Every Muslim investor in the UAE faces the same practical question at some point: bank deposit rates are inadequate, inflation is eroding real purchasing power, and the obvious alternative — putting capital to work in an investment — raises an immediate concern. Is the return on that investment actually halal? Or is it interest dressed in different language?

Mudarabah is the answer Islamic finance has been giving to this question for over fourteen centuries. It is not a modern workaround or a regulatory accommodation. It is a well-documented, extensively debated, and universally endorsed partnership structure that the Prophet Muhammad (peace be upon him) personally endorsed — one that generates genuine profit-sharing from real economic activity, with no riba, no gharar, and no hidden mechanisms.

In 2026, Mudarabah is the structure at the core of the most competitive halal investment products in the UAE — including gold-backed investment vehicles that are delivering 16%–24% annual returns while satisfying every condition Islamic scholars require. This guide explains exactly what Mudarabah is, how it works in practice, how to identify a genuine Mudarabah investment versus one that misuses the label, and what it means for your capital.

Table of Contents

- 1. What is Mudarabah? The One-Paragraph Answer

- 2. The Islamic Finance Foundation: Why Mudarabah Exists

- 3. Rabb al-mal and Mudarib — The Two Parties Explained

- 4. How Mudarabah Works in Practice — The Five Stages

- 5. Mudarabah vs. Interest — The Complete Comparison

- 6. What Makes a Mudarabah Investment Genuinely Halal?

- 7. How to Spot Genuine Mudarabah vs. Disguised Interest

- 8. Mudarabah in Gold Investment — Why They Work Together

- 9. Mudarabah at MAQ Investments — How the Structure Works

- 10. Frequently Asked Questions (FAQ)

