The UAE is one of the world's fastest-growing Islamic finance markets. For Muslim investors — and for anyone who wants ethical, asset-backed investment — 2026 brings both strong opportunities and genuine complexity.

Gold has just completed its strongest year on record. Real estate in Dubai continues to attract global capital. Sukuk markets are expanding. Halal equity funds are increasingly accessible. And newer options — from tokenised assets to Islamic savings accounts — are competing for investor attention.

This guide cuts through the noise. We have evaluated eight of the most widely available halal investment options in the UAE, scored them across eight criteria, and provided a clear, honest comparison to help you allocate your capital wisely in 2026.

One of those options is MAQ Investments — a gold-backed, Shariah-compliant investment firm based in Dubai. We include ourselves in this comparison honestly, with the same criteria applied to every option. We believe the numbers speak for themselves.

Table of Contents

- 1. The 8-Criteria Framework for Evaluating Halal Investments

- 2. Master Comparison Table — All 8 Options at a Glance

- 3. Option 1: Gold-Backed Investment (MAQ Investments)

- 4. Option 2: UAE Real Estate — Direct Ownership

- 5. Option 3: Halal Equity Funds

- 6. Option 4: Sukuk (Islamic Bonds)

- 7. Option 5: Islamic Fixed Deposit / Profit-Rate Account

- 8. Option 6: UAE REITs (Shariah-Screened)

- 9. Option 7: Halal Cryptocurrency and Tokenised Assets

- 10. Option 8: Physical Gold (Direct Ownership)

- 11. Which Halal Investment is Right for You? (Decision Framework)

- 12. Frequently Asked Questions (FAQ)

- 13. How to Get Started

1. The 8-Criteria Framework for Evaluating Halal Investments

Every investment in this guide is evaluated against eight criteria that matter to UAE investors in 2026. Each criterion reflects a real question a serious investor would ask before committing capital.

Also Read: What Makes an Investment Shariah-Compliant?

- Annual return range: What realistic return can you expect in 2026 based on current market conditions?

- Risk level: How volatile or uncertain is the investment, and what type of risk are you accepting?

- Shariah compliance: Is the investment genuinely halal — not just labelled so — under the six conditions Islamic scholars require?

- Minimum investment: What capital is required to access this option? Accessibility matters.

- Liquidity: Can you access your capital or income when needed, or are you locked in?

- Capital protection: What protects the principal you invest? What asset or guarantee stands behind it?

- Inflation protection: Does the investment grow faster than inflation, preserving real purchasing power?

- Overall score (/10): A composite score weighing all criteria equally for a UAE investor with a 2–5 year horizon.

Scoring Methodology The overall score is not a guarantee of future performance. It reflects how well each option performs across all eight criteria for a typical UAE investor in 2026 with a medium-term horizon (2–5 years), moderate risk tolerance, and a requirement for genuine Shariah compliance. A high score on one criterion (e.g. return) does not compensate for a failing on another (e.g. Shariah compliance). An investment that fails the Shariah test cannot score above 5/10 regardless of its financial performance.

2. Master Comparison Table — All 8 Options at a Glance

The following table provides a complete side-by-side comparison. Detailed analysis of each option follows in Sections 3–10.

| Investment Option | Return Range | Risk | Shariah Status | Min. Investment | Liquidity | Capital Protection | Inflation Hedge | Score /10 |

|---|---|---|---|---|---|---|---|---|

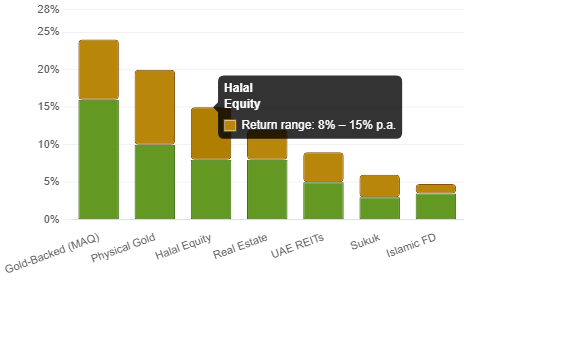

| Gold-Backed Investment (MAQ Investments) | 16%–24% | Medium | Fully Halal | Consult MAQ | Quarterly income | Physical gold backing | Strong | 9/10 |

