Most Muslim investors in the UAE know the word riba. Far fewer can confidently explain gharar, yet it is the second pillar that disqualifies a huge share of modern financial products from being halal.

So, what is gharar in Islamic finance? In one line: it is excessive uncertainty, ambiguity, or hidden risk in a financial contract, the kind that stops one party from knowing exactly what they are agreeing to. Where riba is about unjust returns, gharar is about unjust information. When the terms, the asset, or the outcome are so unclear that you cannot make an informed decision, the contract contains gharar, and it is not permissible.

This guide explains gharar in plain language, shows you exactly where it hides in everyday 2026 finance, from CFDs and crypto to insurance and unclear investment contracts, and gives you a simple test to check any product before you commit your capital.

Table of Contents

- 1. The Short Answer: What is Gharar in Islamic Finance?

- 2. Gharar Explained in Simple Terms

- 3. Why is Gharar Prohibited in Islam?

- 4. Minor Gharar vs. Major Gharar (Gharar Yasir vs. Gharar Fahish)

- 5. The Four Elements That Create Gharar

- 6. Real-Life Examples of Gharar in Modern Finance

- 7. Gharar vs. Riba vs. Maysir, How They Differ

- 8. How to Spot Gharar Before You Invest (The 5-Question Test)

- 9. How MAQ Investments Eliminates Gharar

- 10. Frequently Asked Questions (FAQ)

- 11. How to Get Started with MAQ Investments

1. The Short Answer: What is Gharar in Islamic Finance?

Gharar (غرر) is the Arabic term for excessive uncertainty, ambiguity, or deception in a financial contract. In Islamic finance, gharar refers to any transaction where the key details, the asset, the price, the terms, the delivery, or the outcome, are unknown, undefined, or hidden to a degree that one party could be unfairly harmed.

A contract contains prohibited gharar when a reasonable investor cannot answer three basic questions before agreeing:

- What exactly am I buying or investing in?

- How and when will I receive what I am owed?

- What are the real risks to my capital?

If any of these answers is vague, missing, or designed to be unclear, the transaction fails the gharar test. Alongside the prohibition of riba (interest), avoiding gharar is one of the core conditions of any genuine Shariah-compliant investment.

Also Read: What is Shariah-Compliant Investment?

The Core Definition

Gharar is excessive uncertainty in a contract. Where riba corrupts the return (charging for time and money), gharar corrupts the agreement itself (selling what is unknown or undefined). A genuinely halal investment removes both, the return comes from real performance, and every material term is disclosed in full before you commit.

2. Gharar Explained in Simple Terms

The clearest way to understand gharar is through the classic example Islamic scholars have used for centuries: selling the fish still in the sea, or the bird still in the sky.

You cannot sell a fish you have not caught. Nobody knows if it will be caught, how big it will be, or whether it exists at all. The buyer is paying real money for a completely unknown outcome. That is gharar, a sale of pure uncertainty.

Modern finance is full of digital versions of selling fish in the sea. A contract that pays out based on an event nobody can predict, an investment where you never learn what your money actually buys, or a product with terms so complex that even the seller struggles to explain them, these are the 2026 equivalents of that prohibited sale.

Islamic finance does not prohibit all risk. Genuine business risk is not only permitted, it is required, that is how halal profit is earned through real economic activity. What Islam prohibits is avoidable, excessive uncertainty: risk that comes from hidden information, undefined terms, or pure speculation rather than from honest trade.

The Simplest Way to Think About It

A halal contract says: "You are buying this specific asset, at this price, delivered this way, with these risks."

A gharar contract says: "Give me your money now, and we will see what happens."

If you cannot describe what you are buying and what can go wrong, the contract has too much gharar.

3. Why is Gharar Prohibited in Islam?

Gharar is prohibited because Islamic finance is built on fairness, transparency, and informed consent. A contract can only be just if both parties genuinely understand what they are agreeing to. When one side holds critical information the other lacks, or when the outcome is left to pure chance, the transaction becomes exploitative.

Islamic jurisprudence identifies specific harms that gharar causes:

- It enables exploitation: the party with more information can take advantage of the party with less.

- It invites disputes: when terms are undefined, both sides later disagree about what was actually owed.

- It resembles gambling: paying money for an undefined outcome turns investment into a bet, not genuine trade.

