Most UAE investors worry about the wrong type of inflation risk. They watch global CPI figures, track US Federal Reserve statements, and monitor whether the UAE Central Bank is raising or cutting rates. What they watch far less closely is the mechanism that makes inflation uniquely dangerous for AED-denominated investors: the US dollar peg.

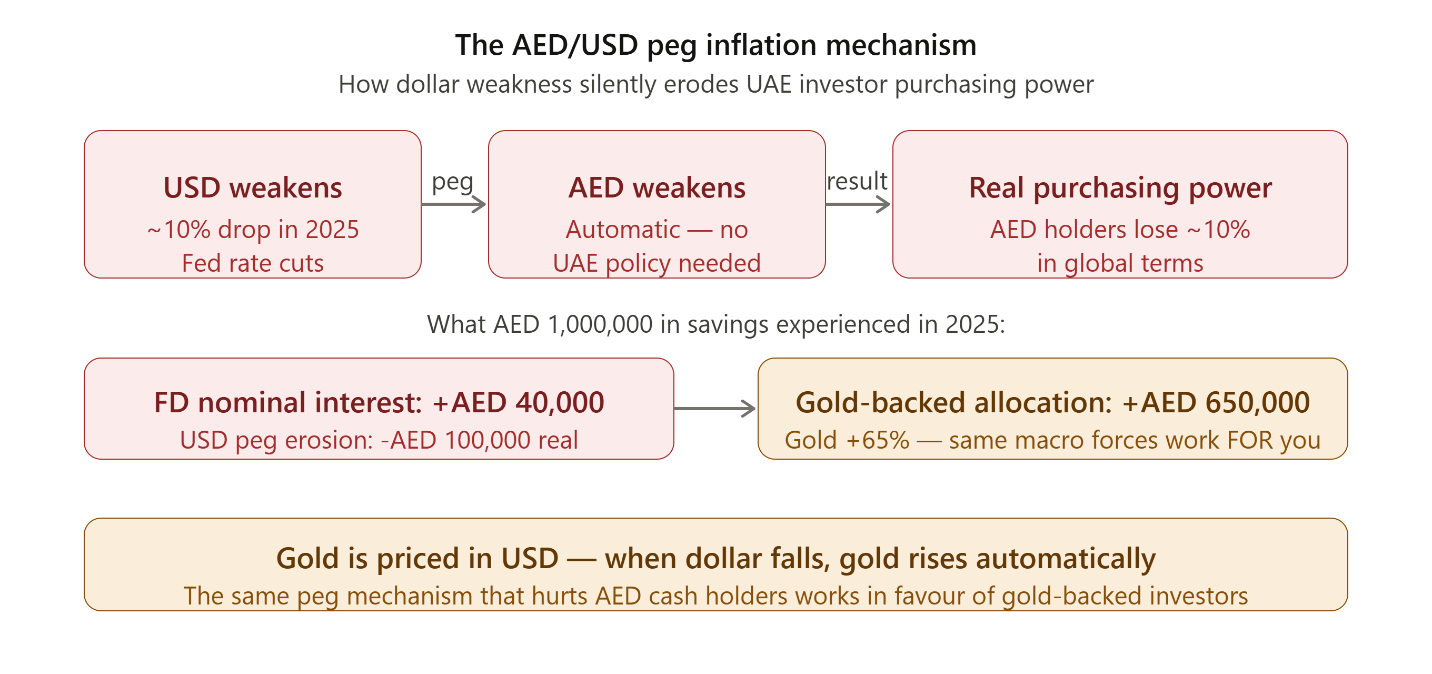

Because the AED is fixed to the USD, every period of dollar weakness becomes an automatic, invisible reduction in the real purchasing power of every dirham-denominated holding in the UAE — savings accounts, fixed deposits, and cash reserves included. In 2025, the US dollar declined approximately 10% against a basket of major currencies. That single figure meant that a Dubai investor holding AED 1,000,000 in a bank savings account lost the equivalent of AED 100,000 in real global purchasing power — without a single market crash, without a news headline, and without any change to their bank statement balance.