| UAE Real Estate (Direct ownership) | 6%–12% | Medium | Halal (with conditions) | AED 500,000+ | Low — illiquid | Backed by property | Moderate | 7/10 |

| Halal Equity Funds (Screened stocks) | 8%–15% | Medium-High | Halal (screened) | AED 1,000+ | High — daily liquidity | Market-dependent | Moderate | 7/10 |

| Sukuk (Islamic Bonds) | 3%–6% | Low-Medium | Halal | AED 10,000+ | Medium — secondary market | Issuer creditworthiness | Weak | 6/10 |

| Islamic Fixed Deposit / Profit-Rate | 3.5%–4.75% | Very Low | Halal (verify) | AED 2,500+ | Low — locked term | Bank balance sheet | Weak | 5/10 |

| UAE REITs (Shariah-screened) | 5%–9% | Medium | Halal (screened) | AED 500+ | High — listed | Portfolio properties | Moderate | 6/10 |

| Halal Cryptocurrency / Tokenised Assets | Highly variable | Very High | Debated | AED 100+ | High but volatile | None or unclear | Unclear | 3/10 |

| Physical Gold (direct ownership) | 10%–20%* | Medium | Halal | AED 200+ | Moderate | The gold itself | Strong | 7/10 |

Physical gold annual return based on 10-year average appreciation, not a guaranteed rate.

3. Option 1: Gold-Backed Investment (MAQ Investments)

Score: 9/10

We include MAQ Investments in this comparison not as self-promotion, but because it represents the asset class — physically-backed, Mudarabah-structured gold investment — that ranks highest on our evaluation criteria. We apply the same honest standards to ourselves as to every other option here.

Also Read: Is Gold Investment Halal?

What it is A gold-backed investment through MAQ Investments places your capital into gold production and trading operations. Returns are generated through actual gold performance — production revenue, trading margin, and gold price movement — and distributed quarterly through a Mudarabah profit-sharing structure.

Returns MAQ Investments targets an annual return of 16% to 24%, distributed quarterly at 4% to 6% per quarter. These are performance-based targets, not guaranteed interest rates. Returns reflect actual gold operations each quarter.

