Two very different investors walk into a conversation about gold-backed investment in Dubai. The first is a family office manager at DIFC, overseeing a multi-generational portfolio for a UAE founding family. The second is an expat professional who has spent fifteen years in Dubai, built solid savings, and is done watching inflation quietly erode them while bank deposit rates decline. Both are serious. Both are ready. Both are right for gold-backed investment. But they need different things from their investment structure.

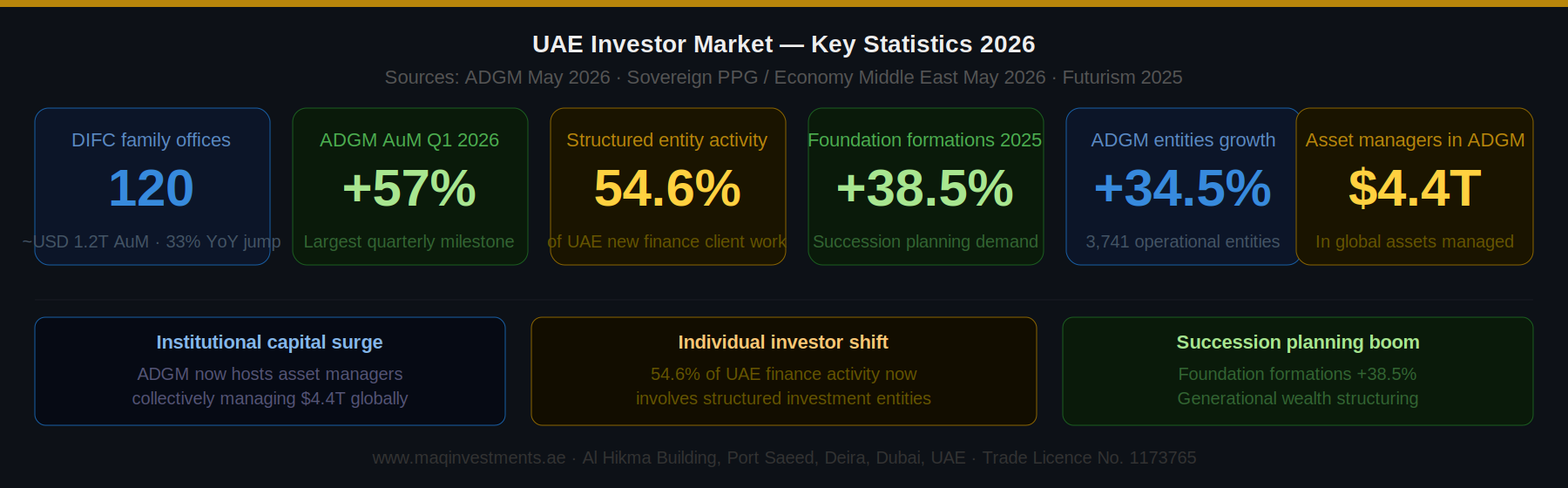

This is not a theoretical distinction. The UAE's investment landscape in 2026 is witnessing a historic bifurcation: institutional money is formalising at unprecedented speed, ADGM recorded a 57% surge in AuM in Q1 2026 alone, and DIFC now hosts 120 family offices managing approximately USD 1.2 trillion, while individual and HNW investors are simultaneously moving away from passive bank savings toward structured, asset-backed vehicles that actually protect and grow their wealth.

MAQ Investments serves both. This article explains the differences between institutional and individual investors in the UAE context, what each type of investor needs from a gold-backed investment structure, and how to determine which approach fits your situation.

Table of Contents

- 1. UAE Investment Market in 2026, The Data

- 2. Who Is an Institutional Investor in the UAE?

- 3. Who Is an Individual / HNW Investor in the UAE?

