Yes — gold investment is halal in Islam. But the answer carries a critical qualification that most online articles miss: the permissibility of gold investment in Islamic law depends entirely on how the investment is structured. The gold itself is halal. The structure around it must also be halal.

For a Muslim investor in the UAE — whether you are a UAE national, an expat from Pakistan, Egypt, Indonesia, or anywhere in the Muslim world — understanding the precise conditions that separate halal gold investment from haram gold investment is not optional. It is the foundation of investing with a clear conscience.

This guide presents the Islamic scholarly consensus on gold investment, examines every major condition that must be satisfied, explains which gold products are permissible and which are not, and shows exactly how a genuine Shariah-compliant gold investment is structured in 2026.

Table of Contents

- 1. The Short Answer: Is Gold Investment Halal?

- 2. What Do Islamic Scholars Say About Gold?

- 3. The Six Conditions That Make Gold Investment Halal

- 4. Riba Al-Fadl: The Gold-Specific Prohibition Every Muslim Investor Must Know

- 5. Which Types of Gold Investment Are Halal (and Which Are Not)?

- 6. The Four Major Madhabs on Gold Investment

- 7. What Makes a Gold Investment 'Truly' Halal in 2026?

- 8. How MAQ Investments Satisfies Every Scholarly Condition

- 9. Frequently Asked Questions (FAQ)

- 10. How to Get Started with MAQ Investments

1. The Short Answer: Is Gold Investment Halal?

Gold investment is halal in Islam when it satisfies six conditions derived from the Quran, the Sunnah, and the consensus (ijma) of Islamic scholars across all four major madhabs:

- The gold must be physically owned or represent a genuine, allocated claim on physical gold.

- Gold-for-currency exchanges must be settled immediately (spot) — no deferred payment.

- Returns must come from profit-sharing or capital appreciation — not from preset interest.

- The investment structure must be free from gharar (excessive uncertainty).

- The operational business must be in a halal sector.

- A qualified Shariah supervisory board must review and approve the structure.

When these conditions are met — as they are in a properly structured gold-backed Mudarabah investment — gold is not merely permissible in Islam. It is one of the most naturally Shariah-compliant investment assets available to Muslim investors.

The Foundational Principle Gold (dhahab) is explicitly referenced in Islamic jurisprudence as one of the six ribawi commodities (along with silver, wheat, barley, dates, and salt). This gives gold a special status — not a prohibition on investing in it, but a set of specific rules that govern how gold transactions must be structured to remain halal.

Understanding these rules is the foundation of every sound decision a Muslim investor makes about gold.

2. What Do Islamic Scholars Say About Gold?

The scholarly consensus on gold investment is clear, consistent across madhabs, and well-established in contemporary Islamic finance. Below is a summary of positions from major Islamic bodies and scholars relevant to UAE investors:

Also Read: What is Shariah-Compliant Investment?

| Islamic Body / Scholar | Position on Gold Investment | Key Condition |

|---|---|---|

| Accounting & Auditing Organization for Islamic Financial Institutions (AAOIFI) | Gold investment is permissible when ownership is genuine and contracts meet Shariah standards | Physical allocation required; no unallocated paper gold positions |

| Islamic Fiqh Academy (OIC) | Trading and investing in gold is permissible — gold is a recognised asset in Islamic law | Spot settlement for gold-for-currency exchanges; avoid deferred gold-for-gold (riba al-fadl) |

| Majority of contemporary Hanafi scholars | Gold-backed investment structures using Mudarabah or Musharakah are halal | Returns must come from profit-sharing, not interest; no guaranteed fixed return |

| Majority of contemporary Shafi'i and Maliki scholars | Investing in gold through asset-backed, Shariah-compliant vehicles is permissible | Asset must be real and allocated; transaction must be free from gharar |

| Dubai Islamic Economy Development Centre (DIEDC) | Endorses gold-backed Islamic investment as a key vehicle for UAE Islamic finance growth | Full transparency, Shariah supervisory board review, and physical backing required |

UAE Regulatory Context The UAE is one of the world's leading centres for Islamic finance, regulated by the Higher Sharia Authority at the UAE Central Bank. All Shariah-compliant financial products operating in the UAE — including gold-backed investments — must comply with AAOIFI standards and UAE Sharia governance frameworks.