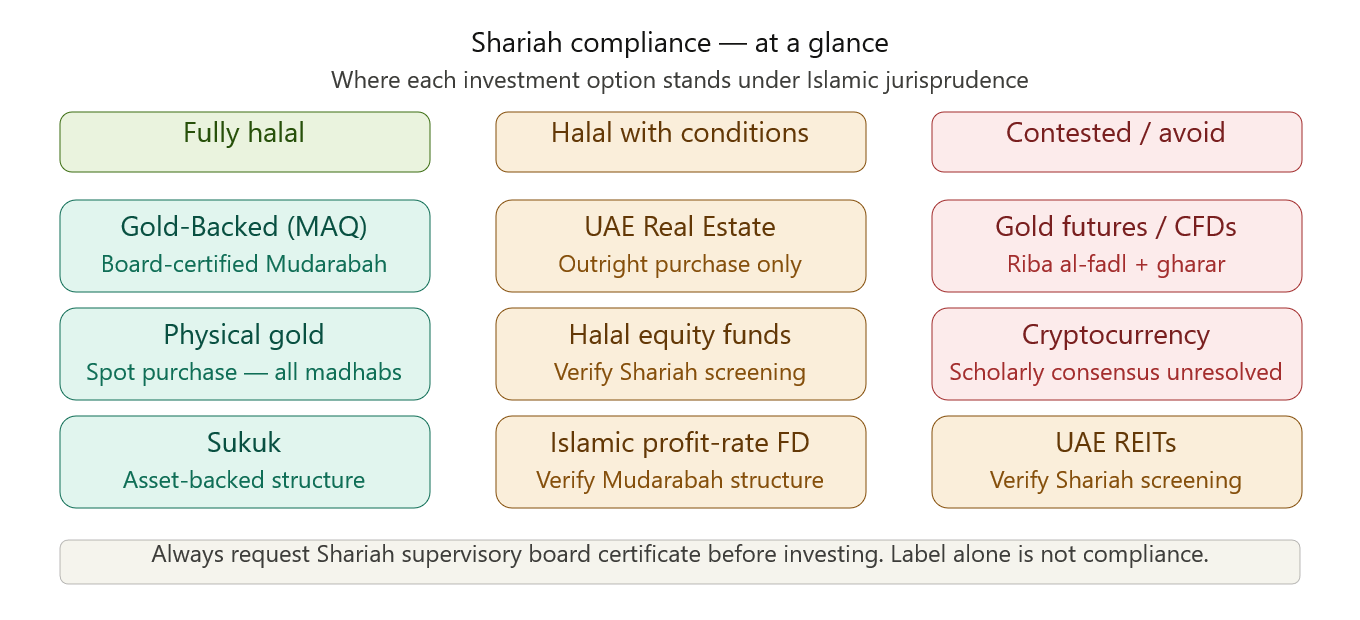

Shariah compliance The investment is fully Shariah-compliant: 100% physical gold backing (no unallocated or paper gold), Mudarabah profit-sharing with no riba, no gharar (full quarterly reporting), halal sector operations, and ongoing Shariah supervisory board review.

Who it suits

- Investors with a 2–5 year horizon seeking above-average halal returns

- Muslim investors who require genuine, documented Shariah compliance

- UAE residents and expats wanting quarterly income from a real asset

- Investors concerned about inflation and dollar weakness in 2026

Considerations

- Returns vary with gold market performance — not a fixed rate

- Better suited for medium-term investors than short-term capital deployment

MAQ Investments — Key Facts

- Return target: 16%–24% per annum (4%–6% quarterly)

- Structure: Mudarabah profit-sharing from gold production

- Capital backing: 100% physically allocated gold

- Shariah: Certified by qualified supervisory board

- Distribution: Quarterly — after each performance period closes

- Location: Al Hikma Building, Port Saeed, Deira, Dubai, UAE

4. Option 2: UAE Real Estate — Direct Ownership

Score: 7/10

UAE real estate — particularly Dubai — remains one of the most sought-after investment markets globally. Direct property ownership delivers rental income plus capital appreciation and is generally considered halal when purchased outright (not through interest-based mortgages).

Also Read: What is Shariah-Compliant Investment?

Returns Rental yields in Dubai average 6%–8% per annum in 2026, with capital appreciation adding 3%–5% in growing areas. Prime locations (Downtown, Marina, Business Bay) may yield less but appreciate more strongly. Total returns of 8%–12% per year are realistic for well-selected properties.

Shariah compliance Direct ownership of property is halal. However, buying with a conventional interest-bearing mortgage makes the investment haram. Islamic home finance (Ijarah or Murabahah structures) exists in the UAE and makes property accessible without riba — but must be specifically requested from lenders who offer it.

Considerations

- High minimum investment — entry typically from AED 500,000 for quality properties

- Illiquid — selling takes weeks to months; not suitable if you may need capital quickly

- Transaction costs (DLD fees, agent fees) can reach 5–7% of purchase price

- Rental management requires active involvement or a property manager

- Outstanding option for long-term wealth building and inheritance planning

5. Option 3: Halal Equity Funds

Score: 7/10

Halal equity funds invest in screened stocks — companies that pass Islamic finance sector and financial ratio tests. They exclude alcohol, tobacco, weapons, gambling, adult entertainment, pork, and conventional banks. The remaining universe of halal stocks is broad and diversified.

Also Read: Gold-Backed Investment vs. Fixed Deposits

Returns Well-managed halal equity funds have historically delivered 8%–15% annual returns over five-year periods, roughly tracking or slightly lagging conventional equity indices due to sector exclusions. In 2026, technology, healthcare, and industrial sectors — all halal-compatible — are performing strongly.

Shariah compliance Genuine halal equity funds are screened and certified by Shariah supervisory boards. Key checks: sector exclusions are applied, financial ratios (debt to equity, interest income percentage) are within permitted thresholds, and impure income is purified. Always verify the fund's Shariah certificate before investing.

Considerations

- Returns are variable and can be negative in market downturns

- Low minimum investment — accessible from AED 1,000 via some platforms

- High liquidity — daily trading for most listed funds

- Sector concentration in technology and healthcare introduces specific macro risks

6. Option 4: Sukuk (Islamic Bonds)

Score: 6/10

Sukuk are Islamic investment certificates that represent ownership in a tangible asset, usufruct, or project. They function similarly to bonds in terms of income profile but are structured to avoid interest, with returns derived from the underlying asset's revenue or lease income.