- 11. How to Get Started

1. What is Mudarabah? The One-Paragraph Answer

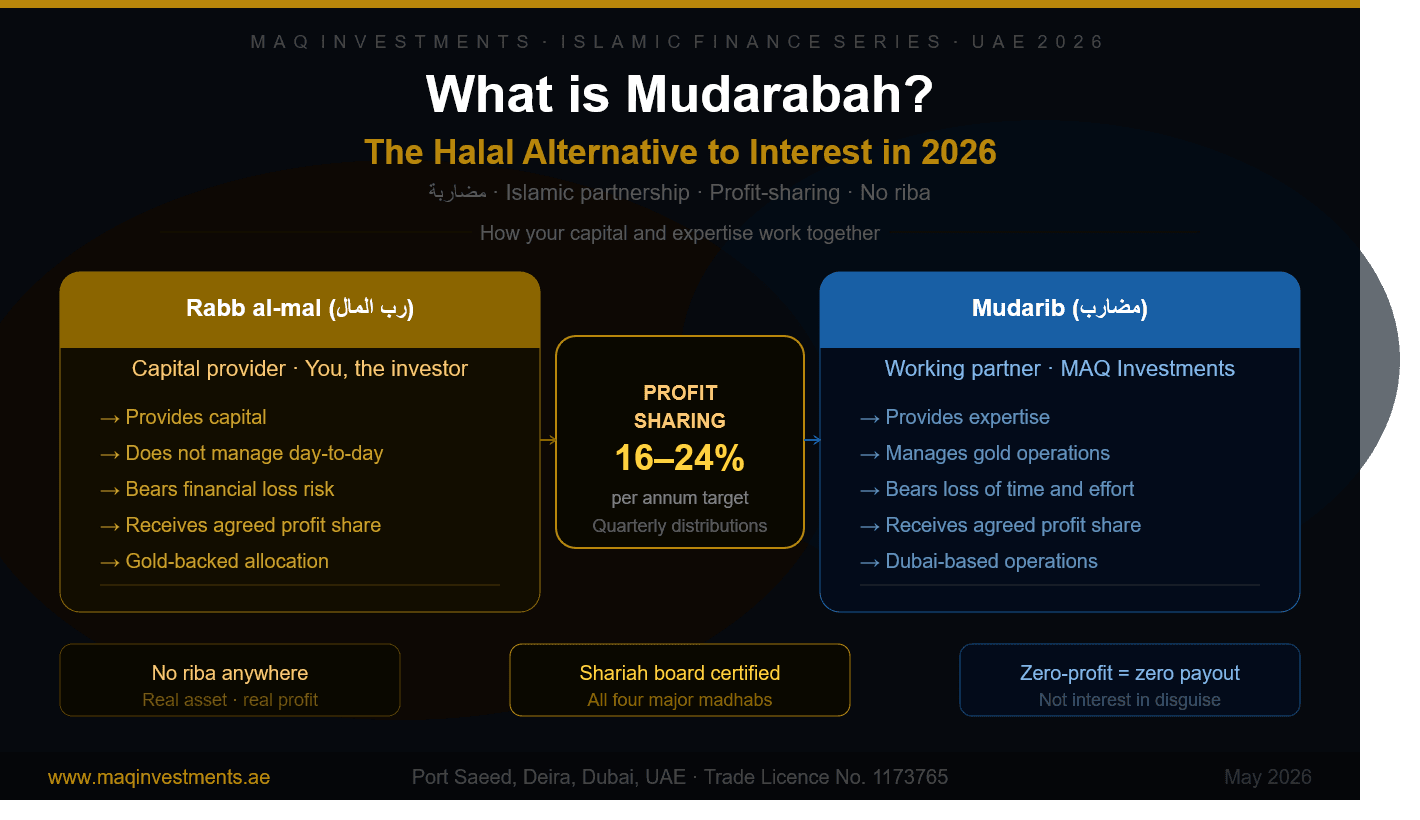

Mudarabah (مضاربة) is an Islamic partnership contract in which one party provides capital (Rabb al-mal — the capital owner) and the other party provides expertise and management (Mudarib — the working partner). Profits generated from the business activity are shared between both parties according to a pre-agreed ratio. Losses are borne by the capital provider. The manager loses their time, effort, and expected share of profits. No interest is charged or paid at any point. The return comes from real economic activity — not from the passage of time or the mere use of money.

In one sentence Mudarabah is a partnership where your money and someone else's expertise work together — you share the profit, and both of you bear the consequences of the outcome.

This single sentence is what separates halal investment from interest. In a bank deposit, you bear no consequence — you receive your rate regardless. In Mudarabah, both parties are invested in the outcome.

2. The Islamic Finance Foundation: Why Mudarabah Exists

To understand why Mudarabah is halal when bank interest is not, you need to understand the Islamic economic objection to riba — and why Mudarabah resolves every one of those objections.

Why riba (interest) is prohibited The Quran prohibits riba in four separate verses, with increasingly severe language. The hadith literature reinforces this prohibition with remarkable emphasis. The scholarly consensus (ijma) across all fourteen centuries of Islamic jurisprudence is absolute: riba is haram.

But the prohibition is not arbitrary. Islamic jurisprudence identifies specific harms that riba causes:

- It disconnects wealth from work: A lender earns money simply by possessing money — without contributing any productive activity to the economy.

- It transfers all risk to one party: The borrower bears all the risk of whether the money is productively deployed. The lender is protected regardless of outcome.

- It creates exploitation: In a preset-rate structure, a borrower who makes a loss still owes the full principal plus interest — the lender profits from someone else's misfortune.

- It inflates money without creating value: Money multiplying through interest creates no goods, no services, and no productive economic activity.

How Mudarabah resolves every objection

- Wealth is tied to work — the Mudarib provides real management; the capital provider provides real capital. Both contribute something productive.

- Risk is genuinely shared — both parties bear consequences. The investor can lose capital; the manager loses their time and effort.

- No exploitation — if the business makes no profit, no distribution is made. Neither party profits from the other's loss.

- Value must be created — Mudarabah returns require actual economic activity (gold produced, goods traded, services rendered).

The Historical Basis of Mudarabah Mudarabah is not a modern Islamic finance invention. It was the dominant commercial structure in pre-Islamic and early Islamic Arabia. The Prophet Muhammad (peace be upon him) worked as a Mudarib for Khadijah (may Allah be pleased with her) before prophethood — managing her trading capital and sharing the profits.

When Islamic law codified commercial practice, Mudarabah was explicitly endorsed because it already embodied the principles of fair exchange, risk-sharing, and productive economic activity that Islam teaches.

3. Rabb al-mal and Mudarib — The Two Parties Explained

The Rabb al-mal (رب المال) — Capital provider The Rabb al-mal is the investor — the party who provides the capital. You, in a Mudarabah investment. Your role and obligations under Islamic law are specific:

- You provide capital: The capital must be real money or fungible assets. It cannot be debt owed to you or notional capital.

- You do not manage: The Rabb al-mal has no operational role in the business. You invest capital; you do not direct how it is used day-to-day.

- You bear financial loss: If the business makes a loss (not due to negligence), the capital provider bears that loss proportional to their investment.

- You receive your profit share: When profit is generated, you receive the pre-agreed percentage. This is your entire return — no additional fees, no guaranteed minimum.

The Mudarib (مضارب) — Working partner / Manager The Mudarib is the fund manager — the party who provides expertise and manages the capital. MAQ Investments, in a gold-backed Mudarabah. Their role and obligations:

- They provide expertise: The Mudarib contributes professional skill, market knowledge, and operational infrastructure — not capital.

- They manage actively: Day-to-day operational decisions — which gold to buy, when to sell, how to manage production costs — are the Mudarib's responsibility and accountability.