- It breaks informed consent: you cannot truly agree to something you were never allowed to understand.

This is why transparency is not a nice-to-have in Islamic finance, it is a legal requirement. A genuine halal investment must disclose what your capital buys, how returns are generated, what the risks are, and who oversees the structure. Anything less introduces gharar.

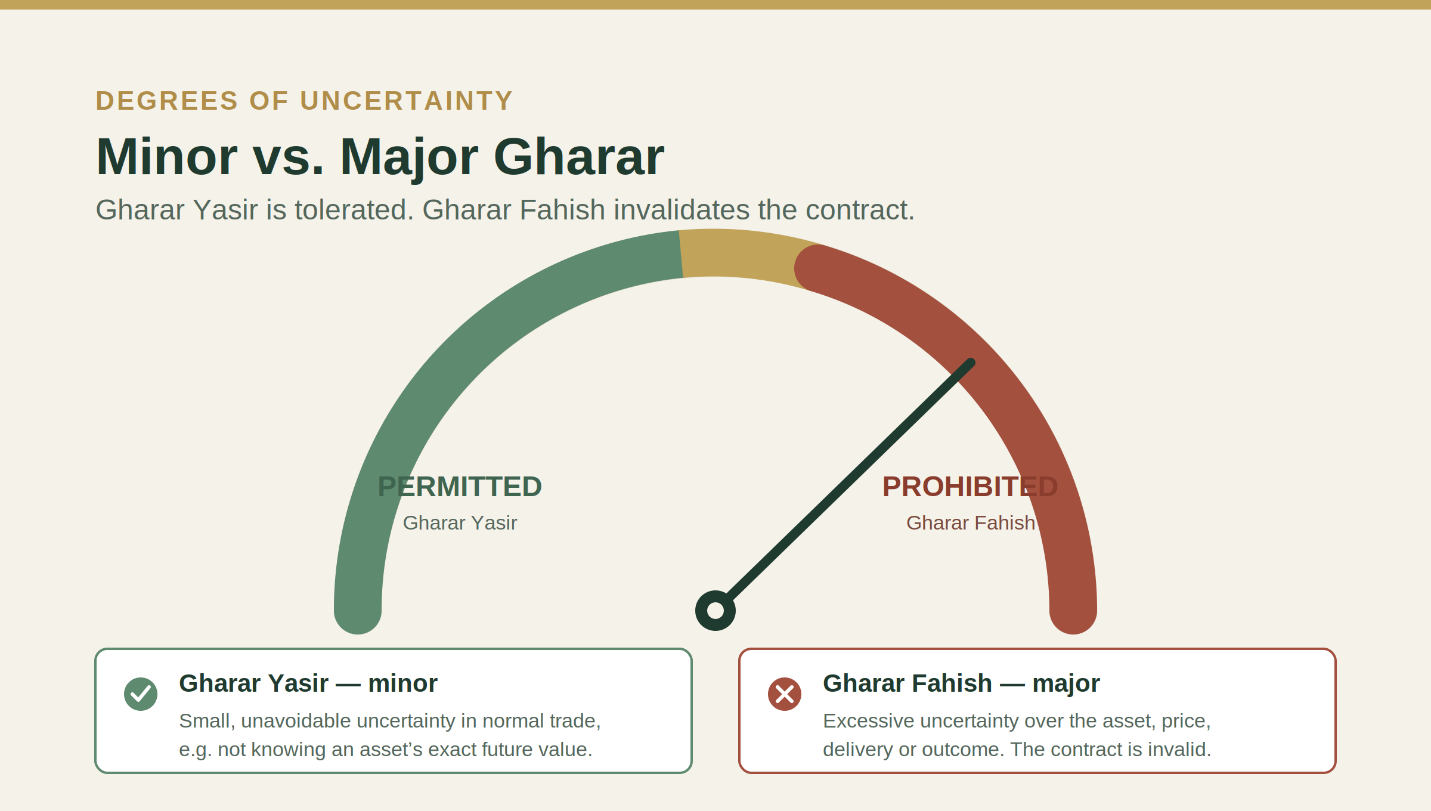

4. Minor Gharar vs. Major Gharar (Gharar Yasir vs. Gharar Fahish)

Not all uncertainty invalidates a contract. Islamic scholars distinguish between two levels of gharar, and only one of them makes a transaction impermissible.