Returns UAE government Sukuk typically yield 3%–4.5% per annum. Corporate Sukuk from UAE issuers range from 3.5% to 6% depending on credit rating and tenor. The Abu Dhabi and Dubai governments are among the world's most prolific Sukuk issuers, making the UAE a deep Sukuk market.

Shariah compliance Major UAE Sukuk are certified by leading Shariah boards. However, not all Sukuk are equal — some structures have been criticised by scholars. Ijarah Sukuk (lease-based) and Musharakah Sukuk are generally considered the most robust structures.

Considerations

- Returns are relatively modest compared to equity or gold investments

- Lower risk profile — suitable for capital preservation with modest halal income

- Interest rate sensitivity — Sukuk prices fall when conventional rates rise

7. Option 5: Islamic Fixed Deposit / Profit-Rate Account

Score: 5/10

Islamic profit-rate accounts are the Shariah-compliant equivalent of conventional term deposits. Structured as Mudarabah or Wakalah arrangements, they offer a profit rate rather than an interest rate.

Returns UAE Islamic banks offer profit rates of approximately 3.5% to 4.75% per annum in early 2026, slightly higher than conventional FDs. Rates are declining as global interest rates fall in 2026.

Shariah compliance Generally Shariah-compliant from certified Islamic banks in the UAE. Verify that the account is genuinely Mudarabah or Wakalah-based.

Considerations

- Lowest return of all options reviewed — likely below real inflation in 2026

- Capital is locked for the agreed term — early withdrawal carries penalties

- Best suited for emergency fund allocation or very short-term savings

8. Option 6: UAE REITs (Shariah-Screened)

Score: 6/10

Real Estate Investment Trusts (REITs) allow investors to participate in UAE property markets with much lower minimum investment than direct ownership. Shariah-screened REITs additionally pass Islamic finance compliance tests.

Returns UAE Shariah-compliant REITs have delivered 5%–9% per annum returns in recent years, combining rental income distributions with unit price appreciation. Emirates REIT is the most prominent Shariah-certified option on Nasdaq Dubai.

Shariah compliance Excludes properties involved in prohibited activities and limits interest-bearing debt beyond AAOIFI thresholds (typically less than 33% leverage).

Considerations

- Much lower entry point than direct property — accessible from AED 500+

- High liquidity — listed and tradeable on Nasdaq Dubai

- Subject to real estate market cycles — unit price can fall

9. Option 7: Halal Cryptocurrency and Tokenised Assets

Score: 3/10

Cryptocurrency and blockchain-based investment have attracted significant attention in the UAE. Several scholars and Islamic finance bodies have issued opinions on cryptocurrency's permissibility — with no consensus reached.

Returns Extremely variable. Bitcoin alone has delivered both 200% annual gains and 65% annual losses in recent years. Tokenised real assets offer a more stable profile but remain early-stage.

Shariah compliance The scholarly consensus is not settled. AAOIFI has not issued a definitive ruling. Many scholars consider it problematic due to its speculative nature, while others permit it subject to spot settlement conditions.

Our Honest Assessment Cryptocurrency does not currently meet the bar of 'clearly halal' that we apply to all investments we recommend. Serious Muslim investors should approach with caution.

10. Option 8: Physical Gold (Direct Ownership)

Score: 7/10

Buying physical gold — coins, bars, or certified bullion — is one of the oldest and most universally endorsed forms of halal wealth preservation.

Returns Gold delivered approximately 65% return in 2025 and has averaged approximately 10%–11% annually over the past 25 years. Physical gold ownership captures this appreciation directly.

Shariah compliance Physical gold purchased for spot settlement is halal under all four major madhabs. Key conditions: immediate exchange, genuine ownership, and no interest component.

