Wealth Preservation vs. Wealth Creation: Which Should Guide Your 2026 Strategy?

A Framework for UAE Investors Deciding Where to Focus

Every serious investor eventually confronts a version of the same question: am I trying to protect what I have, or am I trying to grow it? The two goals sound complementary, but in practice they pull a portfolio in different directions — different assets, different risk tolerances, different time horizons, and often different emotional postures toward market movements.

In the UAE in 2026, this question has acquired new urgency. The AED's peg to a US dollar that lost roughly 10% of its value in 2025 means that simply holding cash has been a preservation failure for many residents — without a single headline-grabbing crash. At the same time, bank deposit rates have fallen to 2.55%–4.75%, meaning that 'safe' parking spots are no longer doing the creation job either.

Investors who assumed they were doing one or the other have often, without realising it, been doing neither.

This article lays out the distinction clearly, helps you identify which objective your current situation actually calls for, and explains why — for a growing number of UAE investors — the answer in 2026 is not a choice between the two but a structure that delivers both simultaneously.

Table of Contents

- 1. What is Wealth Preservation?

- 2. What is Wealth Creation?

- 3. Preservation vs Creation — The Complete Comparison

- 4. The 2026 Problem: Why 'Safe' No Longer Means Either

- 5. Which Objective Fits Your Life Stage?

- 6. The False Choice — Why You Don't Have to Pick One

- 7. How Gold-Backed Mudarabah Investment Does Both

- 8. Building Your 2026 Strategy — A Practical Framework

- 9. Frequently Asked Questions (FAQ)

