You have probably seen the words "Shariah-compliant" on a bank brochure, an investment product, or a financial app. But how do you know if the claim is genuine, or just marketing language designed to attract Muslim investors?

The truth is, many products in the UAE use Islamic finance terminology loosely. A few pass the full test. Most do not.

This checklist is your practical tool to evaluate any investment, before you commit your capital. It covers the four non-negotiable criteria that every Shariah scholar, every Islamic finance regulator, and every genuine halal investment must satisfy.

By the end of this guide, you will know exactly what to look for, and how MAQ Investments measures up against each criterion.

Table of Contents

- 1. The Shariah-Compliant Investment Checklist, Quick Reference

- 2. Criterion 1: No Riba, The Prohibition of Interest

- 3. Criterion 2: Asset-Backed, Real Value, Not Paper Promises

- 4. Criterion 3: No Gharar, Clarity Over Uncertainty

- 5. Criterion 4: Halal Sector, Where Your Money Goes Matters

- 6. The Complete Criterion Breakdown (Detailed Table)

- 7. Red Flags: 8 Signs an Investment Is NOT Shariah-Compliant

- 8. How to Use This Checklist Before You Invest

- 9. How MAQ Investments Passes Every Criterion

- 10. Frequently Asked Questions (FAQ)

- 11. How to Get Started with MAQ Investments

1. The Shariah-Compliant Investment Checklist, Quick Reference

Before diving into each criterion in depth, here is the complete checklist at a glance. Use this as your first filter when evaluating any investment opportunity in the UAE:

| Criterion (Arabic Term) | The Question to Ask | Investment Must... |

|---|---|---|

| No Riba (ربا) | Does this investment pay or charge fixed interest in any form? | Generate returns through profit-sharing, never fixed interest |

| Asset-Backed (أصول حقيقية) | Is my capital secured by a tangible, real-world asset? | Be backed by physical assets (gold, property, commodities), not paper instruments |

| No Gharar (غرر) | Are the terms, risks, and return structure fully transparent and defined? | Have clearly disclosed terms, defined assets, and no hidden uncertainty |

| Halal Sector (قطاعات حلال) | Does the investment avoid industries prohibited under Islamic law? | Exclude alcohol, tobacco, weapons, gambling, adult content, and pork industries |

How to Use This Checklist For any investment you are considering, go through all four criteria. An investment that fails even ONE criterion is not Shariah-compliant, regardless of any label or certificate it carries. There are no partial marks in Islamic finance.