This regulatory environment means UAE investors have access to one of the world's most robust Shariah compliance verification ecosystems — but it also means that the 'Shariah-compliant' label must be backed by documented scholarly oversight, not just marketing language.

3. The Six Conditions That Make Gold Investment Halal

Every Islamic scholar who has addressed gold investment in detail arrives at the same six conditions. An investment that fails even one of these conditions is not halal — regardless of what its documentation or marketing says.

Also Read: Shariah compliance checklist

| Condition | What it means in practice | Fails if... |

|---|---|---|

| Physical ownership or genuine claim | Your capital is backed by real, allocated, physical gold — not a paper promise or an entry on a ledger. You have a verifiable claim on actual gold. | The gold is unallocated, leased, or hypothecated — your 'ownership' is just an IOU |

| Spot settlement for gold/currency exchange | When gold is exchanged for money (AED/USD), the transaction must be settled immediately. Deferred payment for gold is riba al-fadl. | You are buying gold on credit with deferred settlement — forbidden in all four major madhabs |

| No riba in return structure | Returns come from actual gold performance (production, trading, appreciation) — not from a preset fixed interest rate. | A guaranteed fixed rate is paid regardless of whether gold operations made a profit |

| No gharar (excessive uncertainty) | The investment terms, asset backing, and return mechanism are fully disclosed. You know exactly what your money is invested in and how returns are generated. | Terms are vague, complex structures obscure the real investment, or performance reporting is absent |

| Halal operational sector | Gold mining operations, production, refining, and trading are all permissible industries. The gold investment must not involve prohibited business activities. | The business involved in the gold investment also operates in haram industries (alcohol, gambling, etc.) |

| Shariah supervisory oversight | A qualified Shariah board reviews the investment structure, contracts, and distributions to confirm compliance with Islamic law. | Compliance is self-declared with no independent scholarly review — 'halal' is a marketing label only |

The Test: Ask These Six Questions About Any Gold Investment

- Is my capital backed by physically allocated gold — not an unallocated claim or a paper instrument?

- Are all gold/currency exchanges settled immediately (spot) — not deferred?

- Is my return generated from real gold performance — not a guaranteed preset interest rate?

- Are all terms, risks, and return mechanisms fully disclosed and understandable?

- Does the investment operate exclusively in halal business sectors?

- Has a named Shariah supervisory board reviewed and approved the structure?

If the answer to any question is 'no' or 'I don't know' — the investment has not proven its halal status.