- 10. How to Get Started

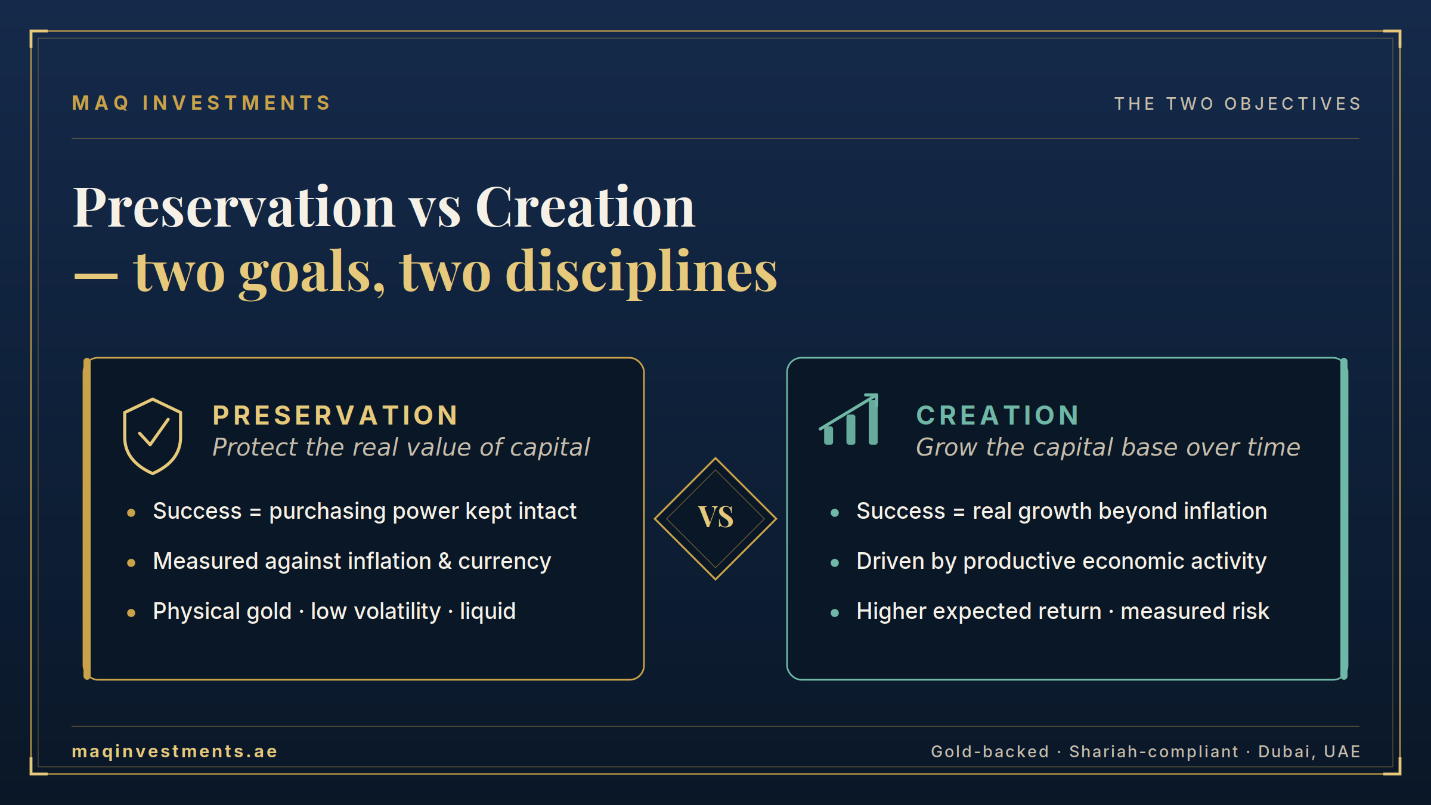

1. What is Wealth Preservation?

Wealth preservation is the practice of protecting the real value of capital you already have. The benchmark is not 'did this investment go up?' but 'did my purchasing power stay the same or better?' A preservation-focused investor measures success against inflation, currency movements, and the risk of permanent loss — not against a growth index.

Preservation-oriented assets share common traits: they tend to be less volatile, more liquid in a crisis, and historically resilient across economic cycles. Physical gold is the most universally recognised preservation asset — it has no counterparty risk, cannot be defaulted on, and has maintained purchasing power across centuries of currency regimes.

Core question: Will this still be worth roughly the same, in real terms, in 10 years?

Common instruments: Physical gold, diversified hard assets, low-volatility holdings, strategic cash reserves

Who needs it most: Investors near a known capital need, those with large existing wealth to protect, and anyone uneasy about currency and inflation risk

2. What is Wealth Creation?

Wealth creation is the practice of growing capital meaningfully over time — building a larger base than you started with, in real terms, not just nominal terms. The benchmark here is growth relative to inflation and relative to opportunity cost: could this capital have done more elsewhere?

Creation-oriented assets accept measured volatility in exchange for higher expected return. This typically means exposure to productive economic activity — businesses, production, trade — where returns are generated by genuine value creation rather than simply holding an asset steady.

Core question: Will this meaningfully grow my capital base over the next 5–10 years?

Common instruments: Equities, growth-oriented funds, profit-sharing ventures (including Mudarabah structures Mudarabah structures), productive real assets

Who needs it most: Investors with a longer horizon, those building toward a future goal (retirement, education, a major purchase), and anyone whose current capital base is not yet sufficient for their goals

The Trap of Treating Them as Opposites

Many investors implicitly believe preservation and creation are mutually exclusive — that protecting capital means accepting near-zero growth, and that pursuing growth means accepting real risk to the principal.

This belief made more sense in an environment of higher interest rates, where a 'safe' bank deposit could at least keep pace with modest inflation. In 2026, with UAE deposit rates declining toward 2.55%–4.75% and inflation plus currency erosion running higher than that, the 'safe' option is failing the preservation test too — while still failing the creation test outright.

3. Preservation vs Creation — The Complete Comparison

The following table lays out the two objectives side by side across the dimensions that matter for a 2026 UAE investor — including where a gold-backed Mudarabah structure sits relative to each.