Considerations

- No income — physical gold does not pay quarterly distributions or dividends

- Storage and security cost money

- Selling requires finding a buyer — less liquid than a listed investment

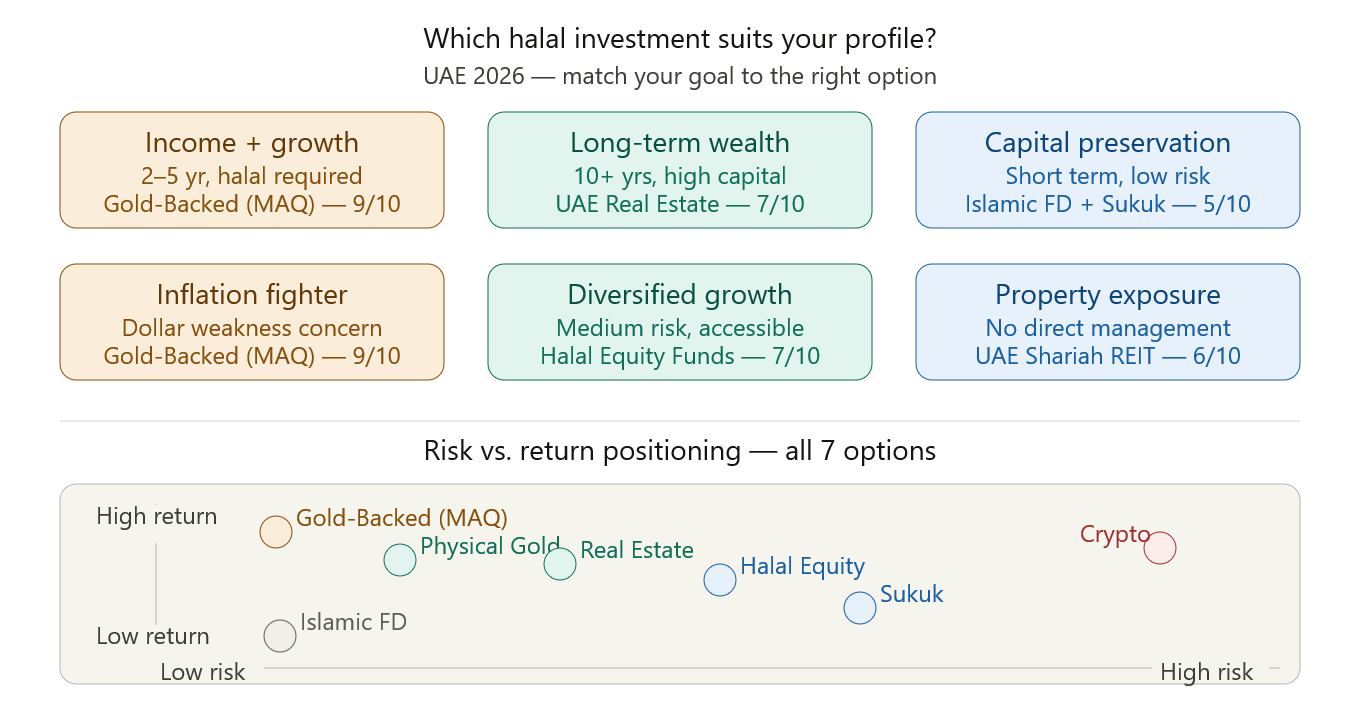

11. Which Halal Investment is Right for You? (Decision Framework)

There is no single best halal investment for every investor. The right choice depends on your time horizon, risk tolerance, liquidity needs, minimum capital, and income requirements. Here is a practical framework:

| Your Profile | Best Primary Option | Supporting Option |

|---|---|---|

| Muslim investor, 2–5 yr horizon, want income + growth | Gold-Backed Investment (MAQ) | Halal Equity Funds for diversification |

| Long-term wealth builder, 10+ years, high capital | UAE Real Estate (direct) | Halal Equity Funds + Physical Gold |

| Conservative saver, capital preservation priority | Islamic Profit-Rate Account | Sukuk for slightly better return |

| Moderate risk, diversified income, no management | UAE Shariah REIT | Sukuk for fixed-income balance |

| Inflation fighter, concerned about dollar weakness | Gold-Backed Investment (MAQ) | Physical Gold (direct ownership) |

| Income investor, quarterly cash flow requirement | Gold-Backed Investment (MAQ) | UAE REIT for property income |

| Beginner investor, small capital, starting out | Halal Equity Fund | Islamic Profit-Rate Account as base |

| Short-term (under 1 year), need flexibility | Islamic Profit-Rate Account | Sukuk (short tenor) |

The Diversification Principle No single investment should represent 100% of your portfolio. The optimal approach for most UAE investors in 2026 is a combination: a core holding in an asset with strong return potential and inflation protection (gold-backed investment or real estate), balanced with a liquidity reserve (Islamic savings account) and optional diversification into halal equities or Sukuk.