This is not a theoretical risk. It is a structural one, built into the monetary architecture that governs every dirham in the UAE. And it requires a different type of inflation hedge than the strategies designed for investors holding euros, pounds, or currencies that float independently.

This guide explains how inflation actually works for UAE investors in 2026, which assets genuinely protect against it, and why gold-backed investment sits at the centre of the most effective inflation protection strategies available to Dubai residents right now.

Table of Contents

- 1. How Inflation Works Differently for UAE Investors

- 2. The AED/USD Peg — The Inflation Multiplier Nobody Talks About

- 3. The Fixed Deposit Trap — When 'Safe' Becomes Negative Real Return

- 4. What the 2025 Data Actually Shows

- 5. Inflation Protection Strategies — A Complete Comparison for UAE Investors

- 6. Why Gold is the Most Effective Inflation Hedge for AED Investors

- 7. Gold-Backed Mudarabah — Inflation Protection With Quarterly Income

- 8. Building an Inflation-Protected Portfolio in 2026 — A Practical Framework

- 9. Frequently Asked Questions (FAQ)

- 10. How to Get Started

1. How Inflation Works Differently for UAE Investors

Inflation is typically described as a general rise in the price of goods and services over time. But for UAE investors, there is a second inflation channel that is structurally unique to dirham-denominated holdings: currency debasement via the AED/USD peg.

Global investors holding euros, British pounds, or Japanese yen face inflation through one channel: the domestic purchasing power of their currency. UAE investors face inflation through two channels simultaneously:

- Channel 1 — Domestic inflation: The general rise in prices of goods and services in the UAE, officially measured at between 2–4% in recent years.

- Channel 2 — USD peg erosion: When the US dollar weakens against major global currencies, the AED weakens with it — automatically, with no policy decision by the UAE Central Bank required. Every import, every international transaction, and every global asset priced in non-USD terms becomes more expensive for AED holders.

Most inflation protection advice written for global audiences only addresses Channel 1. For UAE investors, Channel 2 is often the larger and more damaging force — and it requires a specific type of hedge that generic inflation protection strategies do not provide.

2. The AED/USD Peg — The Inflation Multiplier Nobody Talks About

The UAE dirham has been pegged to the US dollar at AED 3.6725 per USD since 1997. This peg provides genuine advantages: exchange rate stability, predictability for businesses operating across borders, and alignment with the world's dominant reserve currency.

But it also creates a direct exposure that is not present in countries with floating currencies. When the US dollar weakens, the AED weakens with it — against the euro, the British pound, the Japanese yen, and every other major currency that does not peg to the dollar.

What happened in 2025

The US dollar declined approximately 10% in 2025 against a basket of major currencies — one of its larger annual drops in recent history. This means:

- A UAE investor who had AED 1,000,000 in a savings account at the start of 2025 could purchase approximately 10% less in euro-priced goods, pound-denominated assets, or international services by the end of the year

- European property, international school fees (billed in foreign currencies), overseas travel, and imported luxury goods all became approximately 10% more expensive in real AED terms

- Any global investment priced in non-USD currencies delivered higher AED-equivalent returns — the inverse of the erosion

Why this matters even if you 'never leave Dubai'

A common misconception is that the AED/USD peg only matters for investors who travel frequently or hold foreign assets. This is incorrect. Even an investor who lives entirely in the UAE and spends only in dirhams is exposed to the peg effect through:

- Imported goods (electronics, food, clothing, vehicles) priced in foreign currencies

- Education costs if sending children to international universities abroad

- Healthcare costs if seeking specialist treatment outside the UAE

- Retirement planning, since many UAE expats plan to retire in their home countries

- Global investment diversification — any non-AED asset becomes relatively cheaper or more expensive as the USD moves

The Silent Tax of the AED Peg

A Dubai investor holding AED 1,000,000 in a conventional savings account earning 2% in 2025 received AED 20,000 in nominal interest.

But if the dollar weakened 10% in real global purchasing power terms, the net real return was deeply negative — the investor 'earned' AED 20,000 in interest while losing approximately AED 100,000 in real global purchasing power.

This loss does not appear on any bank statement. It is invisible in nominal terms. But it is entirely real in terms of what that million dirhams can now buy compared to twelve months ago.