| Dimension | Wealth Preservation | Wealth Creation | Gold-Backed Mudarabah |

|---|---|---|---|

| Primary objective | Protect existing capital from erosion — inflation, currency weakness, market shocks | Grow capital meaningfully over time — outpace inflation by a wide margin | Both: 100% physical gold backing + 16%–24% target returns |

| Time horizon | Often shorter or capital is near a known need (retirement, large purchase, succession) | Longer horizon — 5+ years where compounding and growth can work | Flexible: structured for both near-term preservation and mid-term growth |

| Typical instruments | Physical gold, low-volatility assets, diversified hard-asset holdings, cash reserves | Equities, growth funds, profit-sharing ventures, productive real assets | Physical gold + Mudarabah profit-sharing operations |

| Risk posture | Minimise downside — accept lower upside in exchange for stability | Accept measured volatility in exchange for higher expected return | Downside protection (gold backing) + upside generation (operational returns) |

| Success measured by | Did my real purchasing power stay intact? | Did my capital base grow in real terms? | Did I protect capital AND generate meaningful growth? |

| 2026 UAE relevance | AED pegged to USD; 2025 dollar weakness (~10%) eroded real value of cash holdings silently | UAE FD rates falling to 2.55%–4.75%; passive holdings no longer keep pace with goals | Addresses both problems simultaneously |

| Where gold-backed Mudarabah fits | 100% physical gold backing = preservation layer built into the structure | 16%–24% target return from quarterly profit-sharing = creation layer built into the same structure | Single allocation serving both functions |