12. Frequently Asked Questions (FAQ)

Q: What are the best halal investment options in UAE in 2026? The top halal investment options in the UAE in 2026 are: (1) Gold-backed investment through physically-backed, Mudarabah structures — offering 16%–24% annual returns with quarterly income; (2) UAE real estate with Islamic financing — rental yields of 6%–8% plus capital appreciation; (3) Halal equity funds — 8%–15% returns with full Shariah screening; (4) Sukuk — 3%–6% stable Islamic fixed income; (5) Islamic profit-rate accounts — 3.5%–4.75% for short-term capital preservation.

Q: What is the highest return halal investment in UAE? Gold-backed investment through professionally managed Mudarabah structures offers the highest returns among Shariah-compliant options in the UAE, targeting 16%–24% per annum. Halal equity funds rank second at 8%–15% annually over the medium term. Returns always carry risk and are never guaranteed in genuine halal structures.

Q: Is real estate investment halal in UAE? Yes — direct property ownership in the UAE is halal when purchased outright or through Shariah-compliant financing (Ijarah or Murabahah). Buying property with a conventional interest-bearing mortgage makes the transaction haram.

Q: Are Sukuk halal? Yes. Sukuk are the Islamic finance equivalent of bonds and represent ownership in a tangible asset, usufruct, or project. Returns come from asset performance or lease income — not interest.

Q: Is cryptocurrency halal in UAE? The scholarly consensus on cryptocurrency remains unresolved. Some UAE and international Islamic scholars permit buying and selling cryptocurrency as a commodity provided transactions are spot-settled and speculative intent is limited. Others consider the highly speculative nature of crypto problematic under Islamic law.

Q: What is the difference between a halal investment and a conventional investment? A halal investment satisfies four key conditions: no riba (returns come from real business performance, not interest), asset-backed (capital is secured by a tangible asset), no gharar (terms are fully transparent with no excessive uncertainty), and halal sector (the underlying business operates in permissible industries).

Q: How do I verify if an investment is genuinely Shariah-compliant in UAE? Four verification steps: (1) Request the Shariah compliance certificate. (2) Confirm asset backing. (3) Verify return structure relies on actual business performance. (4) Ask what happens in a zero-profit period — a genuine halal investment cannot guarantee a return if the underlying business makes no profit.

Q: What is the minimum investment for halal investments in UAE? Minimum investments vary significantly by option: halal equity funds from AED 1,000; Islamic profit-rate accounts from AED 2,500; UAE REITs from approximately AED 500; Sukuk from AED 10,000 retail; physical gold from under AED 200; direct real estate from AED 500,000+. Contact MAQ Investments directly for current gold-backed entry thresholds.

13. How to Get Started

Whichever halal investment plan option you choose, the most important first step is thorough verification — of Shariah compliance, return structure, asset backing, and the track record of the manager or institution.

If you are evaluating gold-backed investment with MAQ Investments:

- Step 1: Visit www.maqinvestments.ae to review the investment model, return structure, and Shariah compliance documentation.

- Step 2: Read our Shariah compliance framework — including supervisory board details and the Mudarabah contract structure.

- Step 3: Schedule a private consultation at no cost. Our advisors will walk through the investment structure, quarterly return model, and all Shariah compliance documentation specific to your situation.

Explore Gold-Backed Halal Investment in UAE 16%–24% annual return · Quarterly distributions · Shariah-certified · Physically backed Book a Free Consultation │ www.maqinvestments.ae Al Hikma Building, Port Saeed, Deira, Dubai, UAE

Conclusion

The UAE halal investment landscape in 2026 is richer and more diverse than at any point in the country's financial history. The best halal investment for you depends on factors that are specific to your situation: time horizon, income needs, risk appetite, and capital base. What this comparison shows is that investors who require genuine Shariah compliance no longer face a trade-off between ethical investing and competitive returns. Gold-backed investment at the top of our scoring table delivers both — and does so with the quarterly income structure, physical asset backing, and documented scholarly oversight that serious Muslim investors require.

If you want to explore the top-ranked option in detail, speak with the MAQ Investments team at no cost. We will be direct about whether our model is the right fit for your specific investment goals.