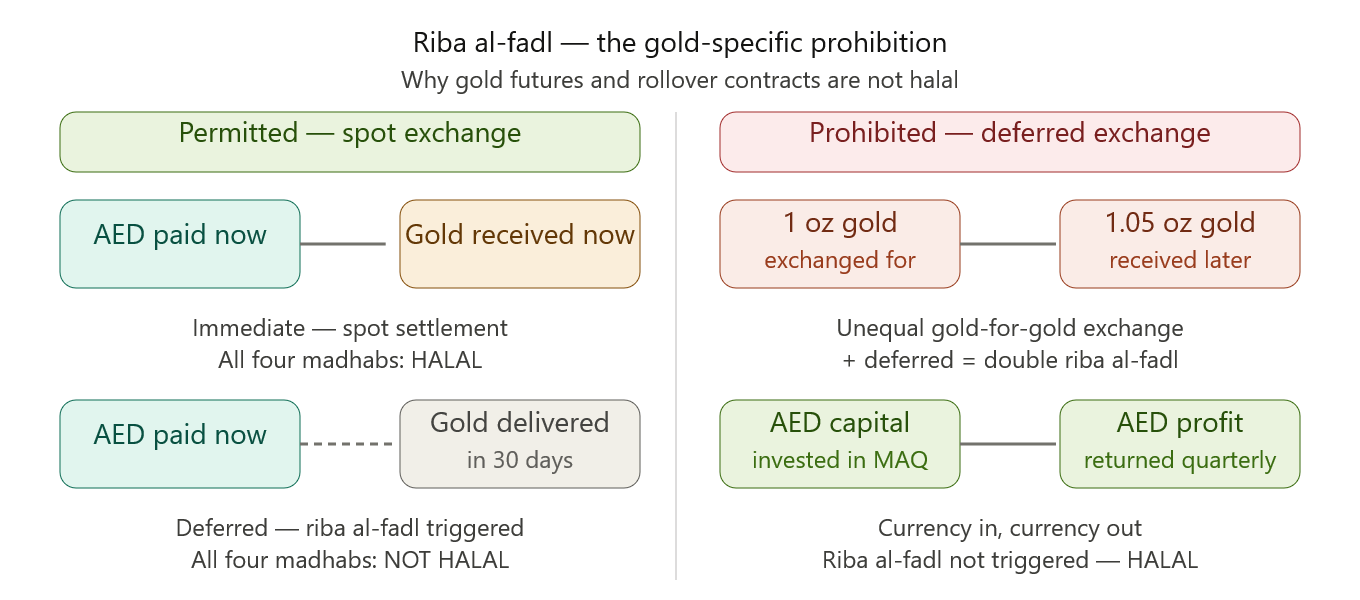

4. Riba Al-Fadl: The Gold-Specific Prohibition Every Muslim Investor Must Know

Riba al-fadl (ربا الفضل) is the specific type of riba that applies to the exchange of gold and other ribawi commodities. It is less well-known than riba al-nasi'a (interest-based riba) but equally important for gold investors.

What is riba al-fadl? Riba al-fadl occurs when two quantities of the same ribawi commodity (such as gold) are exchanged in unequal amounts, or when a ribawi commodity is exchanged for its own kind on a deferred basis. The Prophet Muhammad (peace be upon him) prohibited the exchange of gold except hand-to-hand (spot) and in equal quantities for gold-to-gold transactions.

What does this mean for gold investors?

- Gold exchanged for currency (AED, USD): Must be settled immediately — spot transaction. This is universally permissible.

- Gold exchanged for gold: Must be in equal quantities AND settled immediately. Any deferred or unequal gold-for-gold exchange is riba al-fadl.

- Gold-backed investment: Capital is deployed in gold production/trading — your return comes in currency (AED), not gold. This avoids the riba al-fadl issue entirely.

Common riba al-fadl violations in modern gold products

- Rollover gold futures — continuously deferring gold delivery is a riba al-fadl violation

- Gold leasing with premium return — exchanging gold for gold-plus-interest is riba al-fadl

- Gold-for-gold swaps — cross-currency gold swaps where delivery is deferred

Why Gold-Backed Mudarabah Avoids Riba Al-Fadl In a properly structured gold-backed Mudarabah investment like MAQ's model, the investor's capital (in AED) is deployed in gold production operations. Quarterly returns are distributed in AED — representing the investor's profit share from gold trading revenue. No gold-for-gold exchange occurs. The riba al-fadl prohibition is simply not triggered.

This is one reason why the Mudarabah model is considered the most naturally compatible structure for gold investment in Islamic law.