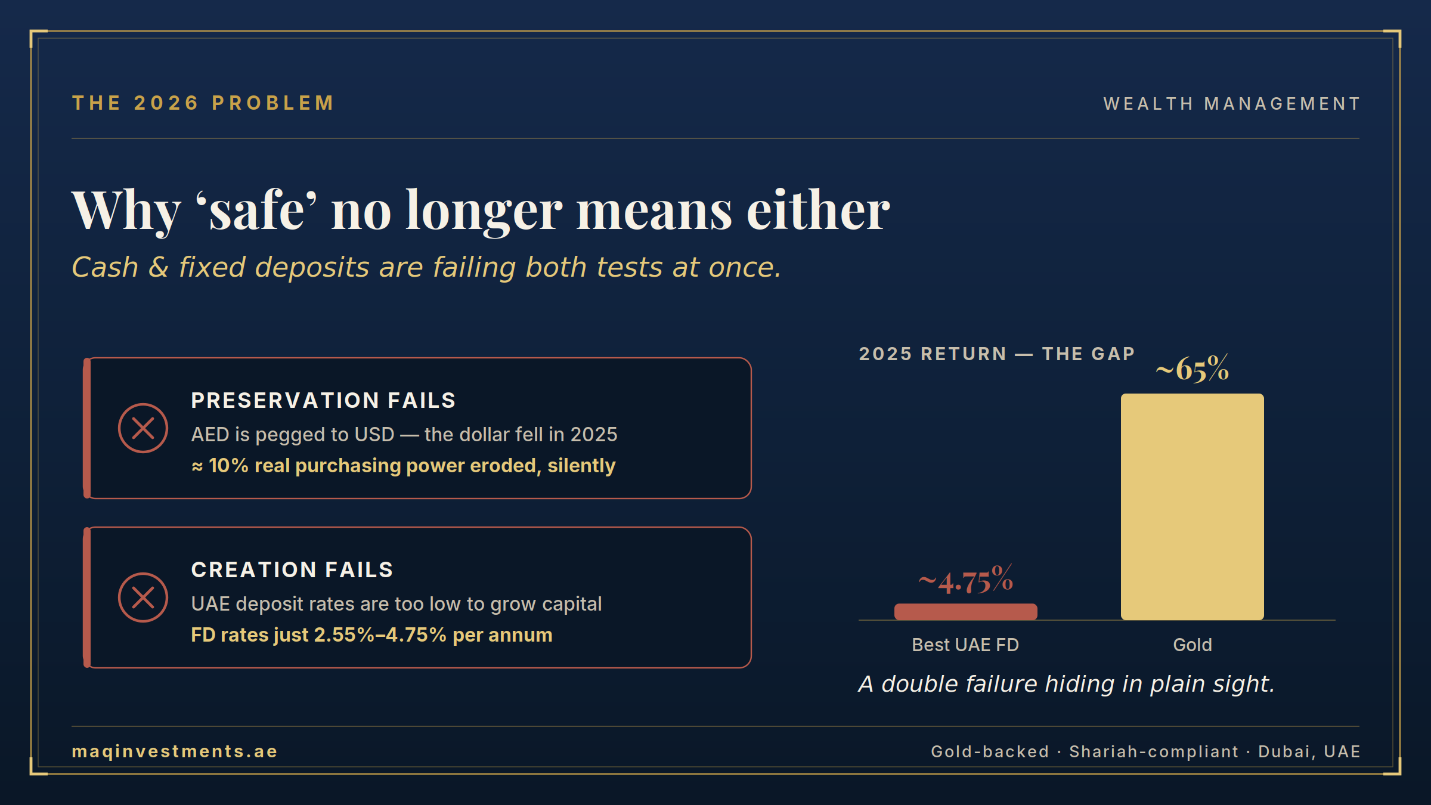

4. The 2026 Problem: Why 'Safe' No Longer Means Either

For UAE investors, 2025–2026 exposed a structural problem that had been quietly building for years: the instruments traditionally treated as 'safe' — cash savings and bank fixed deposits — have stopped reliably serving either the preservation or the creation function.

The Preservation Failure

The AED is pegged to the US dollar. When the dollar weakened by approximately 10% in 2025, every AED-denominated cash holding lost a corresponding amount of real global purchasing power — invisibly, with no market crash, no red headline, and no bank statement reflecting the loss. An investor holding AED 1,000,000 in savings did not see the number change. But what that number could buy, in real terms, shrank.

The Creation Failure

Simultaneously, UAE bank fixed deposit rates have been declining as the UAE Central Bank follows the US Federal Reserve's rate cuts. The best available rates in May 2026 sit at 2.55%–4.75% per annum. Even before accounting for currency erosion, these rates are barely keeping pace with — or falling behind — broader cost-of-living increases. Capital sitting in these instruments is not meaningfully growing.

The Result: A Double Failure Hiding in Plain Sight

An investor who believed they were 'playing it safe' by holding cash and fixed deposits has, without any dramatic event, experienced both a preservation failure (real purchasing power eroded by currency weakness) and a creation failure (nominal growth too slow to matter).

This is precisely the environment in which both 2025 gold returns (approximately 65%) and a renewed interest in asset-backed, profit-sharing investment structures have accelerated across the UAE.