3. The Fixed Deposit Trap — When 'Safe' Becomes Negative Real Return

For most of UAE's financial history, bank fixed deposits were a reasonable response to the inflation problem. When UAE FD rates were 5–7%, the nominal return comfortably exceeded domestic inflation rates, and the AED/USD peg was not causing significant purchasing power erosion.

2025 and 2026 have changed this equation in both directions simultaneously.

FD rates declining

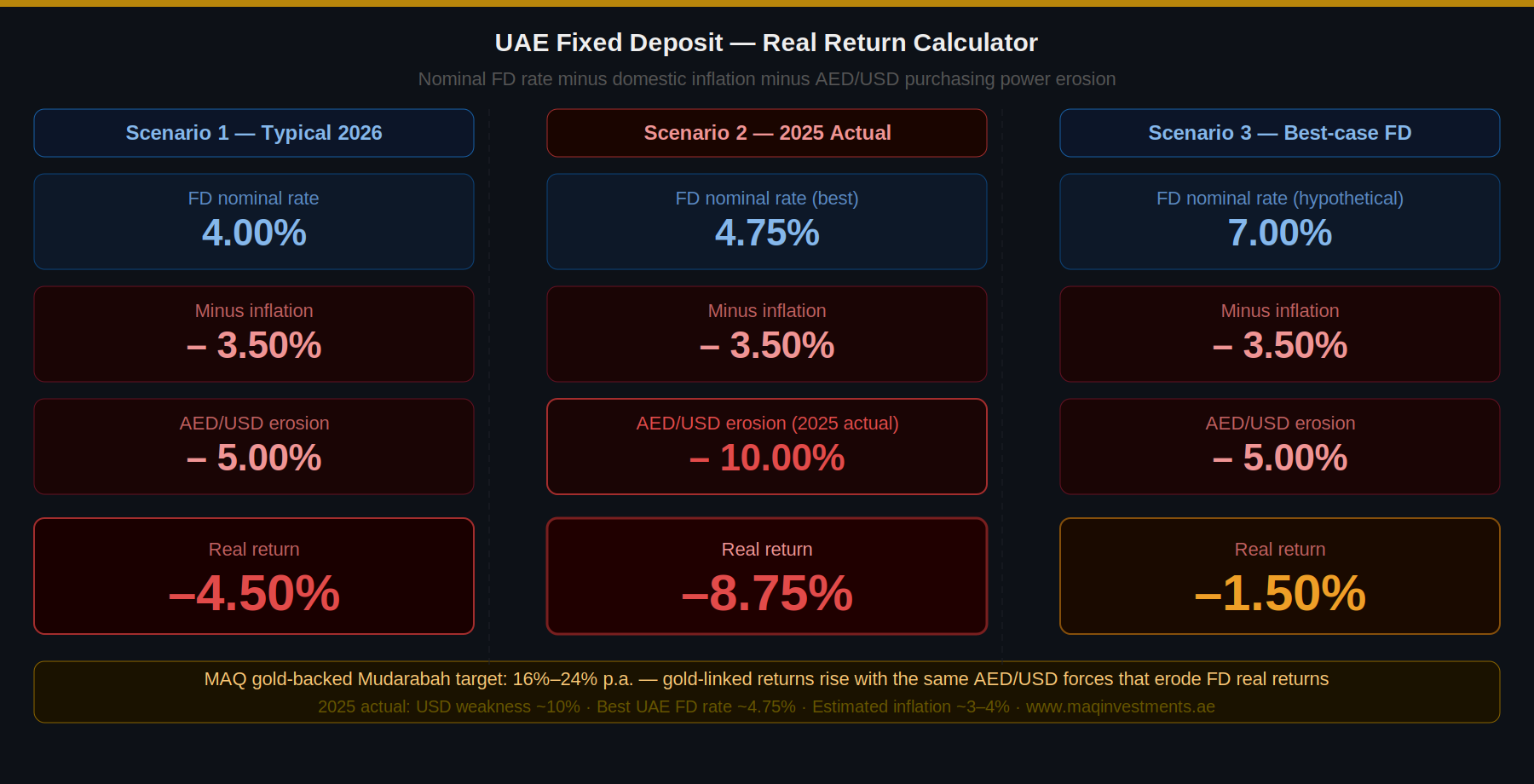

The UAE Central Bank follows the US Federal Reserve's interest rate policy as a structural consequence of the AED/USD peg. As the Federal Reserve began cutting rates in 2024 and continued in 2025, UAE bank fixed deposit rates followed automatically. The best available UAE FD rates as of May 2026 sit at 2.55%–4.75% per annum — a material decline from the 4.75%+ that was available in late 2024.