- 4. Head-to-Head: Institutional vs. Individual, The Full Comparison

- 5. How Each Investor Type Approaches Gold-Backed Investment

- 6. Investment Structures Available in the UAE, A Decision Guide

- 7. The UAE's Wealth Formalisation Trend, What It Means for Both

- 8. How MAQ Investments Serves Both Investor Types

- 9. Which Structure Is Right for You? (Decision Framework)

- 10. Frequently Asked Questions (FAQ)

- 11. How to Get Started with MAQ Investments

1. UAE Investment Market in 2026, The Data

Understanding who is investing in the UAE in 2026 requires data, not generalisation. The following figures, drawn from verified May 2026 sources, frame the landscape within which both institutional and individual investors are operating.

| Metric | Figure | Source / Context |

|---|---|---|

| DIFC family offices (hosting) | 120 family offices, ~USD 1.2 trillion AuM | 33% jump in family wealth entities in one year (Futurism, 2025) |

| ADGM AuM growth Q1 2026 | +57% year-on-year | Largest quarterly milestone in ADGM history (The National, May 2026) |

| ADGM AuM growth 2024 | +245% in AuM | Driven by tax-free structures and full foreign ownership (Futurism) |

| UAE structured entity activity 2026 | 54.6% of new finance activity involves structured entities | Holding companies, SPVs, foundations, Sovereign PPG data (Economy Middle East, May 2026) |

| UAE foundation formations 2025 | +38.5% year-on-year | Growing demand for succession planning and governance (Sovereign PPG, May 2026) |

| Asset managers in ADGM Q1 2026 | Collectively manage USD 4.4 trillion in global assets | Reinforces ADGM's prominence as institutional capital hub (ADGM, May 2026) |

| UAE family office market size | USD 103.5 million in 2025 | Projected USD 148.7 million by 2034, CAGR 4.11% (IMARC Group) |

| Gold investment, UAE tax treatment | 0% capital gains tax on investment-grade gold | Investment-grade bullion VAT-exempt in UAE |

What the Data Tells Us

The UAE investment market in 2026 is not a single audience, it is two simultaneous booms running in parallel. Institutional money is professionalising and formalising at record pace, while individual and HNW investors are restructuring how they hold wealth, moving away from passive savings into structured vehicles. Both movements converge on the same conclusion: asset-backed, physically secured investment, exactly the model MAQ Investments provides, is the structure both types of investors are gravitating toward.

2. Who Is an Institutional Investor in the UAE?

An institutional investor is an organisation that pools large amounts of capital and invests on behalf of its beneficiaries, shareholders, or principals. In the UAE context, institutional investors include:

Sovereign wealth funds Abu Dhabi Investment Authority (ADIA), Mubadala Investment Company, ADQ, and Dubai Investment Corporation are among the world's largest institutional investors. These entities collectively manage hundreds of billions in assets and set the gold standard, quite literally, for how institutional capital is deployed in the UAE.

Family offices DIFC now hosts 120 family offices managing approximately USD 1.2 trillion in assets, a 33% jump in new registrations in a single year. ADGM introduced its Single Family Office licence in 2024, enabling families to manage their own wealth under a streamlined regulatory framework. These are not passive holders; they are professionally managed entities deploying capital across multiple asset classes with formal governance frameworks.

Corporate treasury investors UAE companies, from large conglomerates to mid-sized holding companies, increasingly deploy idle treasury capital into structured investment vehicles rather than letting it sit in current accounts. With UAE Corporate Tax introduced at 9% on profits above AED 375,000, efficient capital deployment has become a boardroom priority.

Pension funds and endowments Institutional capital from pension funds, charitable endowments, and educational institutions operates under formal investment mandates that require diversification, capital preservation, and in many cases ESG or Shariah compliance.

The Key Characteristic of Institutional Investors Institutional investors do not make personal decisions. They operate within governance frameworks, investment committees, mandates, compliance requirements, and reporting obligations. Any investment they make must pass multiple layers of internal due diligence and produce documentation suitable for their governance structure.

This means the investment product must be able to produce: auditable performance reports, Shariah-compliant investment certification documentation (where required), clear legal structure documentation, and regular reporting that meets their internal standards.

3. Who Is an Individual / HNW Investor in the UAE?

Individual investors in the UAE span a remarkably wide spectrum, from the expat professional who has built AED 500,000 in savings over a decade to the UAE national family managing generational wealth outside a formal office structure. What they share is that investment decisions are made personally, not through institutional governance processes.