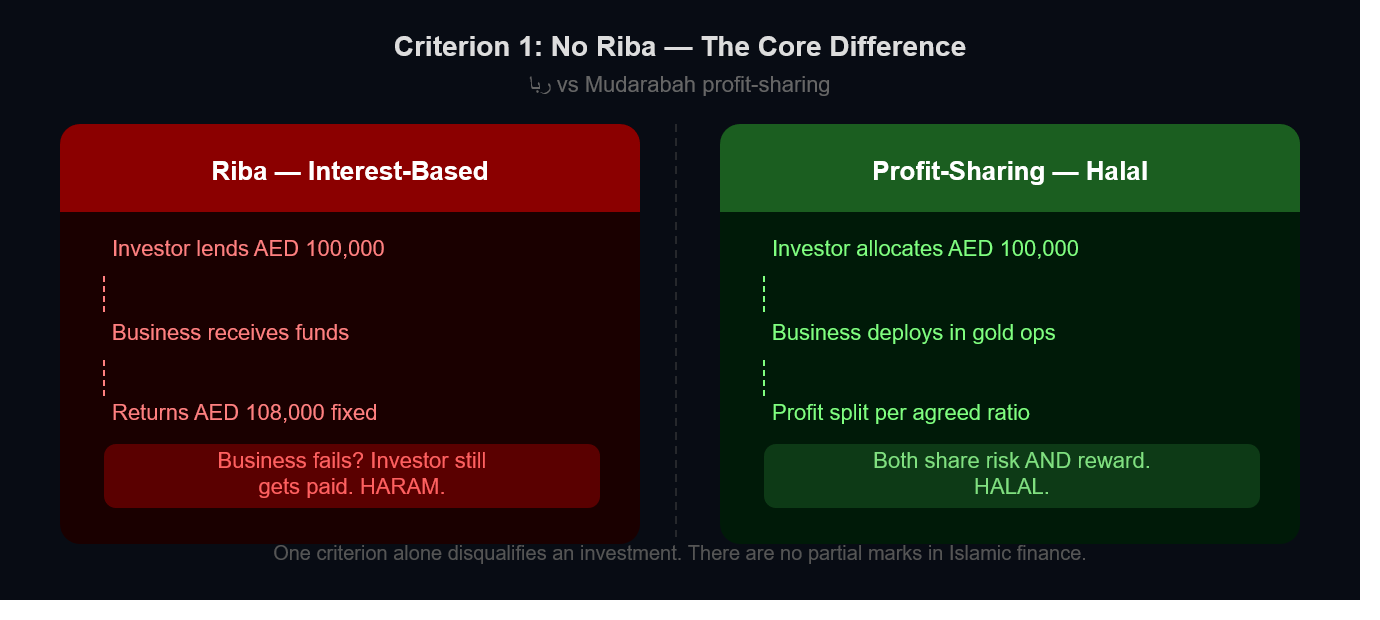

2. Criterion 1: No Riba, The Prohibition of Interest

Riba (ربا) is the Arabic term for interest or usury. It is the single most important prohibition in Islamic finance, and the one most commonly violated by financial products that claim Shariah compliance.

Also Read: What is Shariah-Compliant Investment?

What exactly is Riba? Riba means any guaranteed, pre-determined return on money lent or deposited, where the lender earns regardless of whether the underlying business succeeds or fails. This includes:

- Fixed-interest bank savings accounts and term deposits

- Bonds that pay a set coupon rate

- Loan products where interest accumulates on the principal

- Any financial structure where money itself 'earns money' without connection to a real asset or economic activity

Why is Riba prohibited? Islamic finance views interest-based transactions as fundamentally unjust. When a lender charges interest, they receive guaranteed profit regardless of outcomes, while the borrower bears all the risk. This creates an exploitative imbalance. Islam demands that both parties in a transaction share in risk and reward equally.

What is the halal alternative to interest? Shariah-compliant investments replace interest with profit-sharing structures. The two most common are:

- Mudarabah: A partnership where one party provides capital and the other provides expertise. Profits are split according to an agreed ratio. Losses are borne by the capital provider, while the manager loses their time and effort.

- Musharakah: A joint venture where both parties contribute capital and share profits and losses proportionally. Both parties are genuine partners in the enterprise.

Riba Checklist Question Ask directly: "Is the return on this investment generated through profit-sharing from a real business activity, or is it a fixed rate paid regardless of performance?" If the answer is a fixed rate, it is riba. It is not halal.

3. Criterion 2: Asset-Backed, Real Value, Not Paper Promises

The second pillar of Shariah-compliant investment UAE is that every investment must be tied to a tangible, real-world asset. Money cannot simply generate more money in isolation, there must be a real economic activity or a genuine physical asset at the foundation.

Also Read: Gold-Backed Investment vs. Fixed Deposits

What does 'asset-backed' mean in Islamic finance? An asset-backed investment means your capital is secured by ownership of, or a genuine claim on, a physical asset. Examples that qualify include:

- Physical gold, allocated and stored in a verified vault

- Real estate, direct ownership or a proportional share

- Commodities, physical inventory with verifiable ownership

- Operating businesses, where profit comes from actual production or trade

What does NOT qualify as asset-backed? Many modern financial products have no real asset backing whatsoever. These include:

- Most derivatives, options, futures, and swaps that are bets on price movements with no underlying ownership

- Certain ETFs and index funds, which may hold paper claims rather than physical assets

- Leveraged investment products, where the investment exceeds actual assets held

- Many cryptocurrency structures, where there is no underlying tangible asset

Why does asset-backing matter for Shariah compliance? Islamic finance requires that wealth creation be grounded in real economic activity. When your money is connected to a physical asset, like gold, it participates in the genuine economy rather than abstract financial engineering. This protects both investors and the broader financial system from the speculative cycles that cause economic crises.