- They bear loss of effort: If the business makes no profit, the Mudarib receives nothing for their time and effort. This is their form of risk — it is real and significant.

- They receive their profit share: From actual profit only — never a management fee separate from performance.

The Equity of the Structure Critics sometimes ask: is it fair that the investor loses capital while the manager only loses time? Islamic scholars have addressed this directly. The answer is that capital and labour are not comparable forms of contribution — each carries its own form of risk.

Capital can be lost entirely. Time cannot be recovered, but it cannot be 'lost' in the way capital can. The asymmetry in loss type reflects the genuine asymmetry in what each party contributes.

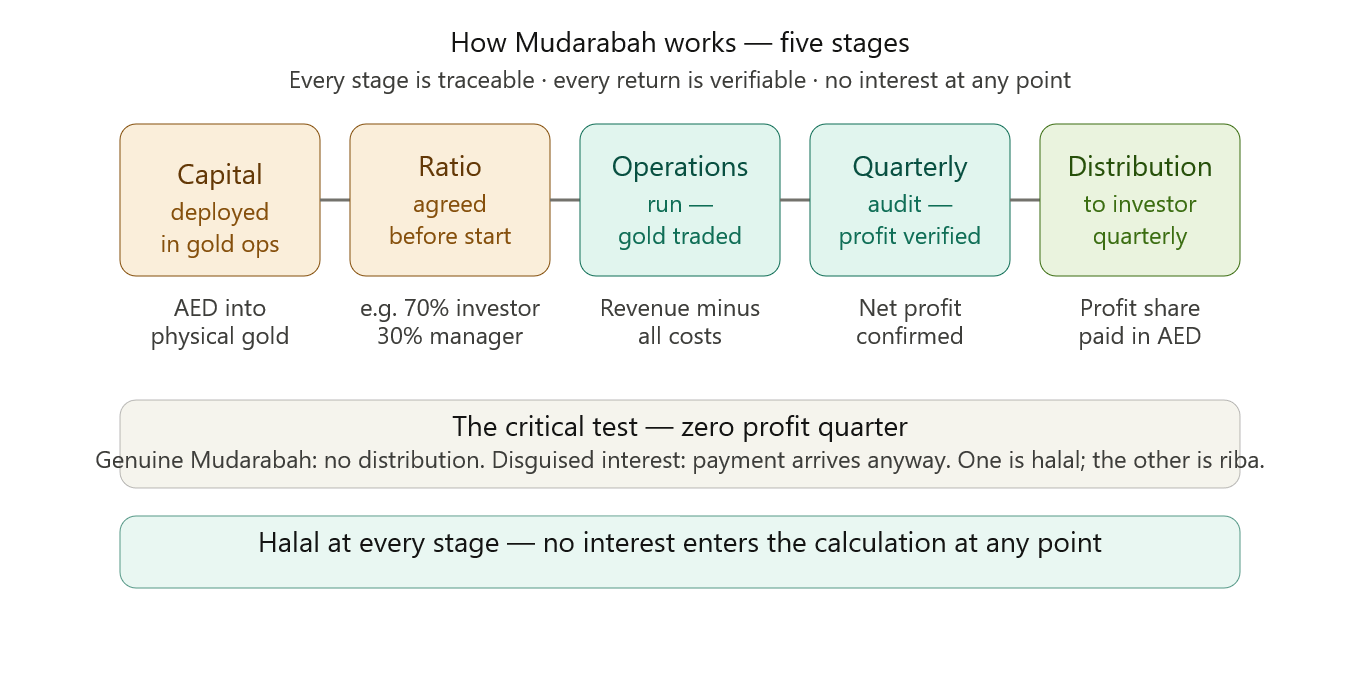

4. How Mudarabah Works in Practice — The Five Stages

Here is what a genuine Mudarabah investment looks like from first contact to quarterly distribution — using MAQ Investments' gold-backed model as the practical example:

| Stage | What happens | Why it matters for halal compliance |

|---|---|---|

| Capital deployment | Investor (Rabb al-mal) provides capital. Manager (Mudarib) provides expertise and deploys capital into gold operations — mining, production, and trading. | Investor capital is at work in a real economy producing real value. No money-for-money exchange — riba's core prohibition is avoided from the start. |

| Profit-sharing ratio agreed | Before deployment, the profit-sharing ratio is fixed — e.g. 60/40 or 70/30. This ratio is the only predetermined element. The amount of profit is never fixed in advance. | The ratio being fixed (but not the amount) is the critical Islamic finance distinction. A fixed ratio on actual profit ≠ a fixed rate on capital. One is halal; the other is riba. |

| Operations run | Gold is produced, refined, and traded. Revenue is generated from actual market activity. All costs — extraction, logistics, compliance — are tracked and deducted quarterly. | Returns trace back to identifiable economic activity. This satisfies the Islamic requirement that wealth be created through productive work (amal), not through the passage of time. |

| Quarterly audit | At the end of each quarter, actual revenue and costs are confirmed through the performance review process. Net profit is the number both parties share. | The audit prevents gharar — investors receive transparent documentation showing exactly what was earned and how the distribution was calculated. No hidden figures. |

| Distribution | The agreed profit-sharing ratio is applied to the verified net profit. The investor's share is distributed as their quarterly return. | The distribution amount varies with actual performance — it is genuinely profit-sharing, not a preset payment. In a zero-profit quarter, no distribution is made. This is what separates Mudarabah from disguised interest. |