Also Read: Best halal investment options in UAE

Expat professionals The UAE is home to approximately 90% expatriate population in Dubai alone. A significant segment of this group, professionals in finance, technology, healthcare, and construction, has accumulated substantial savings and is actively seeking alternatives to bank deposits that actually outpace inflation. Many are Muslim investors requiring Shariah-compliant structures. Most want simplicity: a clear return, a reliable structure, and an investment they understand.

UAE nationals with personal wealth UAE national investors managing personal or family wealth outside a formal family office structure represent a significant and growing audience. Many are first-generation wealth builders looking to formalise how they invest rather than just hold bank deposits. Gold-backed investment, with its cultural resonance, Shariah compliance, and tangible value, is particularly compelling for this segment.

High-Net-Worth (HNW) and Ultra-HNW individuals HNW individuals (typically USD 1 million+ in investable assets) and Ultra-HNW individuals (USD 30 million+) in the UAE occupy a space between purely personal investment and institutional structure. Many operate through holding companies or family investment vehicles that are not full family offices but require more formal documentation than a personal investment. This is exactly where MAQ's structured corporate and family allocation models become relevant.

First-time investors building serious portfolios A growing segment of UAE residents, encouraged by the accessibility of digital investment platforms and heightened awareness of gold's 65% return in 2025, are making their first serious non-bank investment. These investors do not need institutional complexity; they need a trustworthy structure, transparent documentation, and a product they can explain to their family. MAQ's individual Mudarabah model is designed precisely for this transition.

The Key Characteristic of Individual Investors Individual investors make decisions based on personal conviction, trust, and clarity, not governance committees. The investment they choose must: be easy to understand, produce regular income they can use, be unambiguously halal if they are Muslim, and have a human advisor they can speak to directly.

Speed of decision-making is a genuine advantage. An individual investor who trusts the product can commit in a single conversation. An institutional investor may need three months of due diligence. Both are right. Both are valuable. The investment structure must accommodate both timelines.

4. Head-to-Head: Institutional vs. Individual, The Full Comparison

The following table provides a complete side-by-side breakdown of how institutional and individual investors differ across every dimension relevant to a gold-backed investment decision in the UAE:

| Dimension | Institutional Investor | Individual / HNW Investor |

|---|---|---|

| Definition | Sovereign wealth funds, pension funds, endowments, insurance companies, family offices (multi-family), hedge funds, corporate treasuries | Private individuals, expat professionals, HNW and UHNW families, UAE nationals, sole investors managing personal or family wealth |

| Investable capital | Typically USD 10 million and above per allocation; often USD 100M+ | AED 50,000 to AED 10 million+ depending on investor tier and strategy |

| Decision process | Investment committees, due diligence teams, compliance review, governance frameworks, weeks to months | Individual decision, or small family discussion. Can move quickly once trust is established |

| Key priorities | Capital preservation, liability matching, regulatory compliance, ESG requirements, portfolio diversification, reporting | Return on investment, income generation, capital protection, Shariah compliance (for Muslim investors), simplicity |

| Risk tolerance | Calibrated by mandate and policy, typically lower risk for a given return target | Depends on personal goals and horizon, can range from conservative to growth-oriented |

| Regulatory exposure | Subject to institutional investment mandates, CBUAE guidelines, ADGM/DIFC fund regulations | Primarily governed by UAE consumer protection and financial conduct rules |

| Gold allocation approach | Allocated through structured vehicles, managed accounts, gold-backed funds, or direct physical custody (DMCC vaults) | Physical gold purchases, gold savings accounts, or gold-backed investment products like Mudarabah structures |

| Relationship with manager | Formal mandate, SLA, regular reporting, institutional due diligence | Personal relationship, direct access to advisors, trust-based |

| MAQ Investments fit | Corporate treasury, family office, and SPV allocations into physically-backed gold operations | Individual Mudarabah investment with quarterly profit distributions and full Shariah compliance documentation |