Gold as the Ideal Asset-Backed Investment Gold is universally recognised by Islamic scholars as the most naturally Shariah-aligned asset. It is tangible, universally valued, non-perishable, and not subject to artificial manipulation the way paper assets are. When backed by physically allocated gold, an investment satisfies the asset-backing criterion completely. MAQ Investments backs 100% of investor capital with physical gold assets.

4. Criterion 3: No Gharar, Clarity Over Uncertainty

Gharar (غرر) refers to excessive uncertainty, ambiguity, or deception in a financial contract. Like riba, gharar is explicitly prohibited in Islamic law.

What constitutes Gharar? Gharar occurs when the terms of an investment are so unclear, complex, or uncertain that one party cannot make an informed decision. Gharar includes:

- Contracts where the asset being bought or sold does not exist yet at the time of agreement

- Highly complex derivative structures where the investor cannot understand or verify their actual exposure

- Investments with hidden fees, undisclosed conflicts of interest, or opaque performance reporting

- Speculation on future price movements without ownership of the underlying asset (short-selling, CFDs)

- Any financial product where the return depends entirely on chance, indistinguishable from gambling

What is the standard for acceptable transparency? A Shariah-compliant investment must clearly disclose:

- What asset your capital is invested in, specifically and verifiably

- How returns are generated, the actual business activity, not just a percentage promise

- What happens to your capital in a loss scenario, the risk must be honestly stated

- Who manages the investment and what oversight exists, including Shariah board details

- All fees, charges, and profit-sharing ratios, with no hidden deductions

The Gharar Test A simple test: could a reasonably informed investor read the investment documentation and clearly understand (a) what their money is invested in, (b) how their return is generated, and (c) what the realistic risks are? If the answer is no, if any of these three elements are vague, complex, or absent, the investment fails the gharar test.