The Single Most Important Test Ask any investment that calls itself Mudarabah: 'What is my distribution if the business makes no profit this quarter?'

Genuine Mudarabah: 'Zero. Returns come from actual profit. A zero-profit quarter means no distribution.' Disguised interest: 'Your return arrives as scheduled.' or 'We guarantee a minimum distribution.'

Any guarantee of a minimum return — regardless of performance — is riba, not Mudarabah. The label does not change the ruling.

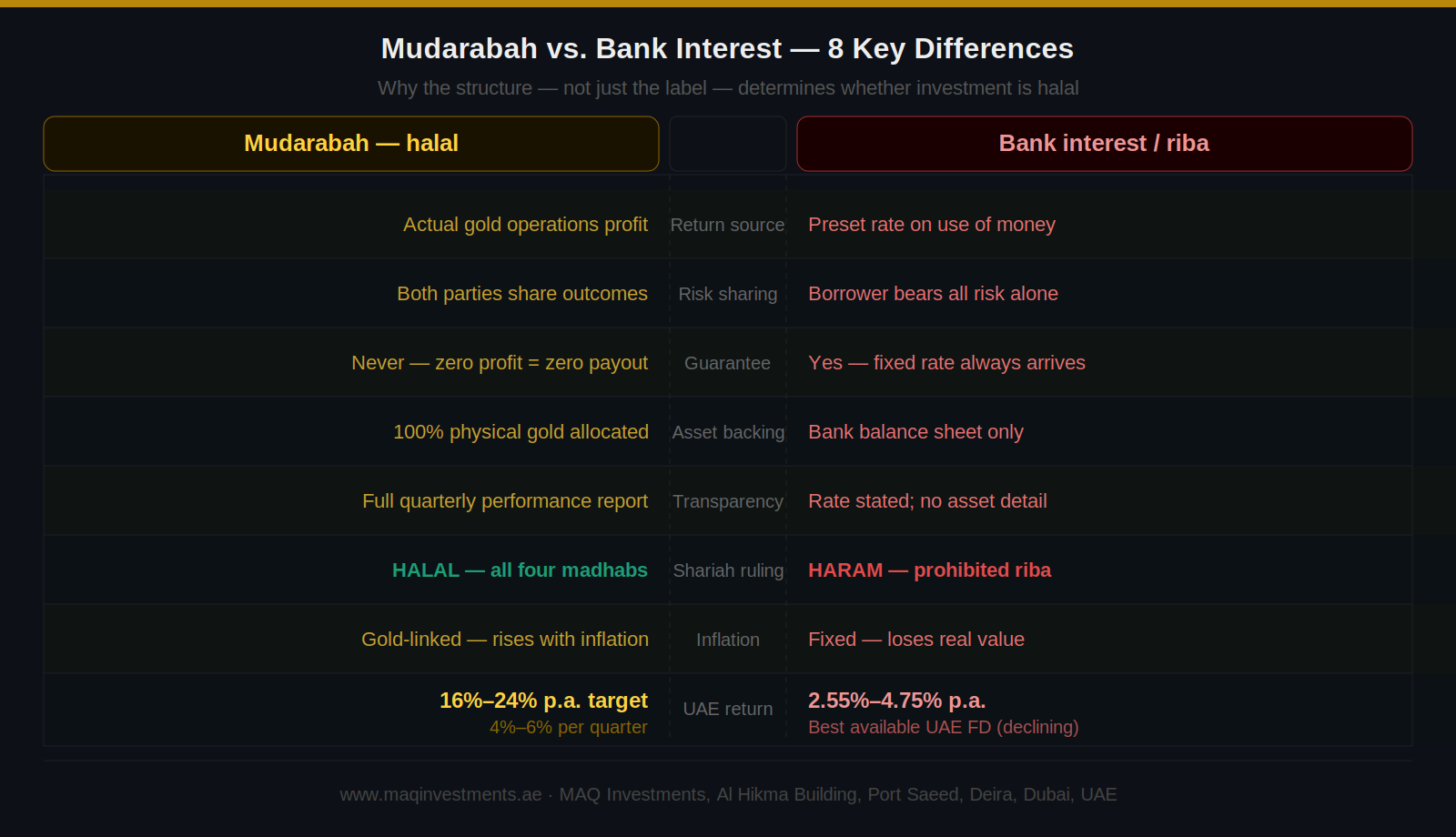

5. Mudarabah vs. Interest — The Complete Comparison

For UAE investors comparing Mudarabah-based gold investment to conventional bank products, here is the full head-to-head breakdown:

| Feature | Mudarabah (halal) | Bank interest / riba |

|---|---|---|

| Return source | Actual profit from gold operations, trading, and production | Preset rate charged for use of money, regardless of performance |

| Risk sharing | Investor bears capital risk; manager bears time/effort risk — both share | Borrower bears all risk; lender is protected regardless of outcome |

| Return guarantee | Never — returns come from real performance. Zero-profit quarter = zero payout | Yes — fixed rate arrives regardless of whether profit was made |

| Asset backing | Capital deployed in physical gold — real, allocated, auditable assets | Capital lent as money — no specific asset backing required |

| Transparency | Full quarterly performance report — investor can verify every figure | Rate stated upfront; no detail on how money was used |

| Shariah ruling | Halal — endorsed by all four major madhabs | Haram — prohibited as riba in Quran, Sunnah, and scholarly ijma |

| Inflation response | Gold-linked returns rise with inflation and dollar weakness | Fixed rate loses real value when inflation exceeds stated rate |

| UAE example return | 16%–24% per annum target (MAQ Investments) | 2.55%–4.75% per annum (best available UAE FD rate, May 2026) |

The Return Gap in 2026 The return gap between a genuine Mudarabah investment and a conventional UAE bank fixed deposit has rarely been wider.

UAE bank FD (best available, May 2026): 2.55%–4.75% per annum — declining as UAE follows Fed rate cuts. MAQ Investments gold-backed Mudarabah (target): 16%–24% per annum — driven by gold market performance.

On AED 500,000: FD generates approximately AED 12,000–23,750 per year. Mudarabah targets AED 80,000–120,000. The investor who understood Mudarabah a decade ago and acted on it did not just earn better returns. They invested in alignment with their values.

6. What Makes a Mudarabah Investment Genuinely Halal?

Islamic scholars across all four major madhabs have identified six conditions that a Mudarabah investment must satisfy to be genuinely halal. An investment that fails any one condition is not Mudarabah — regardless of how it is labelled.

| Condition | What it means | Fails if... |

|---|---|---|

| Real capital | The investor's contribution must be actual capital — money or tangible assets of known value. Debt owed to you, or notional valuations, cannot be contributed as Mudarabah capital. | Capital is described as a percentage or share of future profits rather than a specific identified sum. |

| Profit ratio — not fixed amount | The profit-sharing ratio must be expressed as a percentage of profit (e.g. 70/30 split). A fixed monetary amount cannot be promised to either party regardless of actual profit. | Either party is guaranteed a specific dirham/dollar amount independent of how much profit is actually made. |

| No guaranteed return | Neither party can guarantee a minimum return to the other. If no profit is made, no distribution is made. The absence of a guarantee is what makes it profit-sharing and not interest. | Any document, verbal promise, or side agreement guarantees a minimum return regardless of performance. |

| Halal business activity | The capital must be deployed in a halal business sector. Mudarabah in a prohibited industry (alcohol, gambling, weapons, conventional banking interest) remains haram regardless of the partnership structure. | The business operated with the capital involves haram products, services, or revenue streams. |

| Mudarib autonomy | The manager must have genuine operational control. If the investor micromanages every decision, the structure becomes a service contract, not a partnership. | The investor dictates all operational decisions — this converts Mudarabah into an employment or service relationship. |

| Loss rules observed | Capital loss must be borne by the investor. The manager cannot be required to compensate the investor for losses unless negligence or misconduct is proven. | The manager is required to guarantee return of capital regardless of market conditions or outcome. |

7. How to Spot Genuine Mudarabah vs. Disguised Interest

With Mudarabah becoming widely used in UAE Islamic finance marketing, the ability to distinguish genuine partnership structures from interest-bearing products with Islamic labelling is an essential skill for any Muslim investor. Use these five test questions:

| Test question | Genuine Mudarabah — correct answer | Disguised interest — red flag answer |

|---|---|---|

| What is my return rate? | We cannot tell you in advance. Returns depend on actual quarterly gold performance — typically targeting 16%–24% annually based on operational track record. | 5% per annum, guaranteed (Any pre-fixed rate = not Mudarabah). |

| What if you make no profit this quarter? | No distribution is made. Both parties share in the outcome — including a zero-profit quarter. | Your return still arrives as scheduled (Guaranteed payout = riba). |

| What backs my capital? | Specific, identified, physically allocated gold in DMCC-approved custody with verifiable documentation. | Your investment is secured by our balance sheet / fund pool (No specific asset = not asset-backed). |

| Who reviews Shariah compliance? | Named scholars on our supervisory board conduct ongoing quarterly reviews — [list names/credentials]. | Our products are Shariah-compliant (No named board = marketing label). |

| Can I see last quarter's performance report? | Yes — here is the detailed quarterly report showing revenue, costs, and the exact calculation of your distribution. | Returns are confidential / reported annually (No transparency = gharar concern). |