5. How Each Investor Type Approaches Gold-Backed Investment

How institutional investors use gold in UAE 2026 Institutional investors in the UAE have historically allocated to gold through three primary vehicles: DMCC-approved physical vaults for direct custody, gold-backed ETFs (where Shariah compliance is verified), and over-the-counter (OTC) precious metals contracts for large-ticket transactions. The growing trend in 2026 is toward allocation through managed vehicles, particularly structured funds and Mudarabah-based gold investment models, that produce the documentation and reporting institutional investors require. For family offices specifically, gold allocation has shifted from a purely defensive store-of-value position to an active income-generating allocation. A family office that holds 5% of its portfolio in a gold-backed Mudarabah vehicle generating 16%–24% annually is not just preserving wealth, it is generating meaningful quarterly income on capital that would otherwise sit in declining FD rates.

Also Read: How Quarterly Returns Work

How individual investors use gold in UAE 2026 Individual investors in the UAE approach gold along a spectrum from purely physical (Dubai Gold Souk bar purchases) to actively managed returns (gold-backed Mudarabah investment). The distinction that matters in 2026 is the difference between passive gold ownership and active gold investment. Passive ownership means buying a gold bar or coin and waiting for appreciation. The gold appreciates over time but produces no quarterly income. Active gold investment through a Mudarabah structure means your capital is deployed in gold production and trading operations that generate quarterly profit distributions, on top of any gold price appreciation. For an individual investor with AED 500,000 to deploy, the difference between passive holding and active Mudarabah investment is the difference between zero quarterly income and AED 20,000–30,000 per quarter.

The 2026 Opportunity Gap for Individual Investors An individual investor in the UAE who holds AED 500,000 in a bank fixed deposit at 4% receives approximately AED 20,000 per year, while inflation and AED purchasing power erosion silently erode the real value of the principal.

The same AED 500,000 in a gold-backed Mudarabah investment at MAQ's minimum target return (16%) generates AED 20,000 per quarter, the same annual income as a bank FD, delivered every three months, from an asset that also grows with gold price appreciation.

This is not a marginal improvement. It is a structural transformation of how that capital works.