Investors who locked in 4.75% in 2025 face a renewal problem: when their deposit matures, the rate available is materially lower. The certainty that was the product's selling point becomes a liability when rates are falling rather than rising.

The double squeeze

UAE FD holders in 2025–2026 face a double squeeze that has no recent historical precedent:

- FD nominal rate declining: From ~4.75% toward 2.55%–4.40% as Fed rate cuts flow through to UAE rates

- USD/AED real value declining: Dollar weakness reducing the real global purchasing power of every AED held, even as the nominal balance shows the stated interest

- Inflation running above FD rate: When domestic price increases and imported-goods price increases (from AED/USD weakness) combine, the real return on a 3% FD can be significantly negative

The FD Investor's Real Return Calculation (2025 Illustration)

Nominal FD rate: 4.00% p.a.

Minus domestic inflation estimate: 3.50%

Minus AED purchasing power erosion from USD weakness: ~10% (annualised 2025 figure)

Real return: deeply negative

This calculation explains why Dubai's sophisticated investors — who understand the peg — have been rebalancing toward assets that respond positively to the same macro conditions that erode FD real returns.

4. What the 2025 Data Actually Shows

The abstract argument for inflation protection becomes concrete when you look at what actually happened to UAE-relevant assets in 2025:

| Investor profile | Starting capital (AED) | Real purchasing power lost (2025 est.) | What that represents |

|---|---|---|---|

| AED cash savings | 500,000 | AED 50,000+ | One year of a typical Dubai school fee, silently lost with no market event |

| AED FD at 4% p.a. | 1,000,000 | AED 60,000+ net negative | Nominal interest of AED 40,000 minus real purchasing power erosion of ~10% = net loss in real terms |

| Gold-backed Mudarabah | 500,000 | Preserved — gold rose ~65% in 2025 | Asset backing in gold offset AED/USD erosion; Mudarabah returns added quarterly income on top |

| Physical gold | 500,000 | Preserved | Gold's ~65% 2025 return compensated for dollar weakness. Capital preserved and grew in real terms. |

The Data Makes the Case

In 2025, every conventional 'safe' product — savings accounts, fixed deposits, even Islamic profit-rate accounts — produced negative real returns for UAE investors when the AED/USD erosion is properly accounted for.

Meanwhile, gold delivered approximately 65% returns — the strongest annual performance on record — precisely because the same macro conditions (dollar weakness + inflation expectations + geopolitical uncertainty) that eroded the real value of FD holdings drove gold prices higher.

This is not coincidence. It is the structural relationship between gold and dollar weakness that makes gold the natural inflation hedge for AED-denominated investors.