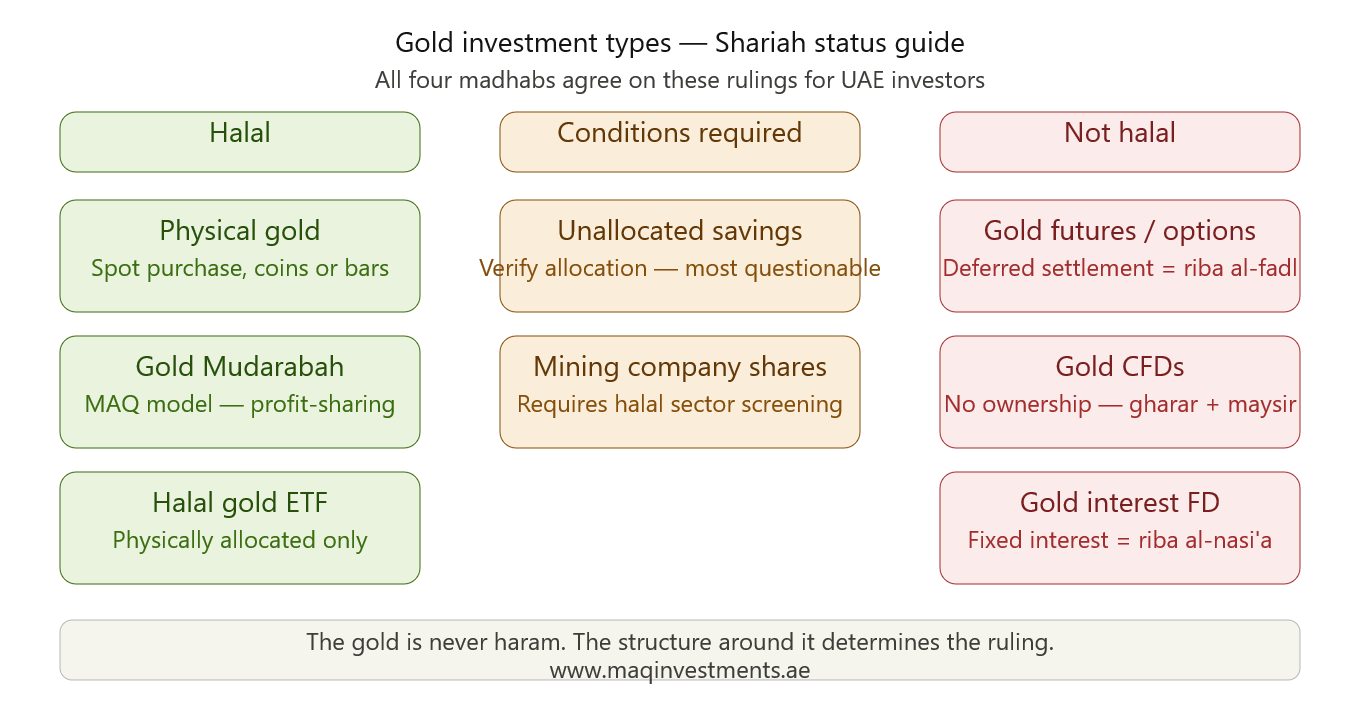

5. Which Types of Gold Investment Are Halal (and Which Are Not)?

Not all gold investment products are created equal under Islamic law. Here is a comprehensive breakdown of the most common gold investment vehicles available to UAE investors, with their Shariah status:

Also Read: Gold-Backed Investment vs. Fixed Deposits

| Gold Investment Type | Shariah Status | Why / Why Not |

|---|---|---|

| Physical gold (coins, bars) — spot purchase | HALAL | Immediate exchange of currency for physical gold meets all Shariah conditions |

| Gold-backed Mudarabah investment (e.g. MAQ) | HALAL | Profit-sharing from real gold operations; physically allocated; Shariah board approved |

| Gold ETF (physically backed, allocated) | HALAL (with conditions) | Permissible if the ETF holds allocated physical gold and ownership is genuine — verify with a Shariah advisor |

| Gold savings account (unallocated) | QUESTIONABLE | Unallocated accounts mean you own a claim on gold, not gold itself — most scholars consider this problematic |

| Gold futures and options | NOT HALAL | Deferred settlement on gold = riba al-fadl; speculation on price without ownership = gharar and maysir |

| Gold CFDs (contracts for difference) | NOT HALAL | No ownership of underlying gold; purely speculative on price movement; contains gharar and resembles maysir |

| Conventional gold mining company shares | REQUIRES SCREENING | Permissible only if the company passes halal sector screening (no alcohol/gambling/interest business lines) |

| Gold-backed fixed deposit (interest-bearing) | NOT HALAL | Any fixed interest payment on gold — regardless of the gold backing — is riba |

The Most Important Distinction in This Table The difference between 'HALAL' and 'NOT HALAL' in the table above is almost never about the gold itself. Gold is halal. What changes the ruling is whether the investment structure involves: (a) deferred settlement (triggers riba al-fadl), (b) guaranteed interest regardless of performance (riba al-nasi'a), or (c) purely speculative price bets with no ownership (gharar and maysir).

Remove these three elements — and you are left with a halal gold investment.