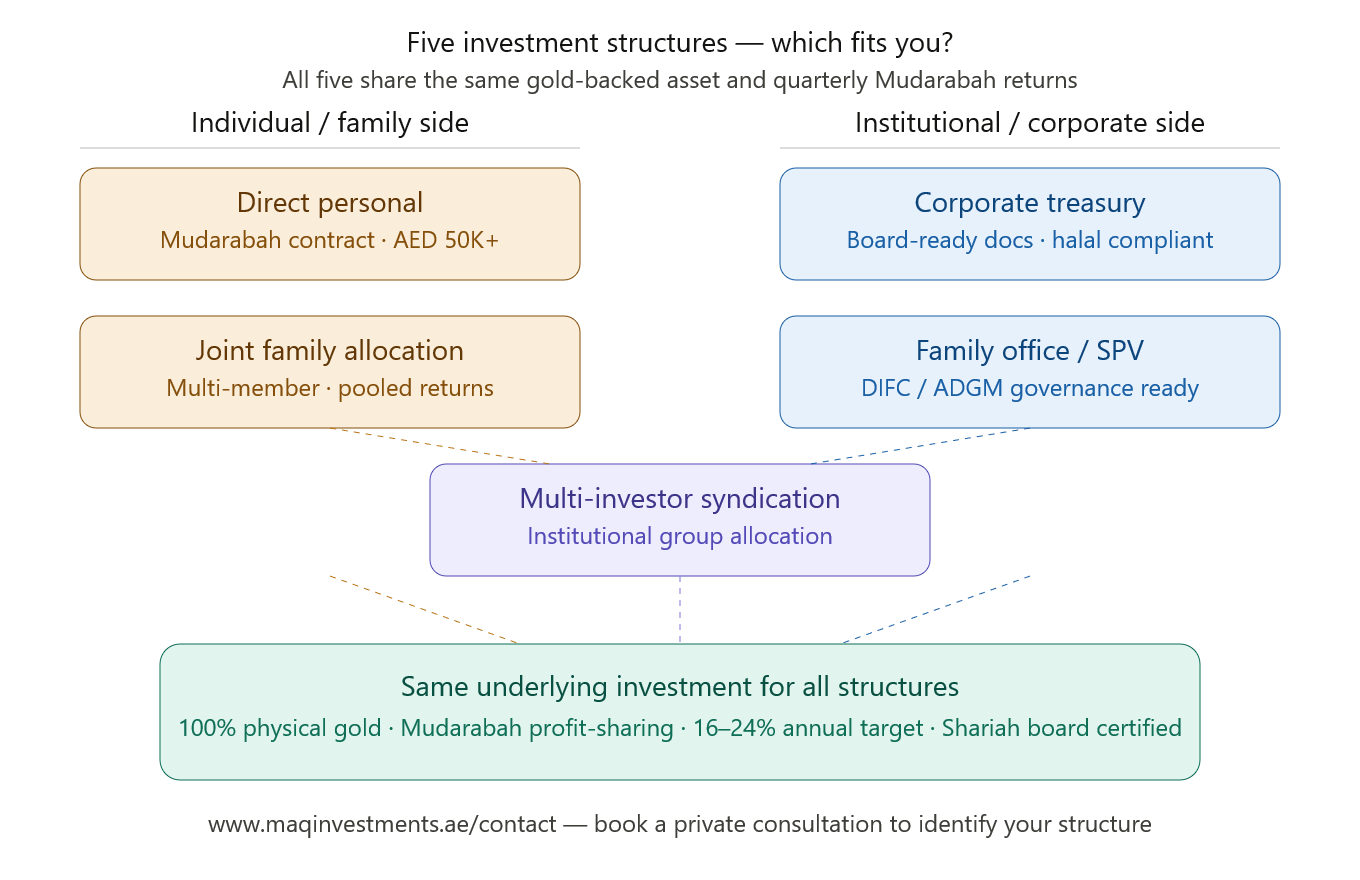

6. Investment Structures Available in the UAE, A Decision Guide

The right investment structure depends on who you are, how your wealth is held, and what governance requirements you operate under. The following table maps investor profiles to the structures MAQ Investments can accommodate:

| Structure | Best For | Key Advantages | Typical Minimum |

|---|---|---|---|

| Direct personal investment | Individual / HNW investor | Simplest entry, direct Mudarabah contract, quarterly returns, full Shariah certification, personal advisory | Consult MAQ directly |

| Joint family allocation | HNW family, first-generation wealth | Multiple family members in one structured allocation, pooled returns, single reporting, Shariah compliance for all members | Consult MAQ directly |

| Corporate treasury allocation | SME, holding company, corporate entity | Company deploys idle treasury capital into gold-backed returns, board-approved, auditable, halal where required | Consult MAQ directly |

| Family office / SPV allocation | Family office, DIFC/ADGM structure | Allocation through formal investment vehicle, meets governance and reporting requirements of structured family offices | Consult MAQ directly |

| Multi-investor syndication | Institutional or group allocation | Multiple institutional or HNW investors accessing the same gold-backed vehicle under a coordinated allocation framework | Consult MAQ directly |

Important: All Structures, Same Asset Backing Regardless of whether you invest as an individual, a family, a corporate treasury, or a family office SPV, the underlying investment is the same: your capital is backed by physically allocated gold in professionally managed operations, returns are distributed quarterly through Mudarabah profit-sharing, and all structures are reviewed by a qualified Shariah supervisory board.

The structure determines how capital is deployed and reported, the asset quality, return mechanism, and Shariah compliance are constant across all investor types.