| Type | Meaning | Effect on the Contract |

|---|---|---|

| Gharar Yasir (minor) | Small, unavoidable uncertainty that exists in almost any normal transaction, such as not knowing the exact future market value of an asset you buy today. | Tolerated. Does not invalidate the contract. Everyday trade cannot function without it. |

| Gharar Fahish (major / excessive) | Significant uncertainty about the existence, ownership, price, delivery, or outcome of the subject of the contract. | Prohibited. Invalidates the contract entirely. This is the gharar Islamic finance forbids. |

The practical line is this: a normal degree of business uncertainty is fine. You are allowed to buy gold today not knowing exactly what it will be worth next year. What you cannot do is buy something that may not exist, whose price is undefined, or whose return depends entirely on chance. That is gharar fahish, and it is the standard this guide focuses on.

The Distinction That Matters

Halal investing does not mean zero risk. It means no excessive, avoidable, or hidden uncertainty. You can carry genuine market risk on a clearly defined, real asset. You cannot carry uncertainty about what the asset even is, whether you own it, or how your return is calculated.

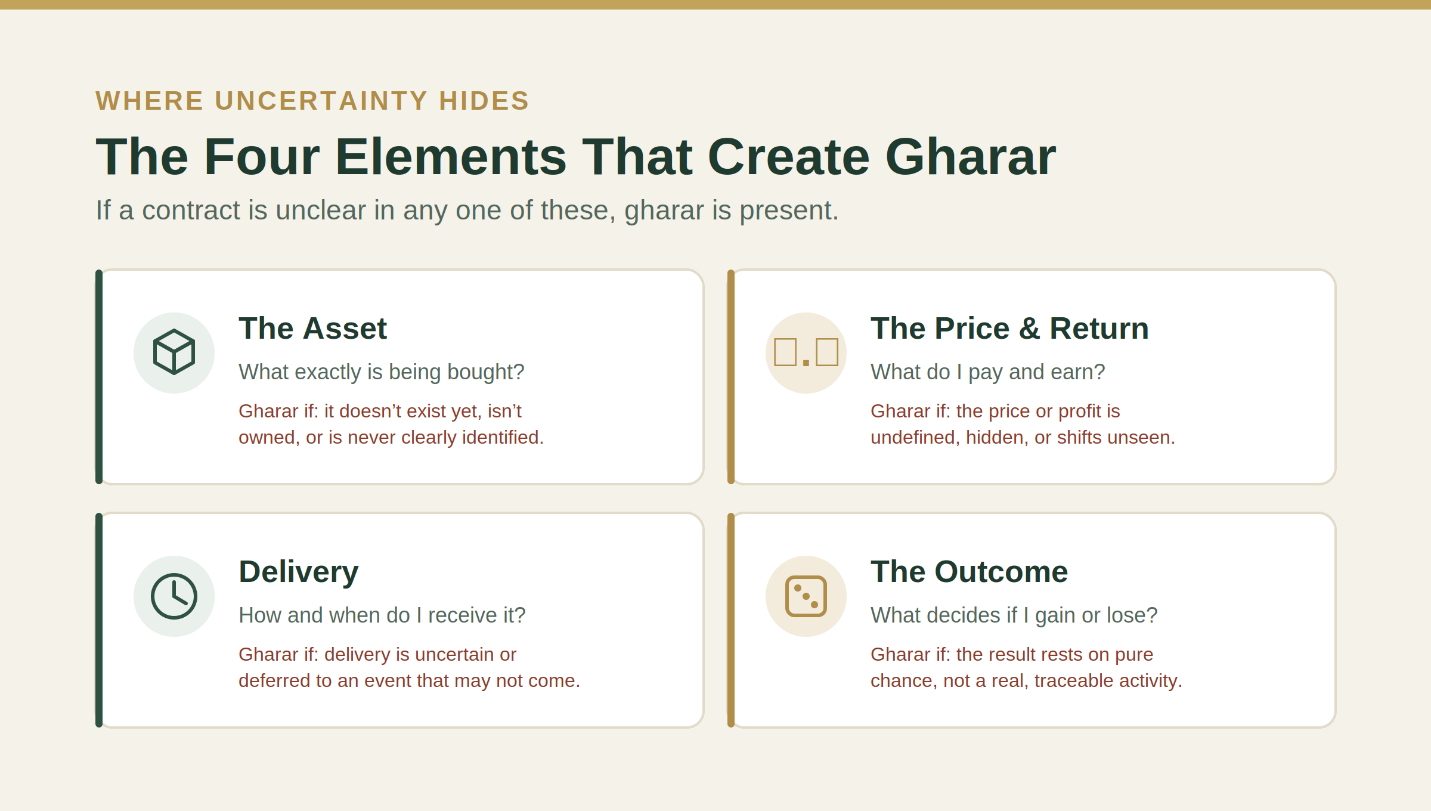

5. The Four Elements That Create Gharar

To make gharar easy to identify, it helps to break it into the four areas where excessive uncertainty usually appears. If a contract is unclear in any one of these, gharar is present.

| Element | The Question It Answers | Gharar Appears When... |

|---|---|---|

| The Asset | What exactly is being bought or invested in? | The asset does not exist yet, is not owned by the seller, or is never clearly identified. |

| The Price | What am I paying, and what is my return? | The price or profit is undefined, hidden, or changes on terms you cannot see. |

| Delivery | How and when do I receive it? | Delivery is uncertain, indefinitely deferred, or dependent on an event that may never happen. |

| The Outcome | What determines whether I gain or lose? | The result depends purely on chance or speculation, not on a real, traceable activity. |

A genuine gold-backed investment answers all four cleanly: the asset is physically allocated gold, the profit-sharing ratio is fixed in writing, distributions follow a defined quarterly cycle, and the return is calculated from real gold operations. No element is left to uncertainty.

Also Read: What Makes an Investment Shariah-Compliant?

6. Real-Life Examples of Gharar in Modern Finance

Gharar is not a historical concept. It appears constantly in 2026 financial products, often inside structures marketed as sophisticated or even "Islamic." Here are the most common real-world examples UAE investors encounter.