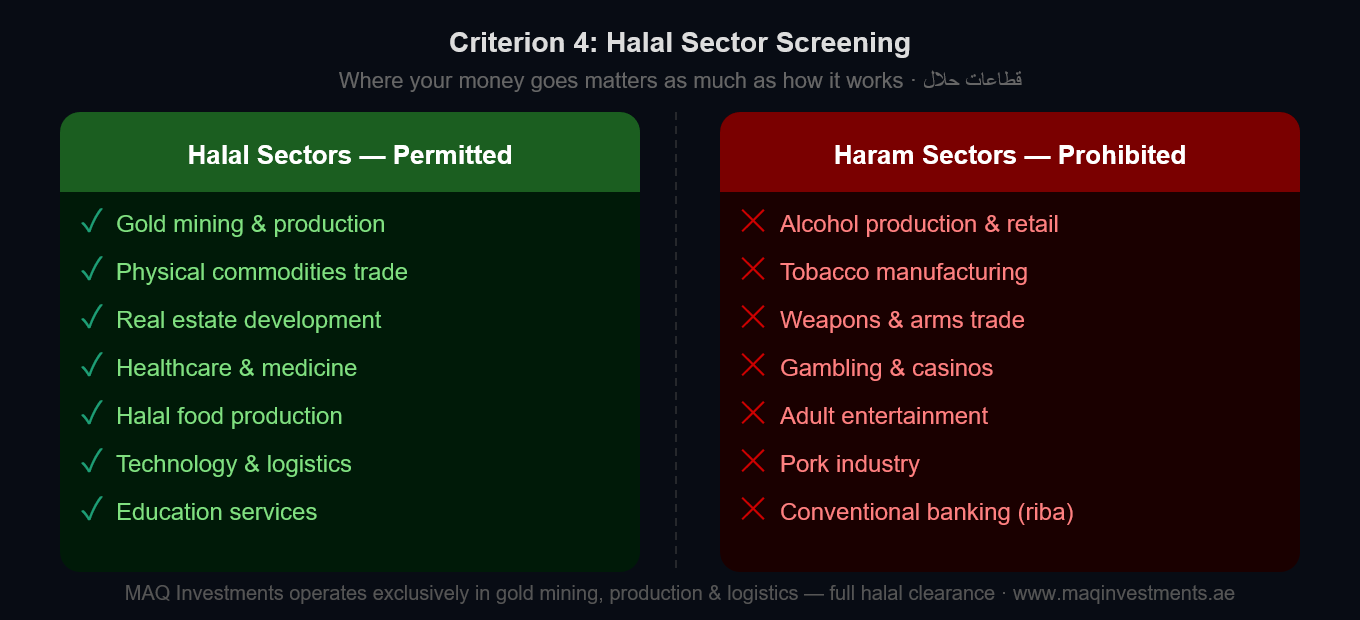

5. Criterion 4: Halal Sector, Where Your Money Goes Matters

Even if an investment has no riba, is asset-backed, and is fully transparent, it still fails Shariah compliance if the underlying business operates in a prohibited (haram) sector.

Islamic finance holds that wealth must be created through activities that are beneficial to society, not those that cause harm, addiction, or moral corruption. Where your money works matters as much as how it works.

Haram sectors, industries that disqualify an investment:

- Alcohol: production, distribution, retail, or any business deriving more than 5% of revenue from alcohol

- Tobacco: cigarette and tobacco product manufacturing or distribution

- Weapons and defence: arms manufacturing, weapons trading, military contractor companies

- Gambling and gaming: casinos, betting platforms, lottery operators, speculative trading platforms structured as gambling

- Adult entertainment: any business involved in pornography, adult media, or related services

- Pork: pork production, processing, or distribution

- Interest-based financial services: conventional banks, insurance companies, and financial firms whose primary business is interest (riba)

Halal sectors, industries that are permissible:

- Precious metals: gold, silver, and other natural commodity production and trade

- Real estate: development, ownership, and rental of physical property

- Halal food production: manufacturing and distribution of food certified halal

- Healthcare: ethical medical services, pharmaceutical manufacturing

- Technology: software, communications, and technology services

- Logistics and infrastructure: transport, supply chain, and physical infrastructure

- Education: academic and professional education services

The 5% Revenue Rule Islamic scholars generally apply a 5% tolerance threshold: if a company derives less than 5% of revenue from haram activities, it may still qualify, provided the investor purifies this portion of their profit through charitable giving (zakat / sadaqah). However, this rule applies to diversified equity portfolios, not to direct investments. For direct investments, like gold-backed models, zero tolerance for haram activity is the standard.

6. The Complete Criterion Breakdown

The following table gives a comprehensive pass/fail breakdown for each criterion, with specific examples and the MAQ Investments position on each:

| Criterion | Investment PASSES if... | Investment FAILS if... | MAQ Investments Position |

|---|---|---|---|

| 1. No Riba (ربا): Zero fixed interest, anywhere | • Returns tied to business performance • Profit-sharing contract (Mudarabah) • No fixed coupon or interest rate | • Fixed interest rate, any amount • Guaranteed return regardless of performance • Conventional bonds or debentures | All investor returns come from physical gold operations and profit-sharing. No fixed interest. No riba, by design. |

| 2. Asset-Backed (أصول حقيقية): Real asset, real value | • Physical gold backing with allocation records • Direct real estate ownership • Verifiable commodity inventory | • Derivatives with no asset ownership • Leveraged products beyond actual assets • Purely paper-based financial instruments | 100% of investor capital is backed by physical gold. No leverage, no paper instruments. |

| 3. No Gharar (غرر): Full transparency, no hidden uncertainty | • Clear documentation of what capital buys • Honest disclosure of all risks • Transparent fee and profit-sharing structure | • Hidden fees or undisclosed deductions • Complex derivatives investor cannot understand • No Shariah board oversight or audit trail | Full transparency: asset disclosure, quarterly reports, Shariah board oversight, and clear profit-sharing agreements. |

| 4. Halal Sector (قطاعات حلال): No haram industries, zero tolerance | • Gold mining and logistics • Ethical commodity production • Halal food, healthcare, technology | • Alcohol, tobacco, or pork industry revenue • Gambling or adult entertainment • Conventional banks as primary investment | Operates exclusively in gold production, mining, and logistics. No haram sector exposure at any level. |