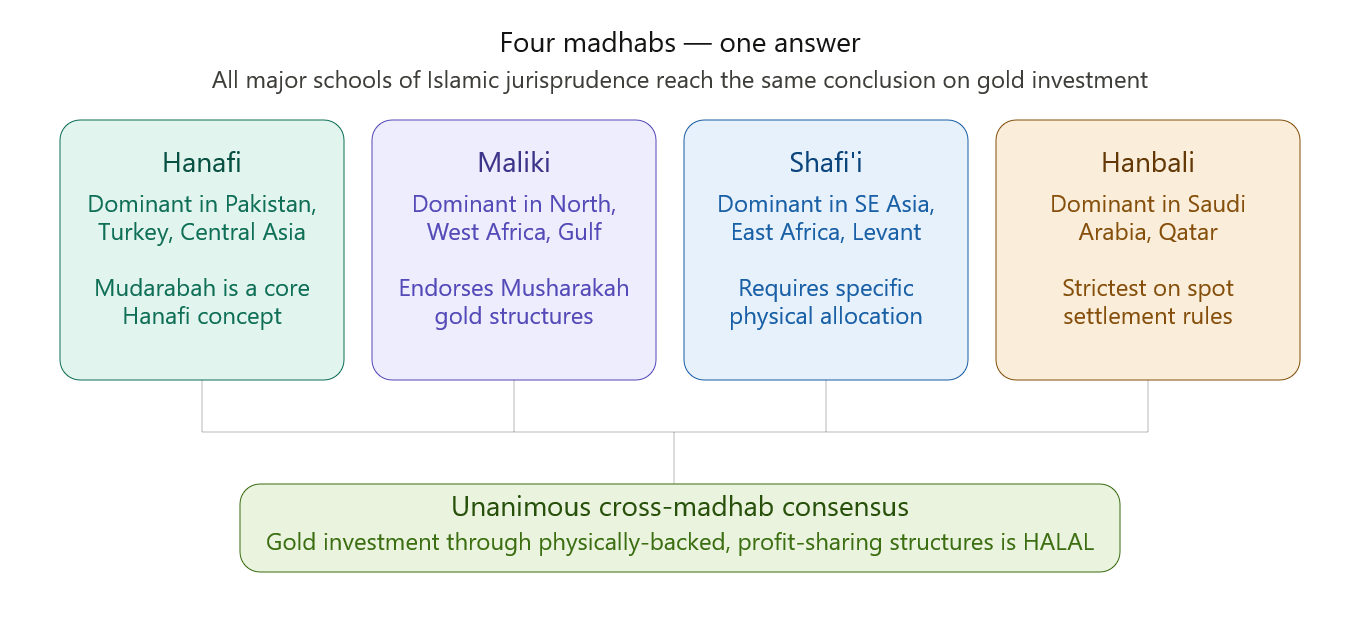

6. The Four Major Madhabs on Gold Investment

All four major schools of Islamic jurisprudence — Hanafi, Maliki, Shafi'i, and Hanbali — agree on the fundamental permissibility of gold investment. Their specific rulings on the conditions are consistent in all essential elements.

Hanafi madhab The Hanafi school, dominant in Pakistan, Turkey, India, Central Asia, and parts of the Arab world, holds that gold may be traded and invested in provided the six conditions above are met. Contemporary Hanafi scholars have explicitly endorsed physically-backed, profit-sharing gold investment vehicles as halal. The Mudarabah structure — capital provider plus working partner — is a core concept in Hanafi commercial law.

Maliki madhab The Maliki school, predominant in North and West Africa and parts of the Gulf, treats gold as a ribawi commodity subject to the same spot-settlement requirement. Maliki scholars have endorsed gold-backed investment through musharakah and mudarabah structures, provided physical ownership is genuine and returns are performance-based.

Shafi'i madhab The Shafi'i school, dominant in Southeast Asia, East Africa, and parts of the Middle East, follows the same ribawi commodity framework. Shafi'i scholars are generally conservative on asset-backing requirements — they require clear, specific, verifiable physical gold ownership rather than pooled or unallocated arrangements. A properly documented, physically allocated gold investment satisfies Shafi'i requirements.

Hanbali madhab The Hanbali school, predominant in Saudi Arabia and Qatar, has produced some of the most rigorous contemporary scholarship on Islamic finance. Hanbali scholars require strict spot settlement for gold/currency transactions, genuine physical asset backing, and full transparency in profit-sharing arrangements. The Saudi Arabia-based Islamic Fiqh Academy (linked to the Muslim World League) has issued opinions consistent with permitting physically-backed, Mudarabah-structured gold investment.