Example 1: CFDs and Contracts for Difference

A CFD lets you bet on whether a price will rise or fall without ever owning the underlying asset. You own nothing, deliver nothing, and your entire outcome depends on price movement. There is no real asset, no real trade, only a speculative bet. This is a textbook case of gharar combined with maysir (gambling).

Example 2: Conventional Insurance

In a conventional insurance contract, you pay premiums for a payout that may never come, and if it does, the amount and timing are uncertain. The contract trades a known sum (premiums) for an unknown one (a possible claim). This uncertainty is why scholars developed Takaful (cooperative Islamic insurance) as the gharar-free alternative, where participants contribute to a shared fund rather than buying an uncertain payout.

Example 3: Highly Speculative Cryptocurrency Trading

Buying a clearly owned, spot-settled digital asset is one thing. But leveraged crypto trading, tokens with no defined backing, and products whose value rests entirely on speculation introduce serious gharar, nobody can identify what genuinely underpins the price or how the return is produced.

Example 4: Complex Derivatives and Structured Notes

Options, swaps, and multi-layered structured products are often so complex that the investor cannot understand their true exposure. When a product is engineered so that its real risk is effectively hidden, that complexity itself becomes a form of gharar.

Example 5: "Unallocated" or Paper Gold

An unallocated gold account gives you a claim on a pool of gold rather than specific, identified bars. You are told you own gold, but you cannot point to which gold is yours. That ambiguity over ownership is gharar, and it is exactly why scholars favour physically allocated gold. For a full breakdown, see our guide on whether gold investment is halal.

Example 6: Vague Investment Contracts

Perhaps the most common example of all: an investment that promises attractive returns but never clearly explains what your money is invested in, how the return is generated, or what happens if the venture loses money. If the documentation cannot answer those questions plainly, the contract carries gharar, regardless of how professional it looks.

The Pattern Behind Every Example

Notice what these all share: you cannot clearly identify the asset, the ownership, or how the return is truly produced. That missing clarity, not the product's name or packaging, is what makes it gharar. Remove the uncertainty, define the asset, disclose the terms, and the same capital can often be deployed in a halal way.