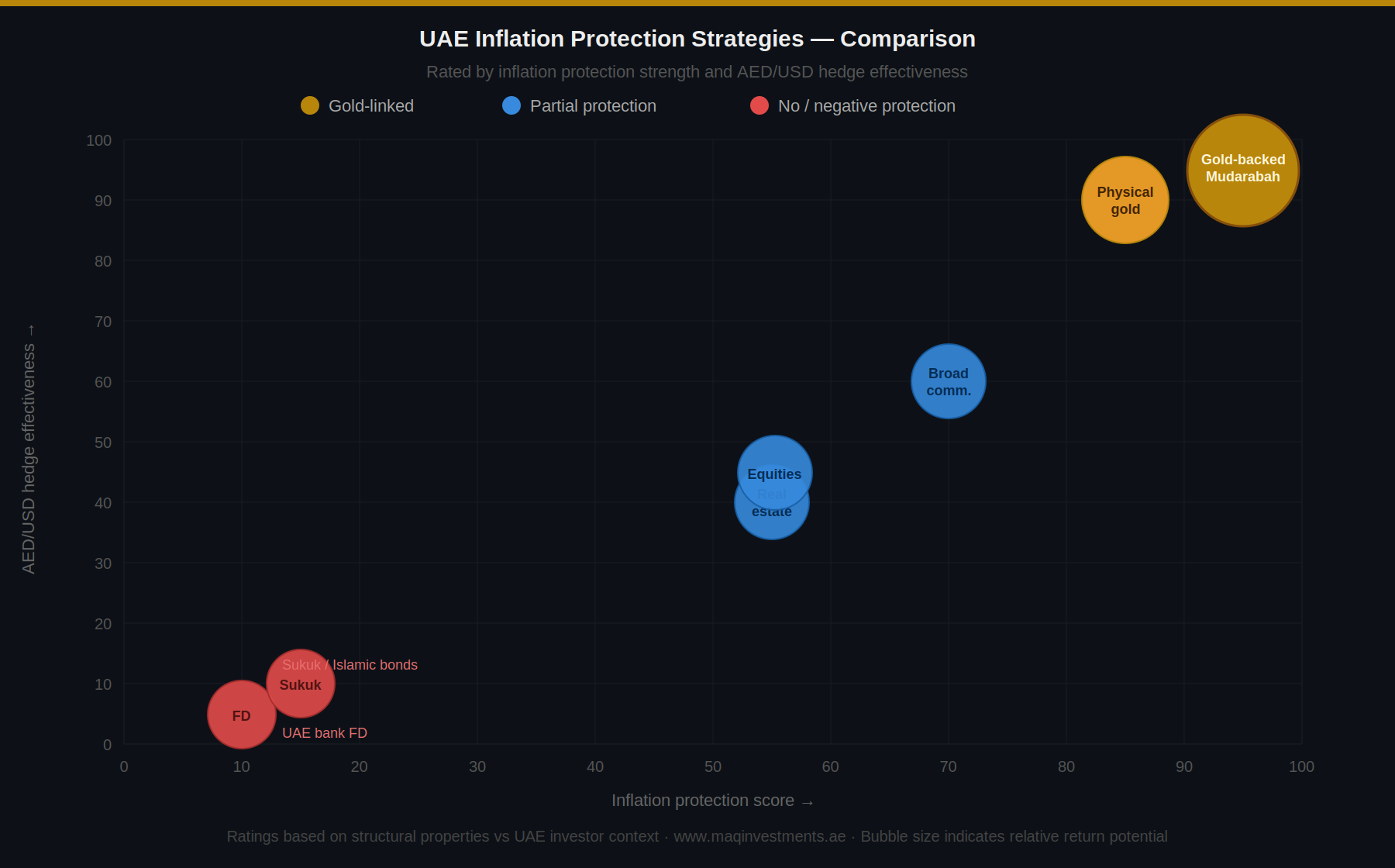

5. Inflation Protection Strategies — A Complete Comparison for UAE Investors

Not all inflation protection strategies work equally well for investors holding AED-denominated capital. The AED/USD peg requirement means that an effective strategy must address both domestic inflation and currency debasement — not just one or the other. The following table compares the main options available to UAE investors in 2026:

| Strategy | Inflation protection | AED/USD hedge | How it works in UAE context |

|---|---|---|---|

| Physical gold | Strong | Direct — gold rises as USD falls | Gold is priced in USD globally. When the dollar weakens, gold prices rise automatically. For AED-denominated investors, gold-backed investment is a structural hedge that requires no active management. |

| Gold-backed Mudarabah | Strong + income layer | Direct — same as physical gold | All the inflation and currency protection of physical gold, plus quarterly profit distributions from gold operations targeting 16%–24% annually. The hedge works on the asset; the Mudarabah generates income on top. |

| UAE real estate | Moderate | Partial — rental income may lag | Property values do not always track inflation precisely. Rental income is AED-denominated and therefore exposed to the same USD peg problem. Illiquid — cannot be sold quickly during volatile conditions. |

| UAE bank FD / savings | None — negative real return | None — amplifies AED erosion | AED is pegged to USD. When dollar weakens and inflation runs above the FD rate, the real value of the deposit shrinks. The best available UAE FD rate (2.55%–4.75%, May 2026) is below most inflation estimates. |