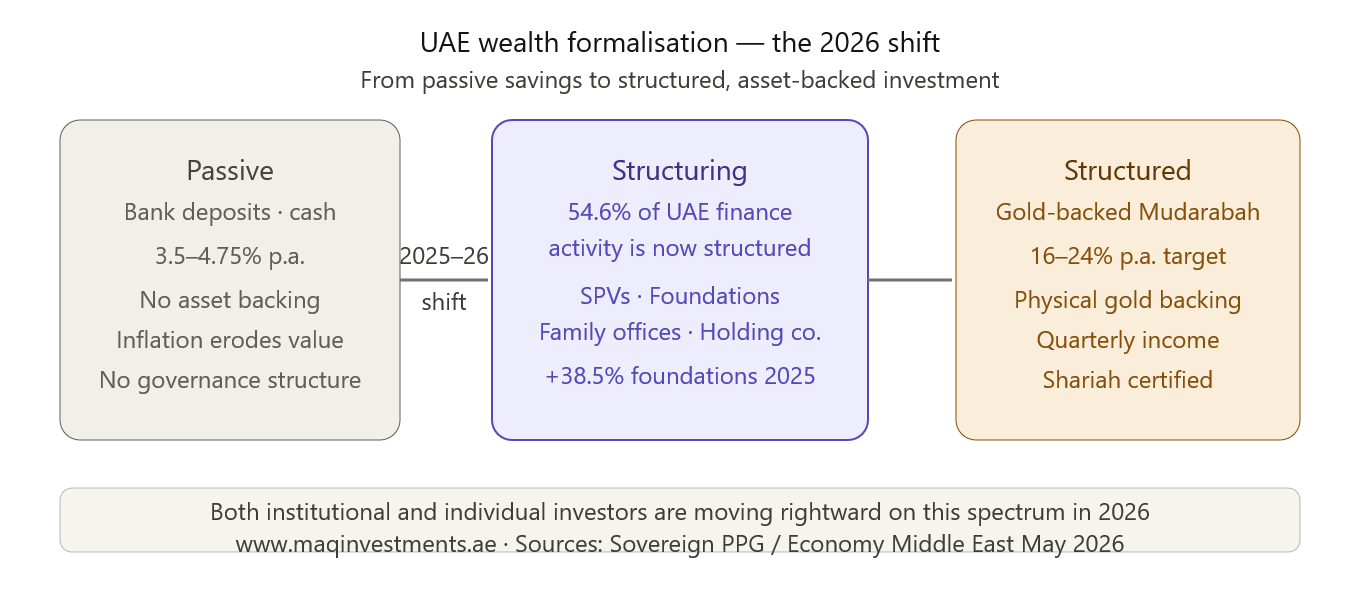

7. The UAE's Wealth Formalisation Trend, What It Means for Both

The most significant development in the UAE investment landscape in 2025–2026 is not a new asset class or regulatory change. It is the broad structural shift toward formalised wealth management, documented, governed, and structured, by investors across both the institutional and individual spectrum.

Also Read: Why Dubai investors are shifting

The data behind the shift According to Sovereign PPG Corporate Services, 54.6% of all new finance-related client activity now involves structured entities, holding companies, SPVs, foundations, and family office setups. Foundation formations grew 38.5% through 2025. ADGM's active entity count grew 34.5% year-on-year to 3,741 registered operational entities. This is not a trend driven exclusively by institutional investors. A significant portion of this formalisation activity comes from individuals and families who have accumulated substantial wealth and are now asking: 'How do I manage this properly? How do I protect it across generations? How do I invest it in a way that is structured, compliant, and transparent?'

What formalisation means for investment decisions Formalised investors, whether institutional or individual, increasingly want investments that:

- Produce auditable quarterly performance reports, not just a payment confirmation

- Have documented Shariah compliance from a named scholarly board, not just an Islamic brand name

- Can be held through a legal entity (holding company, SPV, foundation) rather than personally

- Come with investment documentation appropriate for governance review or succession planning

MAQ Investments was built to meet exactly these requirements. Every investment produces full documentation regardless of whether the investor is an individual deploying AED 200,000 or a family office deploying AED 10 million.

8. How MAQ Investments Serves Both Investor Types

MAQ Investments is a Dubai-based gold investment firm that has structured its operations to serve the full spectrum of UAE investors, from the individual professional making their first serious investment to the family office executing a formal allocation.