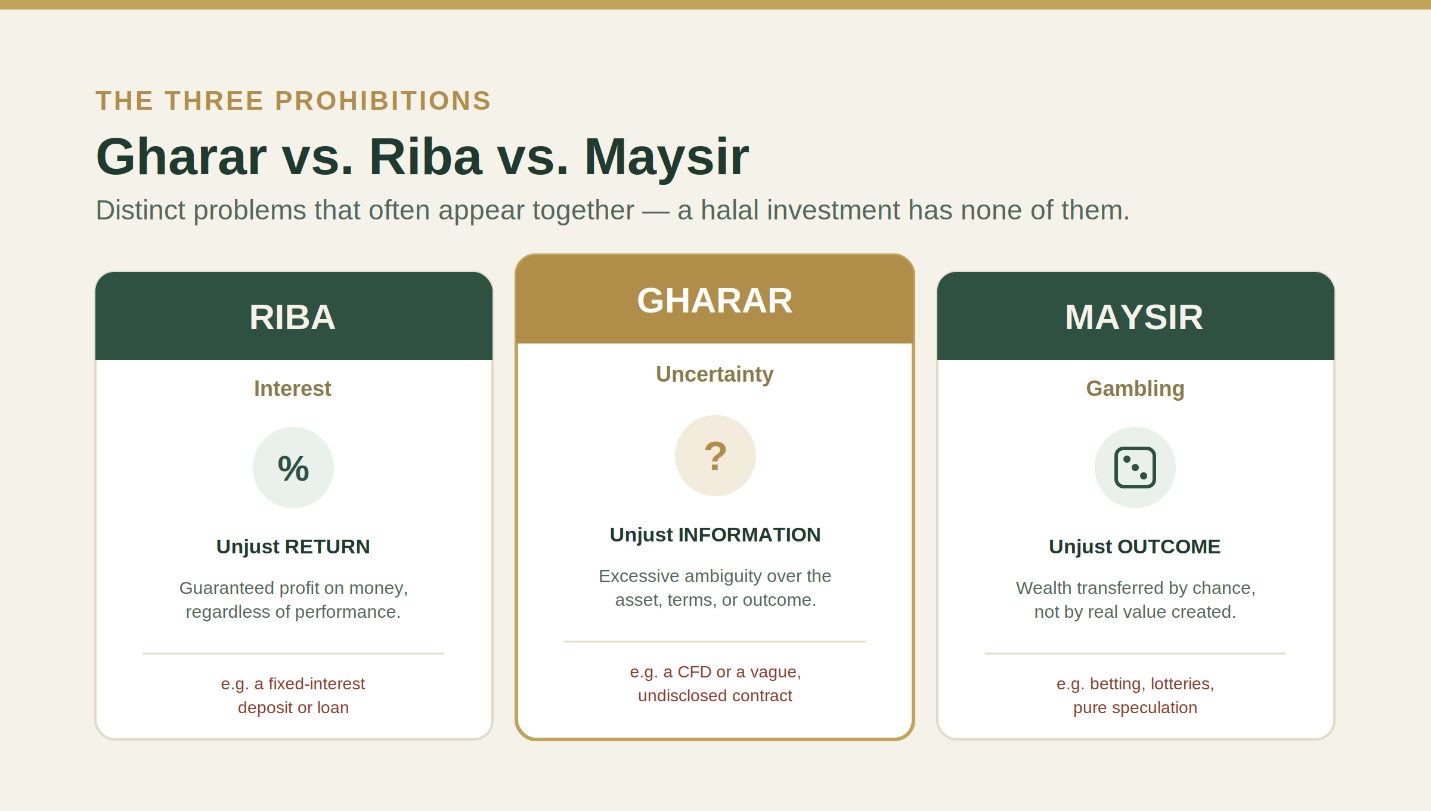

7. Gharar vs. Riba vs. Maysir, How They Differ

Gharar is frequently confused with the other two major prohibitions in Islamic finance. They often appear together in the same product, but they are distinct. Understanding the difference makes each one easier to spot.

| Prohibition | What It Is | The Core Problem | Everyday Example |

|---|---|---|---|

| Riba (interest) | A guaranteed, preset return on money regardless of performance. | Unjust return, money earning money with no real activity. | A fixed-interest bank deposit or loan. |

| Gharar (uncertainty) | Excessive ambiguity about the asset, terms, or outcome. | Unjust information, you cannot know what you agreed to. | A CFD or a vague, undisclosed investment contract. |

| Maysir (gambling) | Gaining at another's expense based purely on chance. | Unjust outcome, wealth transferred by luck, not value. | Betting, lotteries, and pure speculation. |

These three overlap often. A CFD, for instance, contains gharar (no real asset) and maysir (a pure bet) at the same time. A conventional bond can contain both riba (fixed interest) and gharar (opaque terms). A genuinely halal investment is engineered to contain none of the three.