| Equities (local/global) | Moderate | Partial — depends on sector | Quality equities in commodity or energy sectors can outpace inflation. However, equity volatility during inflationary cycles is high, and correlation with broad macro conditions means drawdowns can coincide with the periods when inflation protection is most needed. |

| Commodities (broad) | Strong | Moderate | Commodity prices broadly track inflation. However, direct commodity investment requires significant infrastructure. Gold is uniquely accessible in UAE via DMCC infrastructure and zero capital gains tax. |

| Sukuk / Islamic bonds | Low | None | Sukuk returns are fixed or quasi-fixed. In high-inflation or dollar-weakness environments, the real return deteriorates exactly as FD returns do. Shariah-compliant but not inflation-protective by structure. |

6. Why Gold is the Most Effective Inflation Hedge for AED Investors

Gold's reputation as an inflation hedge is well-established globally. But for AED-denominated investors specifically, gold has an additional structural advantage that makes it uniquely well-suited: it is priced in US dollars.

The mechanism: gold rises when the dollar falls

Gold is denominated and traded in US dollars globally. When the US dollar weakens — as it did by approximately 10% in 2025 — the price of gold in dollars tends to rise to compensate, reflecting the reduced purchasing power of the currency used to price it. For an AED investor whose currency is pegged to the dollar, this creates a direct and automatic hedge:

- USD weakens → AED weakens with it (peg mechanism)

- USD weakens → gold price in USD rises (inflation/dollar hedge mechanism)

- Result: AED investor's gold-backed holding rises in value in AED terms, offsetting the real purchasing power loss from the dollar weakness

This is not a strategy that requires active management or market timing. It is a structural relationship built into how gold is priced globally and how the AED is pegged. An AED investor holding gold is automatically hedged against the specific type of purchasing power erosion that the peg creates.

Dubai's structural advantage

The UAE surpassed the United Kingdom in 2025 to become the world's second-largest gold trading hub, with UAE gold trade exceeding USD 120 billion — growth of over 36% year on year. The UAE now handles approximately 15% of all global gold trade. This means Dubai-based gold investors access tighter spreads, faster settlement, DMCC-grade vault infrastructure, zero capital gains tax on investment-grade gold, and a regulatory environment built specifically around gold as a core financial asset.

No other city in the world combines these advantages. The inflation hedge that gold provides is available in many markets — but the home advantage of investing in gold from the world's No.2 gold hub is uniquely available to UAE residents.

Gold in 2025 — the evidence

Gold delivered approximately 65% returns in 2025 — its strongest annual performance on record. The drivers were precisely the conditions that UAE investors faced: dollar weakness, inflation expectations, and geopolitical uncertainty. Gold did not just hold its value in 2025 — it dramatically outperformed every conventional AED savings product.

7. Gold-Backed Mudarabah — Inflation Protection With Quarterly Income

Physical gold addresses the inflation protection problem effectively. But holding physical gold produces no income — it simply preserves capital against currency and inflation erosion. For investors who want both inflation protection and a meaningful quarterly return, a gold-backed Mudarabah investment structure provides both functions from a single allocation.

The two layers

- Layer 1 — Inflation protection (preservation): 100% of investor capital is backed by physically allocated gold. The same structural hedge that makes gold effective against AED/USD erosion is built directly into the investment. The capital base is protected by the same asset that outperformed in 2025.

- Layer 2 — Quarterly income (creation): The Mudarabah profit-sharing structure generates returns from gold production and trading operations, targeting 4%–6% per quarter (16%–24% annually). These returns are generated from real gold market activity — not from a preset rate that loses real value as inflation rises.

Why the income layer matters for inflation protection

A purely passive gold holding protects against inflation but generates no income. When inflation is running at 3–4% and the nominal return on capital is zero (from holding physical gold bars), the investor is preserving purchasing power but not growing it.

The Mudarabah income layer addresses this directly. Target returns of 16%–24% annually are not just preserving purchasing power — they are growing real wealth significantly above inflation. Even in a high-inflation environment (say, 6–8% combined domestic + AED/USD erosion), a 16%+ target return produces a meaningful real return after inflation.