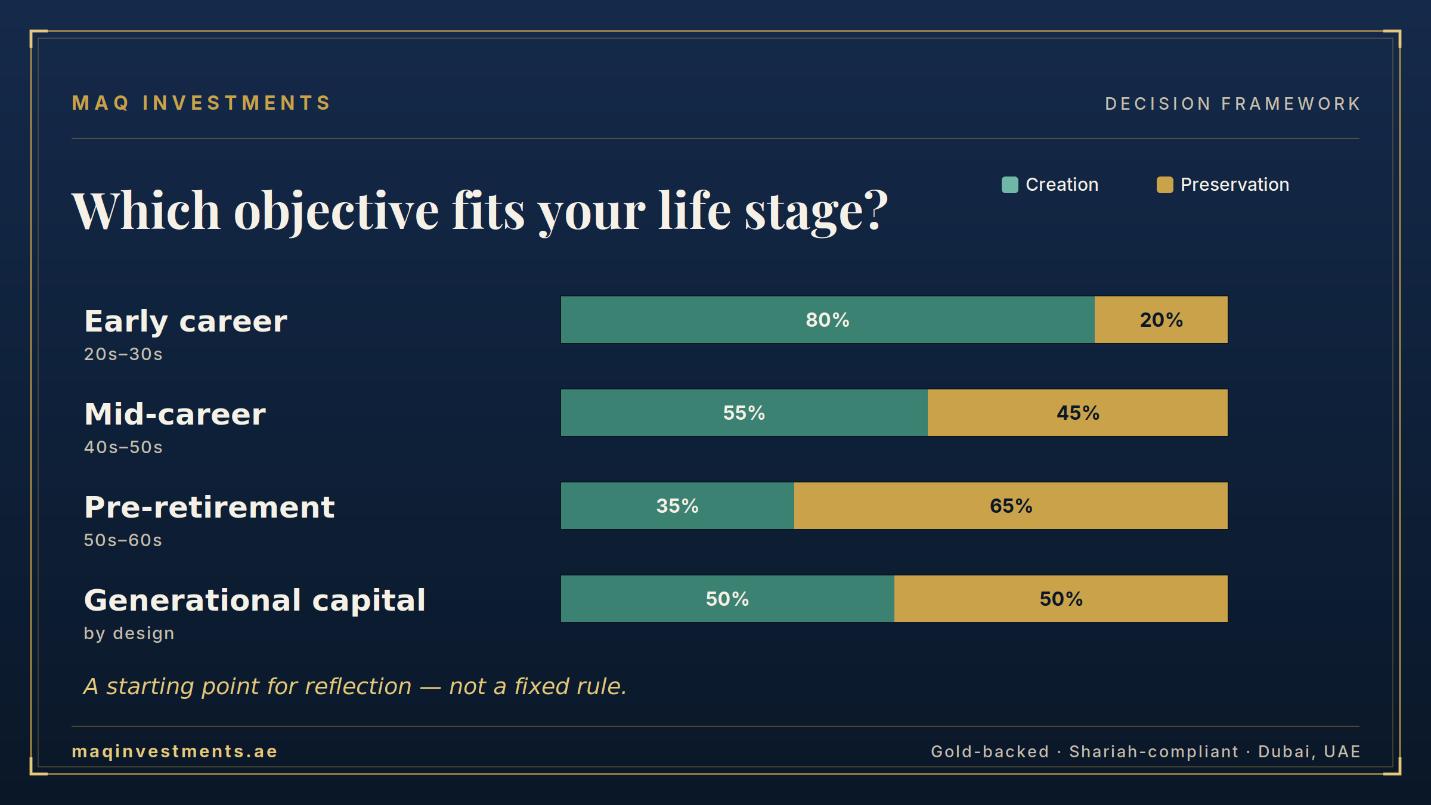

5. Which Objective Fits Your Life Stage?

The right balance between preservation and creation is not fixed — it shifts with your life stage, your existing capital base, and how close you are to needing that capital for a specific purpose. The table below offers a general framework, not a rigid formula:

| Life Stage | Primary Need | Typical Mix | Why |

|---|---|---|---|

| Early career / wealth building (20s–30s) | Mostly creation | 70–90% creation-oriented, 10–30% preservation | Long horizon absorbs volatility; compounding has decades to work |

| Mid-career / peak earnings (40s–50s) | Balanced | 50/50 to 60/40 creation-to-preservation | Capital base is larger — protecting it matters as much as growing it |

| Pre-retirement / wealth transfer (50s–60s) | Mostly preservation, selective creation | 30–40% creation, 60–70% preservation | Capital must support the next phase — large losses are hard to recover from |

| Generational / family office capital | Both, simultaneously, by design | Structured allocation across both objectives, often in the same vehicle | Different family members and goals require both functions running in parallel |

This is a Starting Point, Not a Rule

These ranges describe tendencies, not requirements. A 30-year-old who has already built substantial capital may prioritise preservation earlier. A 60-year-old starting a new venture with capital they can afford to risk may prioritise creation later than the table suggests.

The framework's value is in prompting the right question — 'given where I am, which of these two functions does my portfolio most need right now?' — rather than dictating a specific percentage split.

6. The False Choice — Why You Don't Have to Pick One

The preservation-versus-creation framing implies a trade-off: more of one means less of the other. This is true for many individual instruments — a bank fixed deposit cannot also deliver meaningful growth; a high-growth equity position cannot also guarantee stability of principal.

But it is not true of every instrument. Some asset structures are specifically designed to deliver both functions simultaneously — not by averaging a 'safe' asset with a 'risky' one, but by combining a preservation-grade asset base with a creation-grade return mechanism in a single structure.

What such a structure requires

-

A preservation-grade underlying asset: Something with the resilience profile of gold or another hard asset — not paper claims, not interest-bearing debt instruments whose value depends entirely on a counterparty's solvency.

-

A creation-grade return mechanism: A genuine profit-generating activity layered on top of that asset — production, trading, or operations that create real economic value, with returns distributed to capital providers.