Also Read: What is Mudarabah? The Halal Alternative to Interest

8. How to Spot Gharar Before You Invest (The 5-Question Test)

You do not need to be a scholar to screen for gharar. Before committing capital to any investment in the UAE, ask these five questions. If any answer is vague, evasive, or missing, the product likely contains gharar.

| Test Question | Gharar-Free Answer | Red-Flag Answer |

|---|---|---|

| What exactly is my capital invested in? | A specific, identified, real asset, e.g. physically allocated gold. | "A diversified pool" or no clear answer at all. |

| How is my return generated? | From a defined, real activity you can trace and verify. | "Market movements" or a formula nobody will explain. |

| What happens if the venture makes a loss? | Clearly stated, risk is disclosed and shared honestly. | "Your return is guaranteed regardless" (hidden risk). |

| Can I see the full terms before I commit? | Yes, complete documentation provided upfront. | Terms revealed only after you have signed or paid. |

| Who oversees and reports on the structure? | A named Shariah board plus regular, transparent reporting. | No named oversight and no performance reports. |

The One-Line Gharar Test

Ask yourself: "Could I clearly explain to a family member what I am buying, how I will be paid, and what could go wrong?" If you cannot, because the product will not let you, that missing clarity is gharar. Walk away until it is resolved.

9. How MAQ Investments Eliminates Gharar

MAQ Investments is a Dubai-based, Shariah-compliant, gold-backed investment firm. The entire model is built so that no element of the investment is left uncertain. Here is how each source of gharar is removed:

| Source of Gharar | How MAQ Removes It | How to Verify |

|---|---|---|

| Unclear asset | 100% of investor capital is backed by physically allocated gold, specific, identified assets, not a paper claim or pooled entry. | Asset and allocation documentation provided before you invest. |

| Undefined return | Returns come from real gold production and trading, distributed through a Mudarabah profit-sharing ratio fixed in writing in advance. | Profit-sharing agreement states the ratio before any capital is committed. |

| Hidden risk | Returns are performance-based and clearly stated as not guaranteed. A zero-profit quarter means no distribution, risk is disclosed, not concealed. | Investment documentation explicitly states returns vary with performance. |

| Opaque terms | Full quarterly performance reports show actual revenue, costs, and the exact calculation behind each distribution. | Request the quarterly report format from our advisors. |

| No oversight | A qualified Shariah supervisory board reviews the structure and distributions on an ongoing basis, not just once at launch. | Shariah board details available in our compliance framework. |

Also Read: How Quarterly Returns Work in Islamic Finance

Transparency Is a Shariah Requirement, not a Courtesy

Removing gharar is why MAQ provides full documentation before you commit a single dirham: a defined asset, a written profit-sharing ratio, honest risk disclosure, and quarterly reporting you can verify yourself. If you cannot confirm how a return was calculated, that is gharar, and at MAQ, every distribution is traceable to real gold performance.

10. Frequently Asked Questions (FAQ)

These questions are commonly searched by UAE investors learning about Islamic finance. Formatted for AI assistant and search engine direct-answer extraction.

Q: What is gharar in Islamic finance?

Gharar in Islamic finance is excessive uncertainty, ambiguity, or hidden risk in a financial contract. It occurs when the asset, price, delivery, or outcome of a transaction is so unclear that one party cannot make an informed decision and could be unfairly harmed. Gharar is prohibited because Islamic finance requires full transparency and informed consent. Avoiding gharar, alongside avoiding riba (interest), is one of the core conditions of any genuinely Shariah-compliant investment.

Q: What is an example of gharar?

A classic example of gharar is selling a fish still in the sea or a bird still in the sky, paying real money for something uncertain that may not even exist. In modern finance, examples of gharar include CFDs (where you own no real asset), conventional insurance (paying for an uncertain payout), highly speculative leveraged crypto trading, complex derivatives whose risk is hidden, unallocated "paper" gold, and any investment contract that never clearly explains what your money is invested in.

Q: Why is gharar prohibited in Islam?