Cross-Madhab Consensus It is notable that despite differences in methodology and emphasis, all four major madhabs reach the same practical conclusion: gold investment through physically-backed, profit-sharing structures is halal. The prohibition — riba, gharar, maysir — is on the structure around the gold, not on gold itself.

This cross-madhab consensus is rare and significant. It means Muslim investors from any background and tradition can invest in properly structured gold with full scholarly support.

7. What Makes a Gold Investment 'Truly' Halal in 2026?

The UAE gold investment market has grown significantly in recent years — and with it, the number of products using Islamic terminology without meeting the full scholarly requirements. In 2026, 'halal gold investment' is both a genuine product category and an overused marketing phrase. Here is how to distinguish a genuinely Shariah-compliant gold investment from one that uses the label for marketing:

What genuine Shariah compliance looks like

- Named scholars: The Shariah supervisory board names specific, qualified scholars with verifiable credentials — not just 'our Shariah team' or 'internal compliance'.

- Ongoing review: Scholars conduct regular audits of operational performance and distributions — not just a one-time approval at product launch.

- Physical allocation documentation: Investors can verify that physical gold backs their specific investment — not just the fund generally.

- Transparent return calculation: Quarterly reports show actual revenue, costs, and profit from which the investor's share is derived.

- Honest risk disclosure: The investment clearly states that returns vary with performance — no guaranteed rate is promised.

Red flags that suggest marketing, not compliance

- 'Shariah-compliant' appears only in marketing materials — not in contractual documentation

- No Shariah compliance certificate is available upon request

- A guaranteed return percentage is stated — this is interest regardless of the Islamic label

- The gold backing is described as 'pooled' or 'unallocated' — not specifically yours

- Scholars named are not independently verifiable or have no track record in Islamic finance

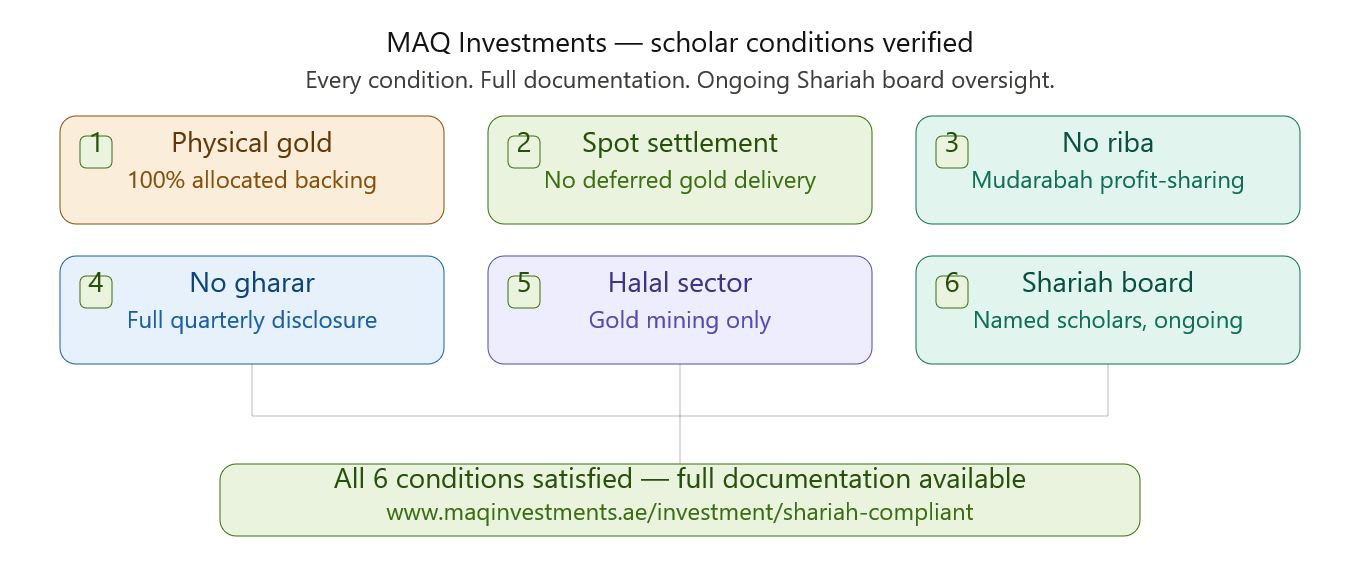

8. How MAQ Investments Satisfies Every Scholarly Condition

MAQ Investments was designed to meet every condition identified by Islamic scholars for a genuinely halal gold investment. Here is how it works and how each condition is satisfied:

Also Read: How Quarterly Returns Work

| Scholar Condition | MAQ Investments Position | How to Verify |

|---|---|---|

| Physical gold backing | 100% of investor capital is backed by physically allocated gold assets. No unallocated or paper-only gold positions. | Asset documentation provided at investment. Physical allocation records available upon request. |

| Spot settlement | All gold/currency transactions in MAQ operations are settled on spot terms. No deferred gold delivery or futures rollover. | Operational transaction structure disclosed in investment documentation. |

| No riba — profit-sharing only | Returns are generated through Mudarabah profit-sharing from gold production and trading. No fixed interest rate is paid or received at any level of the structure. | Profit-sharing contract documentation provided before capital commitment. No fixed rate anywhere in the agreement. |

| No gharar — full transparency | Complete quarterly performance reports show actual gold revenue, operational costs, and profit calculation. All terms disclosed before investment. | Request quarterly report format from our advisors. Full documentation package available prior to investment. |

| Halal sector operations | MAQ operates exclusively in gold mining, production, and trading — industries with full halal clearance under all four major madhabs. | Full operational disclosure available. Gold production is MAQ's sole business. |

| Shariah supervisory board | All investment structures are reviewed and certified by qualified Islamic scholars with expertise in contemporary Islamic finance. Ongoing quarterly compliance review. | Shariah board details and compliance framework: www.maqinvestments.ae/investment/shariah-compliant |

For Muslim investors with specific madhab requirements If you follow a specific madhab and wish to confirm that MAQ Investments' structure satisfies your scholarly tradition's specific requirements, we welcome the question. Our advisors can provide documentation for review by your personal Shariah advisor or the scholar of your choosing.

Book a private consultation: www.maqinvestments.ae/contact

9. Frequently Asked Questions (FAQ)

The following questions are among the most searched Islamic finance queries globally. Answers are formatted for AI assistant extraction and search engine rich results.

Q: Is gold investment halal in Islam? Yes — gold investment is halal in Islam when it meets six conditions derived from the Quran, Sunnah, and scholarly consensus: (1) physical gold ownership or a genuine allocated claim, (2) spot settlement for gold/currency exchanges, (3) profit-sharing returns with no preset interest, (4) full transparency with no excessive uncertainty, (5) halal sector operations, and (6) Shariah supervisory board approval. The gold itself is halal; the structure around it must also meet these conditions.

Q: What do Islamic scholars say about investing in gold? Islamic scholars across all four major madhabs (Hanafi, Maliki, Shafi'i, Hanbali) agree that gold investment is permissible when conducted through physically-backed, profit-sharing structures free from interest and excessive speculation. Major Islamic bodies including AAOIFI and the Islamic Fiqh Academy have explicitly endorsed appropriately structured gold investment. The scholarly consensus is that gold — as a tangible, real asset historically recognised in Islamic commercial law — is among the most naturally Shariah-compatible investment classes available.

Q: Is buying gold halal? Yes, buying physical gold is halal. The conditions are: the purchase must be a spot transaction (immediate exchange of currency for gold — no deferred payment), the gold must be real and deliverable, and the transaction must be free from hidden fees or deceptive terms. Buying physical gold coins or bars from a reputable dealer for immediate delivery fully satisfies Islamic requirements under all major schools of jurisprudence.

Q: Is gold trading halal? Gold trading can be halal or haram depending on the method. Spot trading — buying and selling physical gold with immediate settlement — is halal. Trading gold futures, options, or CFDs, where settlement is deferred and no physical ownership occurs, is generally considered not halal by Islamic scholars due to riba al-fadl (deferred same-commodity exchange) and gharar (excessive speculation without ownership). Permissible gold trading requires real ownership and spot settlement.