-

Alignment between the two: The return mechanism should not undermine the preservation function. If generating returns required leveraging or risking the underlying asset itself, the structure would simply be creation dressed up as preservation.

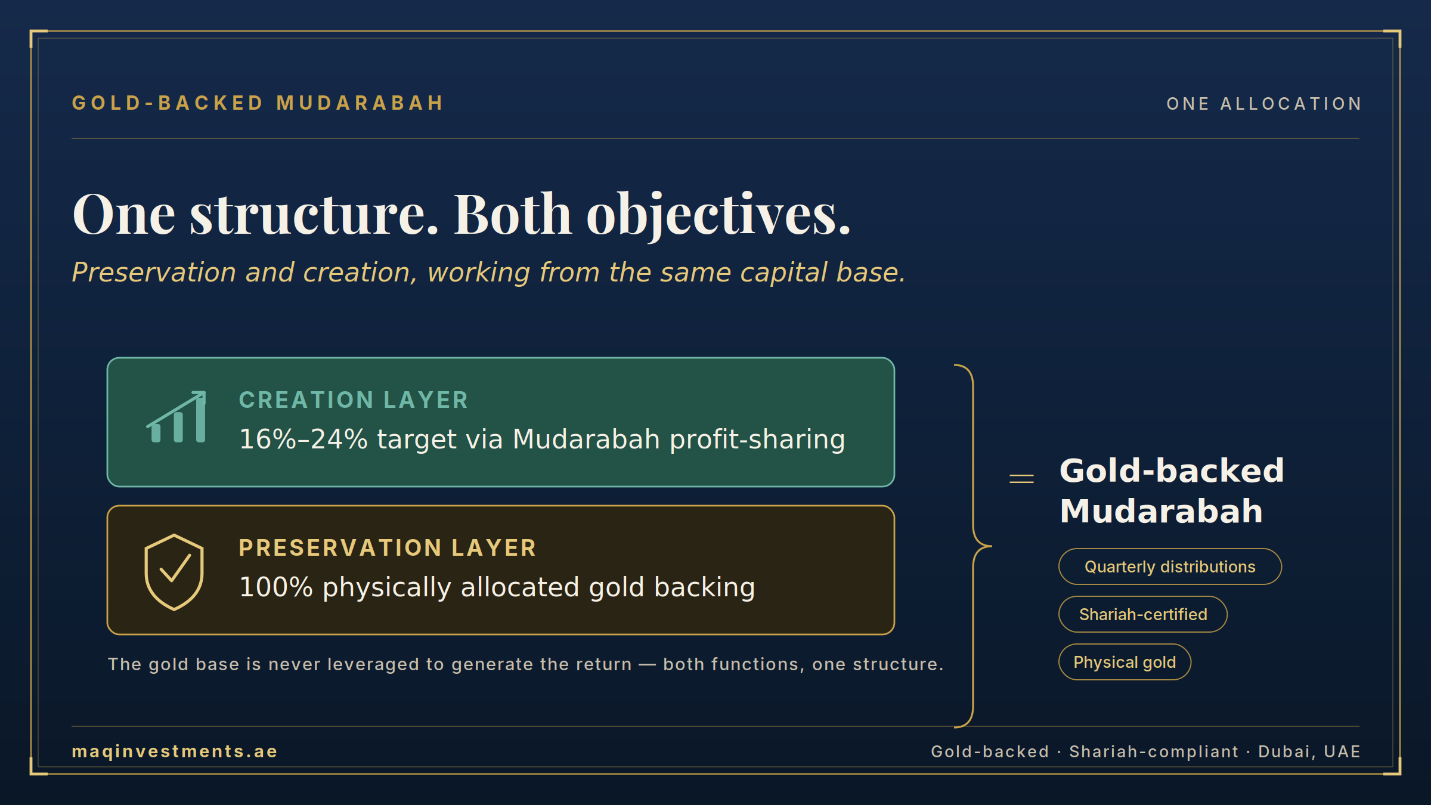

7. How Gold-Backed Mudarabah Investment Does Both

A gold-backed Mudarabah investment is a practical example of a structure designed to satisfy both functions at once — and understanding why illustrates the broader principle.