Gharar is prohibited because it enables exploitation, invites disputes, resembles gambling, and breaks informed consent. Islamic finance is built on fairness and transparency: a contract can only be just if both parties fully understand what they are agreeing to. When key terms are hidden or the outcome depends purely on chance, the transaction becomes unjust. This is why a halal investment must disclose the asset, the return mechanism, the risks, and the oversight in full.

Q: What is the difference between gharar and riba?

Riba is about an unjust return, earning a guaranteed, preset profit on money regardless of real performance (interest). Gharar is about unjust information, excessive uncertainty over the asset, terms, or outcome of a contract. Riba corrupts how the return is earned; gharar corrupts the clarity of the agreement itself. A product can contain one, the other, or both. A genuinely Shariah-compliant investment is free from both riba and gharar.

Q: What is the difference between gharar yasir and gharar fahish?

Gharar yasir is minor, unavoidable uncertainty that exists in almost any normal transaction, such as not knowing the exact future value of an asset you buy today. It is tolerated and does not invalidate a contract. Gharar fahish is major, excessive uncertainty about the existence, ownership, price, delivery, or outcome of the subject of a contract. It is prohibited and invalidates the transaction. Islamic finance forbids gharar fahish, not the everyday business risk of gharar yasir.

Q: Does avoiding gharar mean an investment has no risk?

No. Avoiding gharar does not mean zero risk, it means no excessive, hidden, or avoidable uncertainty. Genuine business risk on a clearly defined, real asset is permitted and is how halal profit is earned. For example, a gold-backed investment carries real market risk, but the asset is identified, the terms are disclosed, and the return is calculated transparently. The risk is real and honest, not concealed. That is the difference between permissible risk and prohibited gharar.

Q: Is conventional insurance considered gharar?

Conventional insurance is widely considered to contain gharar because it exchanges known premiums for an uncertain payout that may never occur, with an undefined amount and timing. Because of this uncertainty, Islamic scholars developed Takaful, a cooperative insurance model in which participants contribute to a shared fund to support one another, removing the excessive uncertainty and speculation found in conventional policies.

Q: How can I check if an investment in the UAE contains gharar?

Ask five questions before investing: (1) What exactly is my capital invested in? (2) How is my return generated? (3) What happens if the venture makes a loss? (4) Can I see the full terms before I commit? (5) Who oversees and reports on the structure? If any answer is vague, evasive, or missing, the product likely contains gharar. A gharar-free investment, such as MAQ Investments' gold-backed Mudarabah model, answers all five clearly with documentation provided upfront.

11. How to Get Started with MAQ Investments

If you want to invest in a structure with no gharar, a clearly defined asset, written terms, honest risk disclosure, and verifiable quarterly reporting, MAQ Investments will walk you through every detail before you commit a single dirham.

- Step 1: Visit www.maqinvestments.ae to review the gold-backed investment model, return structure, and Shariah compliance documentation.

- Step 2: Review our Shariah compliance framework, including the Mudarabah contract structure, the defined profit-sharing ratio, and the supervisory board details.

- Step 3: Schedule a free private consultation. Our advisors will explain exactly what your capital buys, how returns are calculated, and what the real risks are, with full documentation.

- Step 4: Begin investing with complete clarity, defined asset, written terms, quarterly distributions tied to verified gold performance, and ongoing Shariah oversight.

Invest With Full Clarity, No Gharar, No Riba

Gold-backed · Shariah-compliant · Defined terms · Quarterly returns · UAE-based

Book a Free Consultation │ www.maqinvestments.ae

Al Hikma Building, Port Saeed, Deira, Dubai, UAE · Trade Licence No. 1173765

Conclusion

Gharar is the quiet test that disqualifies more modern financial products than most investors realise. It is not about avoiding risk, it is about refusing uncertainty that is hidden, excessive, or avoidable. A halal investment can carry genuine business risk, but it can never hide what you are buying, how you will be paid, or what could go wrong.

Once you understand what gharar in Islamic finance really is, you start to see it everywhere: in the CFD that owns nothing, the contract that explains nothing, the "gold" you cannot point to. And you also start to recognise the alternative, investments built on real, identified assets, with every material term disclosed before you commit.

That is exactly the standard MAQ Investments was built to meet. If you want to invest in gold the way Islamic finance intends, with clarity instead of uncertainty, speak with our team today.