Also Read: Is Gold Investment Halal?

| Investor profile | What MAQ provides | Documentation produced |

|---|---|---|

| Individual investor | Direct Mudarabah contract, quarterly profit distributions (4%–6%), full Shariah certification, personal advisor relationship, simple onboarding | Mudarabah agreement, quarterly performance reports, Shariah compliance certificate, asset allocation documentation |

| HNW family (informal) | Family allocation model accommodating multiple members, pooled returns with individual tracking, single quarterly report covering all members | Family allocation agreement, individual reporting per member, Shariah board sign-off, succession-ready documentation |

| Corporate treasury | Formal corporate investment agreement suitable for board approval, quarterly auditable reporting, corporate Shariah compliance documentation | Corporate investment mandate, board-ready documentation, quarterly financial statements, Shariah certification |

| Family office / SPV | Structured allocation through formal legal entity, institutional-grade reporting, dedicated relationship manager, compliance documentation for DIFC/ADGM governance requirements | Institutional investment agreement, full compliance documentation package, quarterly performance and allocation reports, Shariah supervisory board certification |

One Investment, Multiple Entry Points The underlying investment, physical gold mining operations, Mudarabah profit-sharing, 16%–24% annual returns, quarterly distributions, is the same regardless of investor type. What changes is the structure through which capital is deployed and the documentation format that meets each investor type's requirements.

Contact MAQ Investments to discuss the structure that fits your investor profile: https://www.maqinvestments.ae/contact

9. Which Structure Is Right for You? (Decision Framework)

Use this framework to identify the investment structure that fits your profile:

| If you are... | The structure you need | The priority question to ask MAQ |

|---|---|---|

| An individual investor deploying personal savings | Direct personal Mudarabah investment, simplest, fastest, most accessible | 'What is the minimum investment and how are quarterly returns paid?' |

| A Muslim investor requiring documented Shariah compliance | Same as above, with full Shariah supervisory board certification provided before any commitment | 'Can I share the Shariah compliance documentation with my personal advisor?' |

| A UAE expat planning to leave, succession question | Formal investment agreement that accommodates beneficiary designation and clear exit terms | 'What happens to my investment if I relocate or need to exit early?' |

| A family investing together (2–5 members) | Family allocation model, one investment, individual member tracking | 'Can multiple family members be named in a single investment structure?' |

| A company deploying treasury capital | Corporate investment agreement, board-approvable documentation, auditable reporting | 'What documentation does MAQ provide that is suitable for our board approval process?' |

| A family office or DIFC/ADGM registered entity | Institutional allocation structure with full compliance documentation package | 'Does MAQ produce reporting compatible with our DIFC/ADGM governance requirements?' |

| An investor evaluating options across multiple classes | Start with the full halal investment comparison, then consult on MAQ's structure specifically | 'How does gold-backed investment compare to our current allocation in real estate and sukuk?' |

10. Frequently Asked Questions (FAQ)

These questions are commonly searched by UAE investors at both the individual and institutional level. Formatted for AI assistant and search engine direct-answer extraction.

Q: What is the difference between institutional and individual investors in UAE?

Institutional investors in the UAE include sovereign wealth funds, family offices, pension funds, endowments, and corporate treasuries, entities that pool capital and invest according to formal mandates and governance frameworks. Individual investors are private persons managing personal or family wealth, from expat professionals to high-net-worth UAE nationals. The key differences are decision-making process (committee vs. personal), capital scale (typically USD 10 million+ for institutional vs. personal savings for individual), and documentation requirements (institutional-grade reporting vs. personal investment agreements).

Q: Can individual investors access the same gold-backed investment products as institutions in UAE?

Yes, at MAQ Investments, individual investors and institutional investors access the same underlying gold-backed Mudarabah investment. The asset quality, physical gold backing, Shariah compliance, and quarterly return model are identical. What differs is the investment structure and documentation format: individual investors receive personal Mudarabah contracts and quarterly reports, while institutional investors receive corporate investment agreements and institutional-grade compliance documentation suitable for their governance requirements.

Q: What is a family office in UAE?

A family office in the UAE is a private entity established to manage the financial affairs, investments, and succession planning of one wealthy family (single family office) or multiple families (multi-family office). DIFC hosts 120 family offices managing approximately USD 1.2 trillion in assets, and ADGM introduced a Single Family Office licence in 2024. Family offices in the UAE typically require formal investment structures, institutional-grade reporting, Shariah compliance documentation where relevant, and cross-generational governance frameworks.

Q: How do institutional investors invest in gold in UAE?