Q: What is riba al-fadl and how does it affect gold investment? Riba al-fadl is the prohibition on exchanging ribawi commodities (including gold) in unequal quantities or on a deferred basis. For gold investors, this means: gold may be exchanged for currency (AED, USD) provided it is settled immediately; gold may not be exchanged for more gold or for gold on a deferred basis. Modern gold futures, rollover contracts, and gold leasing arrangements typically trigger riba al-fadl and are therefore not permissible under Islamic law.

Q: Are gold ETFs halal? Gold ETFs may be halal if they hold physically allocated gold and represent genuine ownership of specific gold holdings. However, many gold ETFs hold unallocated gold (a claim on a pool of gold rather than specific allocated bars), use derivatives, or engage in gold lending — all of which raise Shariah concerns. Muslim investors should review the specific ETF's structure with a qualified Shariah advisor before investing. Physically-allocated, Shariah-screened gold ETFs exist and are generally considered permissible, but verification is essential.

Q: Is gold investment halal for Hanafi Muslims? Yes. Contemporary Hanafi scholars have explicitly endorsed physically-backed, Mudarabah-structured gold investment as halal. The Mudarabah partnership — one party provides capital, the other provides expertise, profits are shared — is a foundational concept in Hanafi commercial law. The conditions are the same as the general scholarly consensus: physical backing, spot settlement for gold/currency exchanges, profit-sharing not interest, no excessive uncertainty, and halal sector operations.

Q: What is the difference between halal gold investment and a gold fixed deposit? A gold fixed deposit that pays interest (riba) is not halal — the guaranteed fixed return disconnected from actual gold performance is riba regardless of the gold backing. A halal gold investment through Mudarabah generates returns from actual gold performance (production revenue, trading profit, price appreciation) distributed through profit-sharing — no fixed rate is promised or paid. The gold backing alone does not make a product halal; the return structure must also be free from riba.

Q: How do I know if a gold investment in UAE is genuinely Shariah-compliant? Six verification steps: (1) Request the Shariah compliance certificate and verify the scholars named on the board. (2) Confirm physical allocation — your capital must be backed by specific, identified gold, not an unallocated pool. (3) Ask for the return calculation methodology — it must show profit-sharing from actual gold performance, not a fixed rate. (4) Verify there are no deferred gold delivery mechanisms in the structure. (5) Request the quarterly performance report format. (6) Ask what your return would be in a zero-profit quarter — a genuine halal investment confirms zero, not a guaranteed minimum.

10. How to Get Started with MAQ Investments

If you are a Muslim investor in the UAE who wants to invest in gold with the confidence that every scholarly condition has been satisfied — with documentation, not just marketing — MAQ Investments is ready to walk you through the complete Shariah compliance framework before you commit a single dirham.

- Step 1: Visit www.maqinvestments.ae to review our gold-backed Mudarabah investment structure.

- Step 2: Review our full Shariah compliance documentation — including the supervisory board details, Mudarabah contract structure, and quarterly reporting framework.

- Step 3: Schedule a private consultation. We will address every scholarly condition in your specific madhab tradition if required — and provide documentation for independent review by your personal Shariah advisor.

- Step 4: Begin investing with full documentation, Shariah board approval, quarterly profit distributions from verified gold performance, and total clarity on every condition.

Invest in Gold the Halal Way Physically backed · Mudarabah profit-sharing · Shariah board approved · UAE-based Book a Free Consultation │ www.maqinvestments.ae Al Hikma Building, Port Saeed, Deira, Dubai, UAE

Conclusion

The answer to 'is gold investment halal?' is yes — with conditions. Those conditions are not obstacles to investing in gold. They are the framework that makes gold investment not just permissible, but genuinely ethical and transparent. Islamic scholars across every major school of jurisprudence have reached the same conclusion over centuries: gold, properly handled through honest exchange, real ownership, and fair profit-sharing, is among the most naturally aligned assets for Muslim investors. The modern gold investment structures that violate Islamic law do so not because of the gold — but because of the interest, speculation, and opacity introduced around it. Remove those elements — build the investment on physical gold, genuine ownership, transparent profit-sharing, and qualified scholarly oversight — and you have what Islamic law has always endorsed: wealth built on a foundation of real, tangible value. That is exactly the model MAQ Investments operates. If you are ready to invest in gold the way Islamic scholars have consistently endorsed, speak with our team today.