The Preservation Layer: Physical Gold Backing

In a structure such as MAQ Investments' model, investor capital is allocated to 100% physically held gold — specific, identified, custodied assets, not a paper claim or a balance-sheet promise. Gold has the preservation characteristics that matter: it is not denominated in a currency that can be devalued by policy decisions, it has no counterparty that can default, and it has historically tracked or outpaced inflation over long periods. This is the same asset class that delivered approximately 65% returns in 2025 precisely because of the currency and inflation pressures described in Section 4.

The Creation Layer: Mudarabah Profit-Sharing

Layered on top of that physical gold base is a Mudarabah structure — a partnership in which the capital provider (the investor) and the manager (MAQ Investments) share in the profit generated from gold production and trading operations. This is where the creation function comes from: actual quarterly profit, generated by actual gold market activity, targeting 16%–24% annually and distributed at 4%–6% per quarter.

Crucially, this return mechanism does not undermine the preservation function. The gold backing the investment is not leveraged, pledged, or put at risk to generate the Mudarabah return — the return comes from production and trading activity around the gold, while the underlying physical asset remains the capital base.

Why This Matters for the Preservation-vs-Creation Question

An investor who allocates capital to this kind of structure is not choosing between protecting their wealth and growing it. They are doing both, through a single allocation: the gold component anchors the preservation function (a hedge against the same AED/USD and inflation dynamics described in Section 4), while the Mudarabah profit-sharing component drives the creation function (a target return that significantly exceeds the 2.55%–4.75% available from conventional 'safe' instruments).

This is also why such a structure is described as Shariah-compliant: the return comes from genuine profit-sharing on real economic activity (no riba), backed by a tangible asset (no pure speculation), with full transparency on how returns are calculated each quarter ( gharar ).

8. Building Your 2026 Strategy — A Practical Framework

Use the following sequence to think through your own preservation-versus-creation balance for 2026:

Step 1 — Audit your current allocation honestly How much of your capital is in cash or AED fixed deposits? Calculate what that capital has actually done in real terms over the past 12–24 months, accounting for currency movements and inflation — not just the nominal interest received.

Step 2 — Identify your dominant need Using the life-stage framework in Section 5, identify whether your situation currently calls more for preservation, creation, or — as is increasingly common — both at once.

Step 3 — Separate 'safe' from 'effective' An instrument can feel safe (familiar, low-volatility, government-backed) while being ineffective at either preservation or creation in the current rate and currency environment. Evaluate instruments on what they actually deliver, not on how familiar they feel.

Step 4 — Look for structures that combine both functions Rather than splitting capital between a 'preservation bucket' and a 'creation bucket' that may both be underperforming, consider whether a single structure — such as a physically-backed, profit-sharing investment — can serve both functions with one allocation.

Step 5 — Revisit annually, not reactively Your preservation-versus-creation balance should shift as your life stage and capital base change — on a planned annual review, not in response to short-term market noise.

9. Frequently Asked Questions (FAQ)

These questions reflect common search queries from UAE investors thinking through their 2026 strategy.

Q: What is the difference between wealth preservation and wealth creation?

Wealth preservation focuses on protecting the real value of existing capital — measured by whether purchasing power is maintained against inflation and currency movements. Wealth creation focuses on growing capital meaningfully over time — measured by real growth relative to inflation and opportunity cost. Preservation typically favours lower-volatility, hard-asset holdings such as physical gold; creation typically favours productive, profit-generating allocations such as equities or profit-sharing investments. Both are legitimate goals, and the right balance depends on an investor's time horizon, existing capital base, and life stage.

Q: Should I focus on wealth preservation or wealth creation in 2026?

For most UAE investors in 2026, the honest answer is both — because conventional 'safe' instruments are currently failing at each function individually. AED-denominated cash and bank deposits have been eroded in real terms by 2025 dollar weakness (approximately 10%), while UAE fixed deposit rates of 2.55%–4.75% are too low to meaningfully grow capital. Investors should assess their life stage using a framework (younger investors lean toward creation, those near a capital need lean toward preservation, and those in between often need a balance) and consider structures that can deliver both functions through a single allocation, such as physically-backed, profit-sharing investments.