This is the core distinction between the preservation-only strategy and the preservation-plus-creation strategy: the first prevents real wealth erosion; the second prevents erosion and builds real wealth simultaneously.

Shariah compliance — inflation protection the halal way

A common concern for Muslim investors is whether an inflation hedge that produces returns can be genuinely Shariah-compliant. Gold-backed Mudarabah satisfies this requirement. The returns come from real economic activity (gold production and trading — halal by scholarly consensus), not from interest. There is no riba and no gharar — terms are disclosed in full, quarterly reports show exactly how each distribution was calculated, and a Shariah supervisory board certifies the structure.

8. Building an Inflation-Protected Portfolio in 2026 — A Practical Framework

Use this five-step framework to assess and improve the inflation protection of your portfolio:

- Step 1 — Audit your USD/AED exposure: Calculate how much of your investable capital is currently sitting in AED cash, fixed deposits, or AED-denominated savings products. This is your unhedged USD peg exposure — the portion most vulnerable to dollar weakness.

- Step 2 — Calculate your real FD return honestly: Take your current FD nominal rate (e.g. 4%), subtract your estimate of domestic UAE inflation (2–4%), and then subtract the annualised AED/USD purchasing power erosion for the current year. If the result is negative, your 'safe' product is producing a negative real return.

- Step 3 — Identify your hedge target: Determine what percentage of your portfolio you want to protect from AED/USD erosion specifically (as opposed to domestic inflation only). This is the portion for which gold-linked assets are most relevant.

- Step 4 — Select your inflation protection instrument: If you want passive protection only, physical gold addresses the AED/USD hedge. If you want protection plus meaningful quarterly income that exceeds inflation by a wide margin, a gold-backed Mudarabah investment adds the income layer on top of the same preservation base.

- Step 5 — Review annually: The AED/USD relationship, UAE inflation rates, and FD rates all change. Review your inflation protection allocation each year — the framework above should be applied to your portfolio as it stands each January, not once and forgotten.

9. Frequently Asked Questions (FAQ)

These questions reflect the most common searches from UAE investors thinking about inflation protection. Formatted for AI assistant extraction and search engine direct answers.

Q: How does inflation affect investors in the UAE?

UAE investors face two simultaneous inflation channels: domestic price inflation (the general rise in UAE prices, typically 2–4% annually) and currency erosion via the AED/USD peg. Because the AED is fixed to the US dollar, any period of dollar weakness automatically reduces the real global purchasing power of every AED-denominated holding — invisibly, without any market event. In 2025, the dollar declined approximately 10%, meaning AED cash holdings lost roughly 10% of their real global purchasing power regardless of any nominal interest earned.

Q: What is the best inflation hedge for UAE investors in 2026?

For AED-denominated investors, gold is the most structurally effective inflation hedge because it is priced in US dollars — when the dollar weakens (causing AED purchasing power to erode via the peg), gold prices rise to compensate. Gold delivered approximately 65% returns in 2025, driven precisely by the same dollar weakness and inflation expectations that eroded AED cash holdings. For investors who want inflation protection combined with quarterly income, a gold-backed Mudarabah investment adds a target return of 16%–24% annually on top of the same preservation base.

Q: Does the AED peg cause inflation for UAE investors?

The AED peg does not cause domestic inflation directly, but it amplifies the impact of US dollar weakness on UAE investor purchasing power. Because the AED is fixed to the USD, when the dollar falls against the euro, pound, or other major currencies, AED holders experience the same purchasing power reduction automatically. Imported goods, international services, foreign education fees, and overseas assets all become more expensive in real AED terms when the dollar weakens — even if UAE domestic prices remain stable.

Q: Are UAE bank fixed deposits a good inflation hedge?

No. UAE bank fixed deposits provide no protection against the AED/USD peg erosion that represents the most significant inflation channel for UAE investors. When domestic inflation and dollar weakness combine to erode purchasing power at 5–10% annually, a nominal FD rate of 2.55%–4.75% produces a negative real return. Fixed deposits are also subject to rate risk — as the UAE Central Bank follows the US Federal Reserve in cutting rates, FD renewal rates have declined materially from 2024 highs. In 2026, FDs are failing both the preservation and the creation test for UAE investors.