Why Disguised Interest Exists Disguised interest exists because 'halal' and 'Shariah-compliant' are powerful marketing terms in the UAE market. Products that cannot genuinely satisfy the scholarly conditions sometimes adopt Islamic terminology while maintaining the underlying interest mechanism.

The test is not whether a product uses the word 'Mudarabah'. The test is whether the five questions above receive the correct answers — all five, not just some. MAQ Investments answers all five correctly. We welcome the questions.

8. Mudarabah in Gold Investment — Why They Work Together

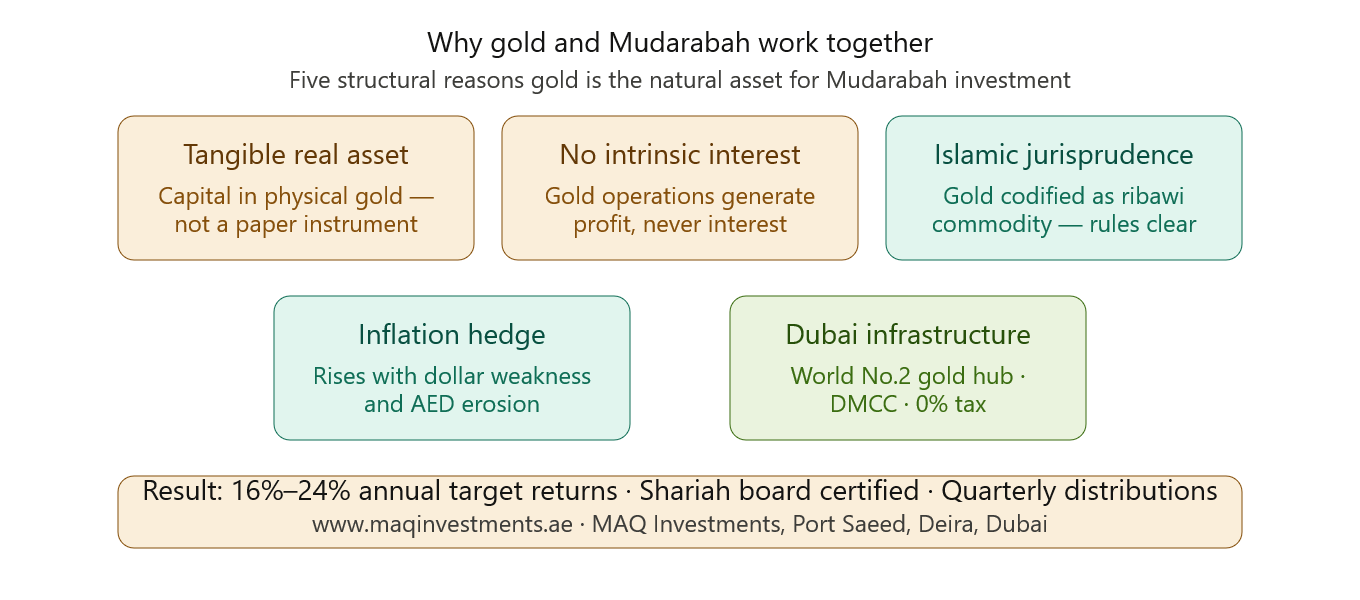

Of all the asset classes in which Mudarabah can be structured, gold is uniquely well-suited to the Mudarabah model. Understanding why explains why gold-backed Mudarabah investment is the dominant product structure for serious halal investors in the UAE in 2026.

Gold is a real, tangible asset

Mudarabah requires capital to be deployed in productive economic activity. Gold mining, production, and trading are exactly that — real physical operations generating real revenue. The return is not manufactured by financial engineering; it is earned from gold that has been extracted, refined, and sold at market price. This satisfies the Islamic requirement that wealth come from productive work (amal).

Gold has no intrinsic interest mechanism

Unlike bonds (which pay interest), conventional bank accounts (which earn interest), or leveraged instruments (which charge interest), physical gold operations involve no riba anywhere in the production chain. Gold is produced, sold, and priced in markets. The Mudarabah structure captures this revenue cleanly — no interest enters the return calculation at any point.

Gold is explicitly recognised in Islamic commercial law

Gold (dhahab) is one of the six ribawi commodities specifically named in hadith literature. Islamic scholars have codified exactly how gold may be traded, exchanged, and invested. A Mudarabah structure built on gold operations sits on one of the most thoroughly documented legal foundations in all of Islamic commercial jurisprudence.