Q: Can an investment provide both wealth preservation and wealth creation?

Yes, if it combines a preservation-grade underlying asset with a creation-grade return mechanism without one undermining the other. A gold-backed Mudarabah investment is one example: physical gold provides the preservation function (resilience against currency and inflation pressures), while Mudarabah profit-sharing from gold production and trading operations provides the creation function (target returns of 16%–24% annually). The key is that the return mechanism does not require leveraging or risking the underlying preservation asset — both functions operate from the same capital base without conflict.

Q: Why are bank fixed deposits no longer enough for wealth preservation in UAE?

The AED is pegged to the US dollar. When the dollar weakens — as it did by approximately 10% in 2025 — AED-denominated holdings, including fixed deposits, lose a corresponding amount of real global purchasing power, even though the nominal balance and interest payments remain unchanged. At the same time, UAE fixed deposit rates have declined to 2.55%–4.75% as the UAE Central Bank follows US Federal Reserve rate cuts. When currency erosion and inflation exceed the interest earned, a fixed deposit fails the preservation test — the investor's real purchasing power has declined despite the account balance growing.

Q: How much of my portfolio should be allocated to wealth preservation vs wealth creation?

There is no universal percentage, but a general framework based on life stage is useful: early-career investors with long horizons often allocate 70–90% toward creation-oriented assets; mid-career investors with larger capital bases often move toward a 50/50 to 60/40 split; pre-retirement investors often shift to 60–70% preservation; and family or generational capital often runs both objectives simultaneously through structured allocations. These are starting points for reflection, not rules — the right split depends on individual circumstances, existing capital, and proximity to specific financial goals.

Q: Is gold a wealth preservation or wealth creation asset?

Physical gold is traditionally classified as a wealth preservation asset — it has no counterparty risk, cannot be devalued by policy decisions, and has historically maintained purchasing power across long periods, including delivering approximately 65% returns in 2025 amid dollar weakness and inflation concerns. However, when physical gold is combined with a profit-sharing structure such as Mudarabah — where capital is deployed in gold production and trading operations generating quarterly distributions — the same underlying asset can also serve a wealth creation function, with target returns of 16%–24% annually layered on top of the preservation characteristics of the gold itself.

10. How to Get Started

Whether your 2026 priority is preservation, creation, or — as is increasingly the case for UAE investors — both at once, the starting point is the same: an honest assessment of what your current allocation is actually delivering, and a conversation about structures designed to do more.

Step 1: Visit www.maqinvestments.ae to review the gold-backed Mudarabah investment model and how it combines preservation and creation functions.

Step 2: Review the Shariah compliance framework to understand the physical gold allocation and Mudarabah profit-sharing structure in detail.

Step 3: Book a free private consultation. Our Dubai-based advisors will help you assess your current preservation-versus-creation balance and discuss whether this structure fits your situation.

One Structure, Both Objectives

100% physical gold backing for preservation · 16%–24% target returns for creation · Quarterly distributions · Shariah certified

Book a Free Consultation │ www.maqinvestments.ae

Al Hikma Building, Port Saeed, Deira, Dubai, UAE · Trade Licence No. 1173765

Conclusion

Preservation and creation are often presented as competing instincts — protect what you have, or risk it for growth. But in 2026, the more useful question for UAE investors is not which instinct to follow, but whether the instruments they currently rely on are actually serving either instinct at all.

For an investor holding AED cash or fixed deposits through 2025, the honest answer was likely neither — currency erosion quietly undermined preservation, while declining rates undermined creation. That double failure, occurring without any dramatic market event, is precisely why structures that combine a preservation-grade asset base with a creation-grade return mechanism have become a central conversation for serious UAE investors this year.

A gold-backed Mudarabah investment is one such structure — built to protect capital through physical gold while growing it through genuine, Shariah-compliant profit-sharing.Speak with our team to find out whether it fits the balance your 2026 strategy needs.

Questions? Contact MAQ Investments +971 55 648 0193 | www.maqinvestments.ae