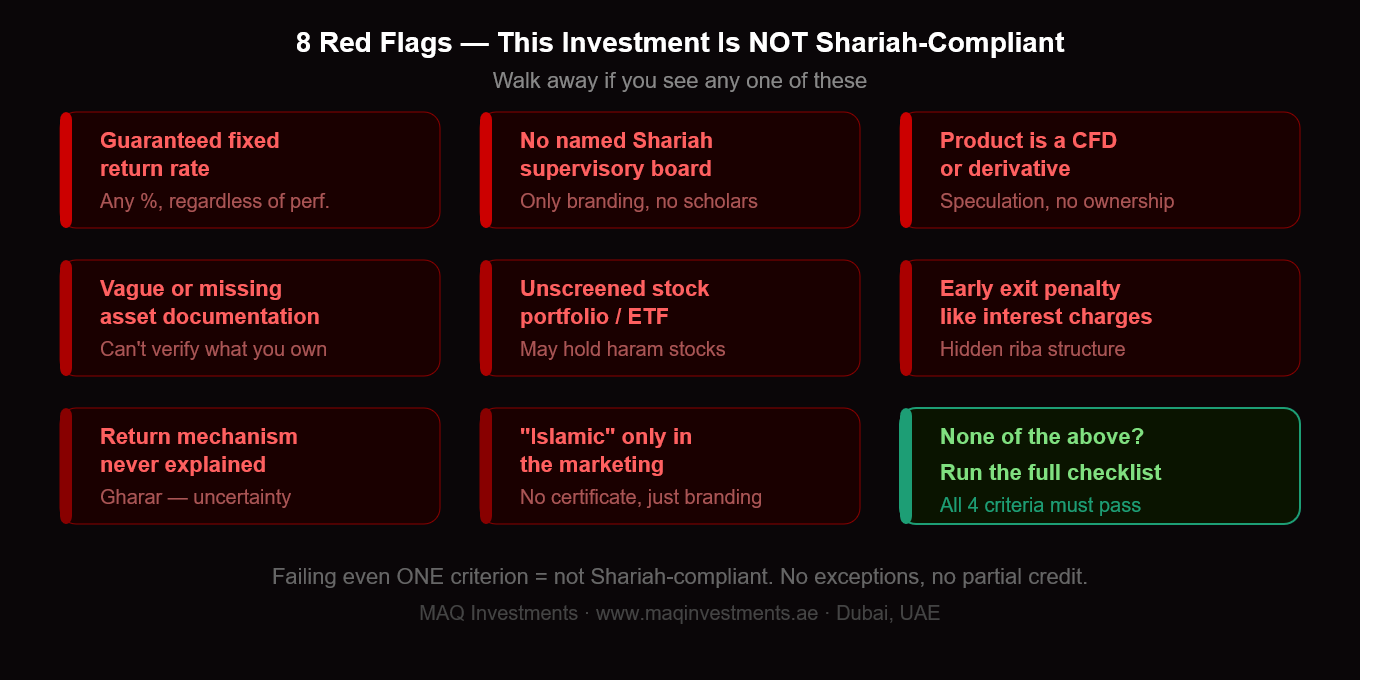

7. Red Flags: 8 Signs an Investment Is NOT Shariah-Compliant

Many investment products market themselves as Islamic or halal without meeting the full criteria. These are the warning signs to watch for:

| Red Flag | Why It Signals Non-Compliance |

|---|---|

| Guaranteed fixed return percentage | Any fixed return (e.g., 5%, 8%, 12%) regardless of business performance, is riba. Halal investments cannot guarantee a rate. |

| No mention of a Shariah board | Legitimate Shariah-compliant products are reviewed by qualified Islamic scholars. If no board is named, the claim is unverified. |

| The product is a derivative or CFD | Contracts for Difference (CFDs) and options involve speculation on price movements without asset ownership (gharar). |

| Vague or missing asset documentation | If you cannot verify exactly what physical asset your money is invested in, it fails the asset-backed criterion. |

| Investment in a generic stock portfolio | Generic equity funds often include alcohol, gambling, and banking stocks. Explicit halal screening is required. |

| Early withdrawal penalties resembling interest | If early exit costs are structured as percentage penalties on capital (like interest), this may constitute hidden riba. |

| No clear explanation of returns | If the documentation cannot explain the exact business activity generating your return, this is excessive uncertainty. |

| The 'Islamic' label is only in marketing | Some products label themselves Islamic to attract investors while the underlying structure remains interest-based. Ask for the certificate. |