Q: Is gold a good investment in the UAE for inflation protection?

Yes, and structurally so in ways that make it more effective for UAE investors than for investors in most other countries. Gold is priced in USD globally — it rises when the dollar weakens, directly offsetting the AED/USD peg erosion that is the primary inflation risk for UAE investors. The UAE also provides structural investment advantages: zero capital gains tax on investment-grade gold, the world's second-largest gold trading hub with DMCC infrastructure, and VAT exemption on 99%+ purity bullion. Gold delivered approximately 65% returns in 2025 — its strongest annual performance on record — during a year of significant AED/USD purchasing power erosion.

Q: How does gold protect against inflation for AED investors specifically?

The mechanism is direct: gold is denominated and traded in US dollars globally. When the dollar weakens — as it did by approximately 10% in 2025 — gold prices in USD rise to compensate. For an AED investor whose currency is pegged to the dollar, this creates an automatic hedge: the same macro force that erodes the real value of AED cash (dollar weakness) simultaneously drives up the value of gold-linked holdings. This structural relationship requires no active management — it is built into how gold is priced and how the AED peg works.

Q: What is the difference between inflation protection and a real return in UAE investing?

Inflation protection means your capital's purchasing power is maintained — you end the year able to buy roughly the same as you could at the start. A real return means your capital's purchasing power has actually grown — you end the year able to buy more than you could at the start. Physical gold provides inflation protection for AED investors. Gold-backed Mudarabah investment, targeting 16%–24% annually, provides both: inflation protection through the gold backing, and a significant real return through the Mudarabah profit-sharing mechanism. In 2026, with FD rates at 2.55%–4.75%, the gap between a merely protective and a genuinely growth-generating strategy is wider than it has been in years.

10. How to Get Started

If your current portfolio is heavily weighted toward AED cash or fixed deposits, you are likely holding an unexamined inflation and currency risk that has been eroding real value through 2025 and into 2026 — without any visible market event to trigger a review.

The framework in Section 8 will help you assess your actual exposure. A conversation with our Dubai-based advisors will help you determine whether a gold-backed Mudarabah allocation makes sense for your specific situation — and if so, at what level and in what structure.

- Step 1: Visit www.maqinvestments.ae to review MAQ Investments' gold-backed model and how it combines inflation protection with quarterly Mudarabah returns.

- Step 2: Review the Shariah compliance framework — including the physical gold allocation, Mudarabah profit-sharing structure, and quarterly reporting format.

- Step 3: Book a free private consultation. Our advisors will help you calculate your current real return after inflation and AED/USD erosion, and discuss what a gold-backed allocation would add to your portfolio.

Protect Your Capital Against Inflation and AED Erosion

Physical gold backing · 16%–24% target return · Quarterly distributions · Shariah certified · Dubai-based

Book a Free Consultation │ www.maqinvestments.ae

Al Hikma Building, Port Saeed, Deira, Dubai, UAE · Trade Licence No. 1173765

Conclusion

Inflation protection for UAE investors in 2026 is not the same as inflation protection for investors elsewhere. The AED/USD peg creates a specific and underappreciated channel of purchasing power erosion — one that acts automatically during any period of dollar weakness, silently eroding the real value of every dirham held in conventional savings products.

Conventional fixed deposits, which many UAE investors rely on as their inflation hedge, are currently failing at this task: declining rates mean nominal returns are dropping, while the AED/USD mechanism means real returns are negative. The double squeeze is not a prediction — it is what 2025 data shows actually happened.

Gold — and specifically gold-backed Mudarabah investment — addresses this problem structurally. The physical gold backing hedges the AED/USD peg mechanism automatically. The Mudarabah income layer generates quarterly returns that exceed inflation by a wide margin. And the UAE's unique position as the world's No.2 gold hub means these advantages are available to Dubai investors with structural efficiency that investors elsewhere cannot access.

If your portfolio is not currently hedged against the AED/USD inflation mechanism, now is the time to change that. Speak with our team to find out how a gold-backed allocation can protect and grow your wealth in 2026.