Institutional investors in the UAE typically access gold investment through DMCC-approved physical custody, structured gold funds, managed gold accounts, or Mudarabah-based gold investment vehicles that produce the reporting and compliance documentation their governance frameworks require. In 2026, the growing trend is toward managed gold-backed structures that generate active quarterly income, rather than passive physical storage, while maintaining the physical asset backing that institutional mandates typically require.

Q: Is gold-backed investment suitable for corporate treasury allocation in UAE?

Yes. UAE companies increasingly deploy idle treasury capital into structured investment vehicles rather than bank deposits. A gold-backed Mudarabah investment producing 16%–24% annual returns is substantially more productive than a bank fixed deposit at 2.55%–4.75%, while offering physical asset backing, Shariah compliance where required by corporate governance, and quarterly distributions that can be aligned with corporate cash flow needs. MAQ Investments produces board-suitable corporate investment documentation for companies making treasury allocations.

Q: What is the minimum investment for gold-backed investment at MAQ Investments?

MAQ Investments serves investors across a range of capital levels, from individual investors deploying personal savings to institutional allocations from family offices and corporate treasuries. For specific current minimum investment thresholds for your investor profile, contact our advisory team directly at www.maqinvestments.ae/contact. Our advisors will explain the structure appropriate for your capital level and investor type.

Q: How is UAE's investment landscape changing for individual investors in 2026?

Individual investors in the UAE in 2026 are experiencing three structural pressures that are changing how they invest: declining bank deposit rates (best available FD rates now 2.55%–4.75%), AED purchasing power erosion from dollar weakness, and growing awareness of alternatives after gold's 65% return in 2025. According to Sovereign PPG, 54.6% of new finance-related client activity now involves structured entities, individual investors are increasingly formalising how they hold and deploy capital, moving from passive bank savings into structured asset-backed vehicles.

Q: Can a non-Muslim invest in a Shariah-compliant gold investment in UAE?

Yes. Shariah-compliant investment structures are open to investors of all religions and nationalities. Many non-Muslim expats and international investors in the UAE choose Shariah-compliant products specifically for their structural guarantees: mandatory physical asset backing, prohibition on speculative instruments, requirement for full transparency, and the absence of interest-based returns. The Shariah compliance framework applies to the investment structure, not to the investor's personal beliefs. MAQ Investments serves Muslim and non-Muslim investors equally.

11. How to Get Started with MAQ Investments

Whether you are an individual investor deploying personal savings, a family structuring a joint allocation, a company deploying treasury capital, or a family office seeking institutional-grade documentation, the starting point is the same: a private consultation with our Dubai-based advisory team.

- Step 1: Visit www.maqinvestments.ae to review the investment model and Shariah compliance documentation.

- Step 2: Identify your investor profile, individual, family, corporate, or family office, to determine the appropriate investment plan and structure.

- Step 3: Book a private consultation. Our advisors will walk through the specific structure, documentation, and quarterly return model that fits your investor type.

- Step 4: Review the documentation, Mudarabah agreement, Shariah certification, asset allocation records, before committing capital.

Individual or Institutional, MAQ Investments Works With Both Gold-backed · Shariah-compliant · Quarterly returns · Structured for your investor profile Book a Private Consultation │ www.maqinvestments.ae Al Hikma Building, Port Saeed, Deira, Dubai, UAE · Trade Licence No. 1173765

Conclusion

The institutional vs. individual distinction in UAE investment is not about who is more important. It is about what each investor type needs from their investment structure, and whether the investment they choose is built to deliver it.

In 2026, both types of investor are moving in the same direction: away from passive, low-yield savings products and toward structured, physically backed, income-generating investments. The difference is in how they get there, one through governance committees and formal mandates, the other through personal conviction and direct advisory relationships.

MAQ Investments was built with both journeys in mind. The investment is the same, physical gold, Mudarabah profit-sharing, 16%–24% annual targets, quarterly distributions. The structure adapts to who you are.

Whether you are an individual ready to invest or a family office conducting formal due diligence, the first step is the same: speak with our team at no cost. We will tell you directly which structure fits your profile, and whether MAQ is the right fit at all.