8. How to Use This Checklist Before You Invest

When you are presented with any investment opportunity in the UAE, from a bank, a private firm, or an online platform, run through these five steps before committing capital:

Step 1: Ask for the Shariah Board Certificate A genuine Shariah-compliant investment will have documentation from a qualified Shariah supervisory board. Ask for the name of the board, the scholars who sit on it, and when the most recent compliance review was conducted. If no certificate exists, walk away.

Step 2: Identify the Return Mechanism Ask specifically: how is my return generated? Get a clear, plain-language answer. If the answer involves profit-sharing from a named business activity, good. If the answer is a fixed rate or involves guaranteed returns, it is riba.

Step 3: Verify the Asset Backing Ask: what physical asset is my capital secured by? Can I verify this asset exists and is allocated to my investment? Evasive answers indicate a problem.

Step 4: Screen the Business Sector Ask: what industry does this investment operate in? Request a breakdown of revenue sources if it is a diversified product.

Step 5: Read the Risk Disclosure A Shariah-compliant investment will honestly state the risk of loss. Genuine Islamic investments share risk; they do not eliminate it.

Before You Sign Anything, Ask These Four Questions:

- "Does this investment pay me fixed interest or profit-sharing?" (Must be profit-sharing)

- "What physical asset backs my capital, and where is the documentation?" (Must be specific)

- "Has this product been certified by a named Shariah supervisory board?" (Must be yes)

- "What industries does the underlying business operate in?" (Must be halal sectors only)

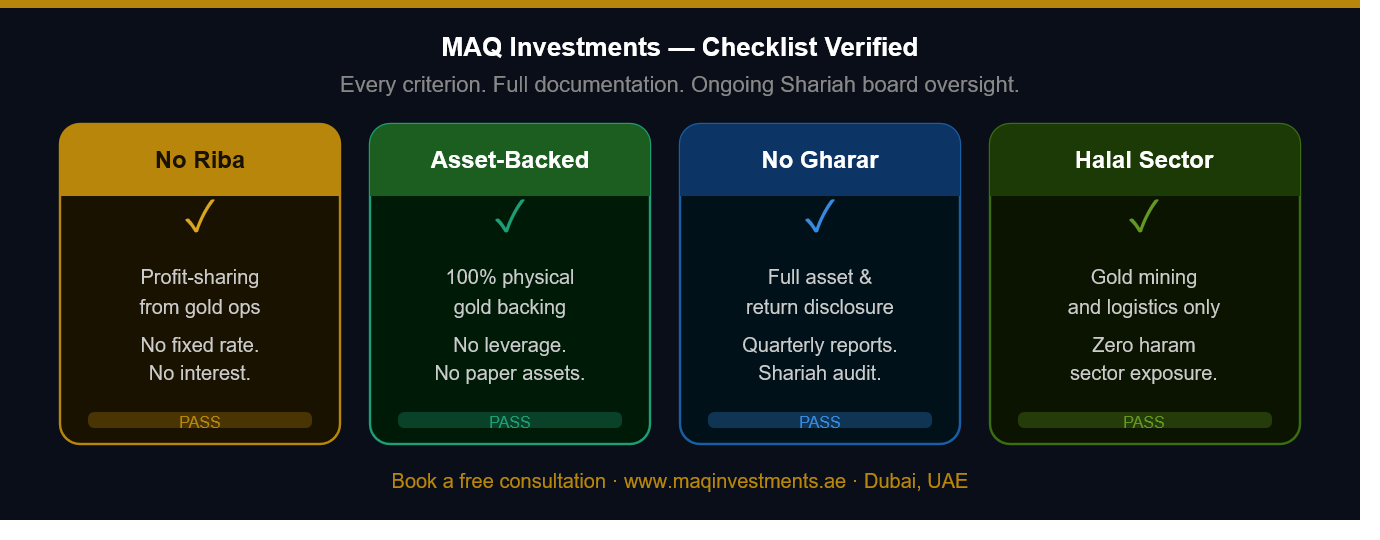

9. How MAQ Investments Passes Every Criterion

MAQ Investments was built from the ground up to satisfy every criterion on this checklist—not as an afterthought, but as the foundation of the business model.