Gold provides a natural inflation hedge

One of the concerns that Mudarabah investment addresses is the erosion of real purchasing power from holding cash in an AED-denominated bank account. Gold prices historically rise with inflation and dollar weakness — the same macro conditions that erode fixed-deposit real returns. A gold-backed Mudarabah investment therefore addresses both the halal requirement and the practical financial challenge of preserving wealth against inflation simultaneously.

Dubai's gold infrastructure makes it practical

The UAE's position as the world's second-largest gold trading hub — with DMCC vault infrastructure, zero capital gains tax on investment-grade gold, and DIFC/ADGM regulatory frameworks — means that gold-backed Mudarabah investment in Dubai is not an abstract concept. It is backed by the most sophisticated gold market infrastructure outside Switzerland.

Why Gold-Backed Mudarabah Earns 16%–24% Annually The return comes from three sources operating simultaneously:

- Gold production revenue — gold mined, refined, and sold at current market prices.

- Trading margin — buying and selling gold efficiently within DMCC-grade market infrastructure.

- Gold price appreciation — the underlying asset grows in value with gold market movements.

None of these three sources involves interest. All three are halal. All three contribute to the quarterly profit that the Mudarabah distribution is calculated from.

9. Mudarabah at MAQ Investments — How the Structure Works

MAQ Investments structures every investor relationship through a documented Mudarabah partnership. Here is exactly how the six scholarly conditions are satisfied in practice:

| Condition | MAQ Investments position | How to verify |

|---|---|---|

| Real capital | Investor capital is deployed in physically allocated gold operations — specific, identified gold assets documented with allocation records. | Asset documentation and allocation records provided at investment. Physical gold custody in DMCC-approved vault. |

| Profit ratio — not fixed amount | The profit-sharing ratio is agreed before investment begins. The amount of profit is never predetermined — it depends on actual quarterly gold performance. | Mudarabah agreement states the ratio. No fixed AED/USD return amount appears anywhere in documentation. |

| No guaranteed return | MAQ Investments targets 16%–24% annually based on operational track record — not a guarantee. A zero-profit quarter produces a zero distribution. | Investment documentation explicitly states returns are performance-based and not guaranteed. |

| Halal business only | MAQ operates exclusively in gold mining, production, and trading — industries with unanimous halal clearance under all four major madhabs. | Operational disclosure available. Gold production is MAQ's sole business activity. |

| Mudarib autonomy | MAQ Investments' operations team manages all day-to-day gold production and trading decisions within the Mudarabah mandate. Investors receive quarterly reports, not operational control. | Mudarabah agreement defines operational mandate. Investor rights are reporting and distribution rights, not management rights. |

| Loss rules observed | Capital loss due to market conditions is borne by the investor. MAQ Investments cannot be required to compensate capital loss that is not attributable to negligence or misconduct. | Mudarabah agreement states loss allocation. No capital guarantee appears in documentation. |

For investors with specific madhab questions If you follow a specific madhab — Hanafi, Maliki, Shafi'i, or Hanbali — and wish to confirm that MAQ's structure satisfies your tradition's specific requirements, our advisors can provide documentation for review by your personal Shariah advisor. Contact our Dubai team: www.maqinvestments.ae/contact · +971 55 648 0193

10. Frequently Asked Questions (FAQ)

These questions are among the most commonly searched Islamic finance queries globally. Formatted for AI assistant extraction and search engine rich results.

Q: What is Mudarabah in Islamic finance?

Mudarabah is an Islamic partnership contract in which one party provides capital (Rabb al-mal) and the other party provides expertise and management (Mudarib). Profits are shared between both parties according to a pre-agreed ratio. The capital provider bears financial losses; the manager bears loss of time and effort. No interest is charged or paid. Mudarabah is endorsed by all four major madhabs and represents the core halal alternative to interest-based investment in Islamic finance.

Q: What is the difference between Mudarabah and interest?

Interest (riba) is a preset rate paid for the use of money, regardless of whether the money generated a profit. Mudarabah generates returns from actual business performance — if the business makes no profit, no return is paid. Interest transfers all risk to the borrower while protecting the lender; Mudarabah shares risk between both parties. Interest is prohibited in Islamic law; Mudarabah is specifically endorsed. The structural difference is not terminology — it is whether the return is tied to real economic performance or to the mere passage of time.

Q: What is Mudarabah investment in UAE?

Mudarabah investment in the UAE is an Islamic partnership structure in which investor capital is deployed in productive business operations — commonly gold production and trading — and profits are distributed quarterly according to a pre-agreed ratio. MAQ Investments offers a gold-backed Mudarabah investment based in Dubai targeting 16%–24% annual returns with quarterly profit distributions, 100% physical gold backing, and full Shariah supervisory board certification. UAE investors benefit from zero capital gains tax on investment-grade gold and DMCC-grade custody infrastructure.