| Criterion | MAQ Investments Position | Verification |

|---|---|---|

| No Riba | Returns are generated exclusively through profit-sharing from gold production operations. No fixed interest is paid or charged. | Ask for the profit-sharing agreement documentation at sign-up. |

| Asset-Backed | 100% of investor capital is secured by physical gold assets. The gold is real, allocated, and verifiable. | MAQ provides asset documentation upon investment. |

| No Gharar | Full transparency is non-negotiable. Investors receive clear documentation on what their capital buys, risks, and performance. | Quarterly reporting and Shariah board oversight from day one. |

| Halal Sector | Operates exclusively in gold mining, production, and logistics, sectors with full halal clearance. | Full business activity disclosure is available. |

Shariah Supervisory Board All investment plans and structures at MAQ Investments are reviewed and approved by qualified Islamic scholars with expertise in contemporary Islamic finance. Regular audits ensure ongoing compliance. Learn more about our Shariah compliance framework

10. Frequently Asked Questions (FAQ)

Q: What are the four criteria that make an investment Shariah-compliant? The four non-negotiable criteria are: (1) No riba: returns must come from profit-sharing; (2) Asset-backed: capital must be secured by a tangible physical asset; (3) No gharar: investment terms and risks must be fully transparent; (4) Halal sector: the underlying business must not operate in prohibited industries.

Q: What is riba in Islamic finance and how do I identify it? Riba is any guaranteed, fixed return on money disconnected from a real business outcome. If a return is a fixed percentage guaranteed regardless of whether the business makes a profit, it is riba. Legitimate returns are tied to actual business performance.

Q: What does 'asset-backed' mean in Shariah-compliant investment? It means your capital is secured by ownership of, or a genuine claim on, a tangible physical asset such as gold or real estate. Wealth must be grounded in real economic activity, not abstract paper instruments.

Q: What is gharar and why is it prohibited? Gharar means excessive uncertainty or ambiguity in a contract. It is prohibited because both parties must have full, clear knowledge of what is being exchanged. Hidden fees, overly complex structures, or pure speculation contain gharar.

Q: Is gold investment halal in Islam? Yes. Gold investment is halal when the gold is physically allocated, the transaction follows spot-price settlement rules, and it is free from speculative elements. Gold-backed investments like those by MAQ Investments are among the most naturally Shariah-compliant instruments available.

Q: Can non-Muslim investors use Shariah-compliant investments? Absolutely. Many non-Muslim investors choose Islamic finance products because of their built-in safeguards: mandatory asset backing, prohibition on excessive speculation, and full transparency.

11. How to Get Started with MAQ Investments

If you want to invest in a product that satisfies every criterion with full documentation and ongoing Shariah oversight, MAQ Investments is ready to welcome you.

- Step 1: Visit www.maqinvestments.ae to explore our gold-backed, Shariah-compliant investment structures.

- Step 2: Review our Shariah compliance documentation.

- Step 3: Schedule a free private consultation with our investment advisors.

- Step 4: Begin investing with complete asset documentation, transparent profit-sharing, and ongoing Shariah board oversight.

Invest the Right Way, Every Criterion. Every Time. Gold-backed · Shariah-compliant · Transparent · Quarterly returns · UAE-based Book a Free Consultation

Conclusion Shariah-compliant investment is a specific, well-defined standard, not a marketing phrase. An investment either satisfies all four criteria or it does not. The next time you are presented with an opportunity claiming to be halal, use this checklist. Ask the four questions. Request the documentation. If an investment cannot answer these with clear evidence, it has not earned the Shariah-compliant label.