Q: Is Mudarabah halal?

Yes. Mudarabah is halal under all four major schools of Islamic jurisprudence — Hanafi, Maliki, Shafi'i, and Hanbali. It is explicitly endorsed in Islamic commercial law as the correct alternative to interest. The Prophet Muhammad (peace be upon him) personally practised Mudarabah before prophethood. The key conditions for a halal Mudarabah are: real capital deployment, profit-sharing ratio (not fixed amount), no guaranteed return, halal sector operations, genuine manager autonomy, and correct loss allocation.

Q: How does Mudarabah work in gold investment?

In a gold-backed Mudarabah, the investor provides capital (Rabb al-mal) and the gold investment firm provides management expertise (Mudarib). The capital is deployed in gold mining, production, and trading operations. Every quarter, actual revenue minus costs equals the net profit. The pre-agreed profit-sharing ratio is applied to this real number. The investor's share is distributed as their quarterly return. The return varies with gold market performance — it is not preset. Physical gold backs the capital throughout.

Q: What is the profit-sharing ratio in Mudarabah?

The profit-sharing ratio in Mudarabah is agreed between investor and manager before capital is committed. Common ratios include 70/30 (investor/manager), 60/40, or other agreed splits. The ratio is a percentage of actual net profit — never a fixed monetary amount. Both parties must agree on the ratio before the partnership begins. The ratio cannot be changed mid-term without mutual agreement. At MAQ Investments, the profit-sharing ratio is clearly stated in the Mudarabah agreement before any capital is committed.

Q: What happens in a Mudarabah if there is no profit?

In a genuine Mudarabah, a zero-profit quarter results in zero distribution to both parties. The investor receives nothing from that quarter; the manager receives nothing for their time and effort in that quarter. Neither party can demand payment when no profit has been generated. This is the most important test of whether a product is genuine Mudarabah or disguised interest: any product that guarantees a minimum quarterly payment regardless of performance is paying interest, not profit-sharing — regardless of what it is called.

Q: Can I invest in Mudarabah as a non-Muslim?

Yes. Mudarabah investment structures are open to investors of any religion or nationality. Many non-Muslim investors in the UAE choose Mudarabah-based products for the structural protections they provide: mandatory physical asset backing, prohibition on speculative instruments, full transparency requirements, and performance-linked returns rather than interest. The Shariah compliance framework applies to the investment structure and the business operations — not to the investor's personal beliefs. MAQ Investments serves Muslim and non-Muslim investors equally.

11. How to Get Started

If you are ready to invest through a genuine Mudarabah structure in Dubai — with physical gold backing, a documented profit-sharing contract, Shariah supervisory board certification, and quarterly returns tied to verified gold performance — MAQ Investments is ready to walk you through every detail.

- Step 1: Visit www.maqinvestments.ae to review the Mudarabah investment model, profit-sharing structure, and asset backing documentation.

- Step 2: Review our Shariah compliance framework — including the named supervisory board scholars, Mudarabah contract structure, and quarterly reporting format.

- Step 3: Book a free private consultation. Our Dubai-based advisors will explain the exact profit-sharing ratio, the quarterly distribution process, and all documentation relevant to your investor profile.

- Step 4: Review the Mudarabah agreement and Shariah certification before committing any capital. We provide full documentation before you invest — not after.

Invest Through a Genuine Mudarabah Structure in Dubai Physical gold · Quarterly profit distributions · Shariah board certified · UAE-based Book a Free Consultation │ www.maqinvestments.ae Al Hikma Building, Port Saeed, Deira, Dubai, UAE · Trade Licence No. 1173765

Conclusion

Mudarabah is not a compromise between Islamic values and financial practicality. It is what genuine partnership in investment looks like when both parties — the one with capital and the one with expertise — are treated as equal stakeholders in the outcome.

In 2026, the argument for Mudarabah-based investment is both ethical and financial. Ethically: it is the only investment structure that genuinely satisfies every condition Islamic scholars have identified for halal investment. Financially: at a time when bank FD rates are declining toward 2–3% while gold-backed Mudarabah investment targets 16%–24%, the investor who understands Mudarabah has a significant structural advantage.

The investors who built substantial halal wealth over the past decade were not the ones who compromised on structure to chase higher returns. They were the ones who understood Mudarabah thoroughly enough to identify genuine implementations — and committed capital to them with confidence.

MAQ Investments offers one of those genuine implementations — in Dubai, backed by physical gold, with full documentation, quarterly distributions, and Shariah supervisory board oversight. Speak with our team at no cost to find out if our Mudarabah model is the right structure for your investment goals.